Better practice reporting features

The key is to report clear and meaningful information in the performance reporting table. The following is a list of better practice reporting features:

- Template – Report in line with the Finance Secretary Direction, template and guidance

- Performance measures – Report each performance measure and/or each target in separate boxes or on separate rows so the reader is able to clearly identify the measure and associated target

- Key activities – refer to the key activities in the current (i.e. 2025–26) corporate plan by title. Use footnotes to explain any changes to the key activities which will be published in the next (i.e. 2026–27) corporate plan.

- Most entities report performance information for all the key activities that relate to each program. While some entities report performance measures by each key activity, this is optional and not a requirement.

- Expected performance results – Report the expected performance results for the current year (i.e. 2025–26) against the target (if any) and indicate whether the expected performance result is on track or not (if known)

- Footnotes – use footnotes to report changes, details and rationales

- Identifiers – Include any identifier (e.g. number) of the key activity, performance measure and/or target for a clear read between the PBS and current corporate plan.

Reporting one performance measure with one target

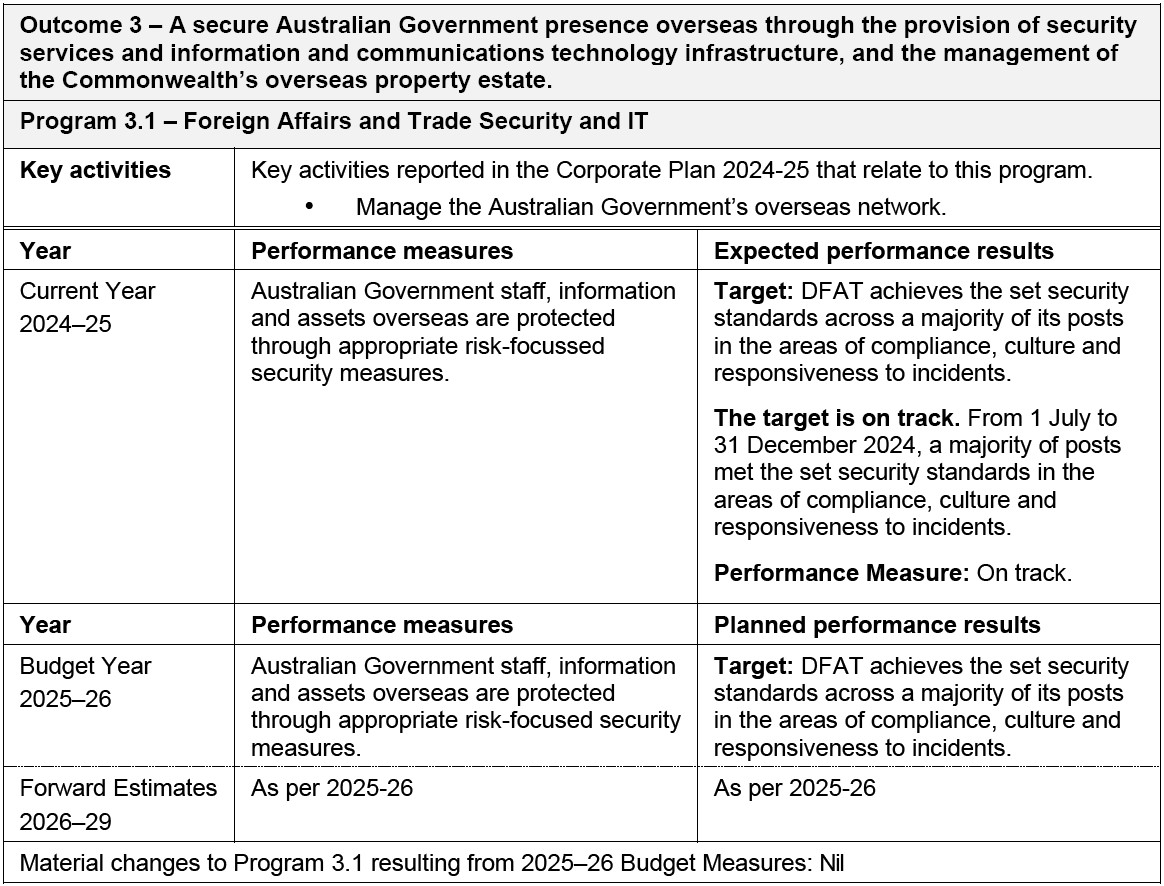

The Department of Foreign Affairs and Trade in the 2025–26 Foreign Affairs and Trade Portfolio Budget Statements (page 53) reported one performance measure under its Outcome 3, Program 3.1 and the relevant Key activity. In the example, the performance information:

- is reported in line with the template and guidance

- refers to the key activity from the current corporate plan, by title only

- is presented clearly in separate boxes, using bold text for the target, indicator and overall result

- the Expected performance results report the target, an indication that the target is on track to be met, the target result as at 31 December 2024, and an indicator that the performance measure is on track to be met

- the Planned performance results for the Budget year is reported correctly, outlining the measure and associated target for 2025–26

- the Planned performance results for the Forward estimates are reported ‘As per 2025–26’ to indicate the performance measure and associated target is the same (unchanged) from the Budget year

- clearly reports ‘Nil’ to indicate there have been no material changes to the program resulting from 2025–26 Budget Measures.

Reporting one performance measure with multiple targets

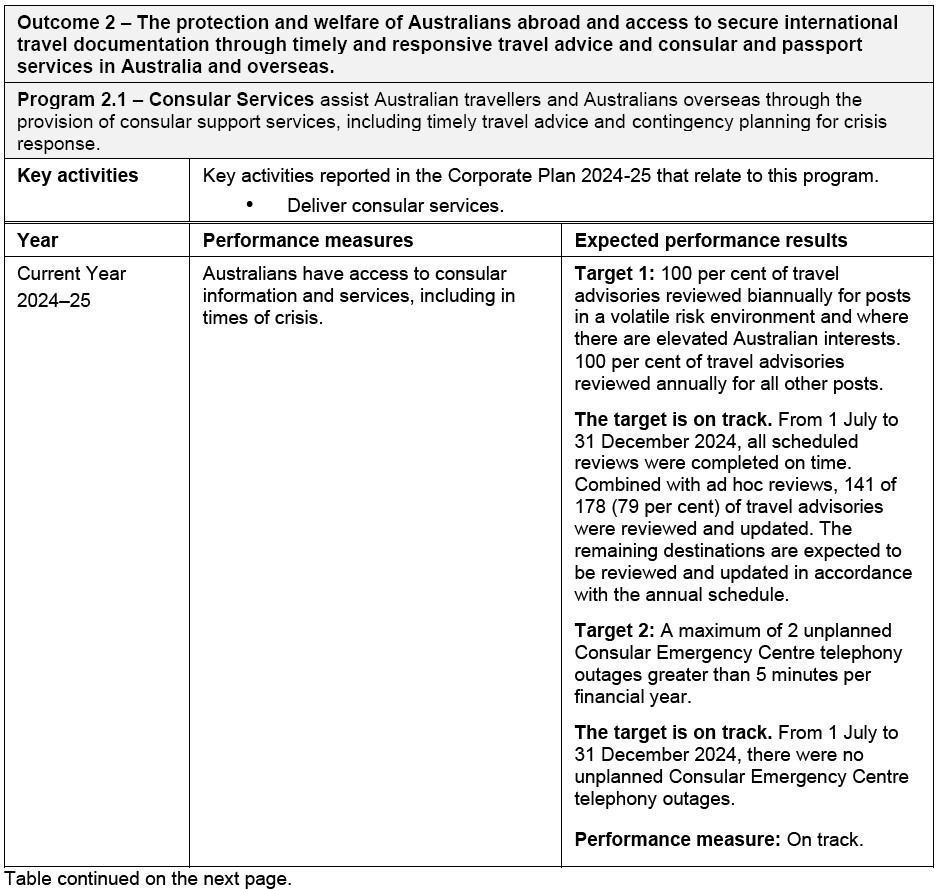

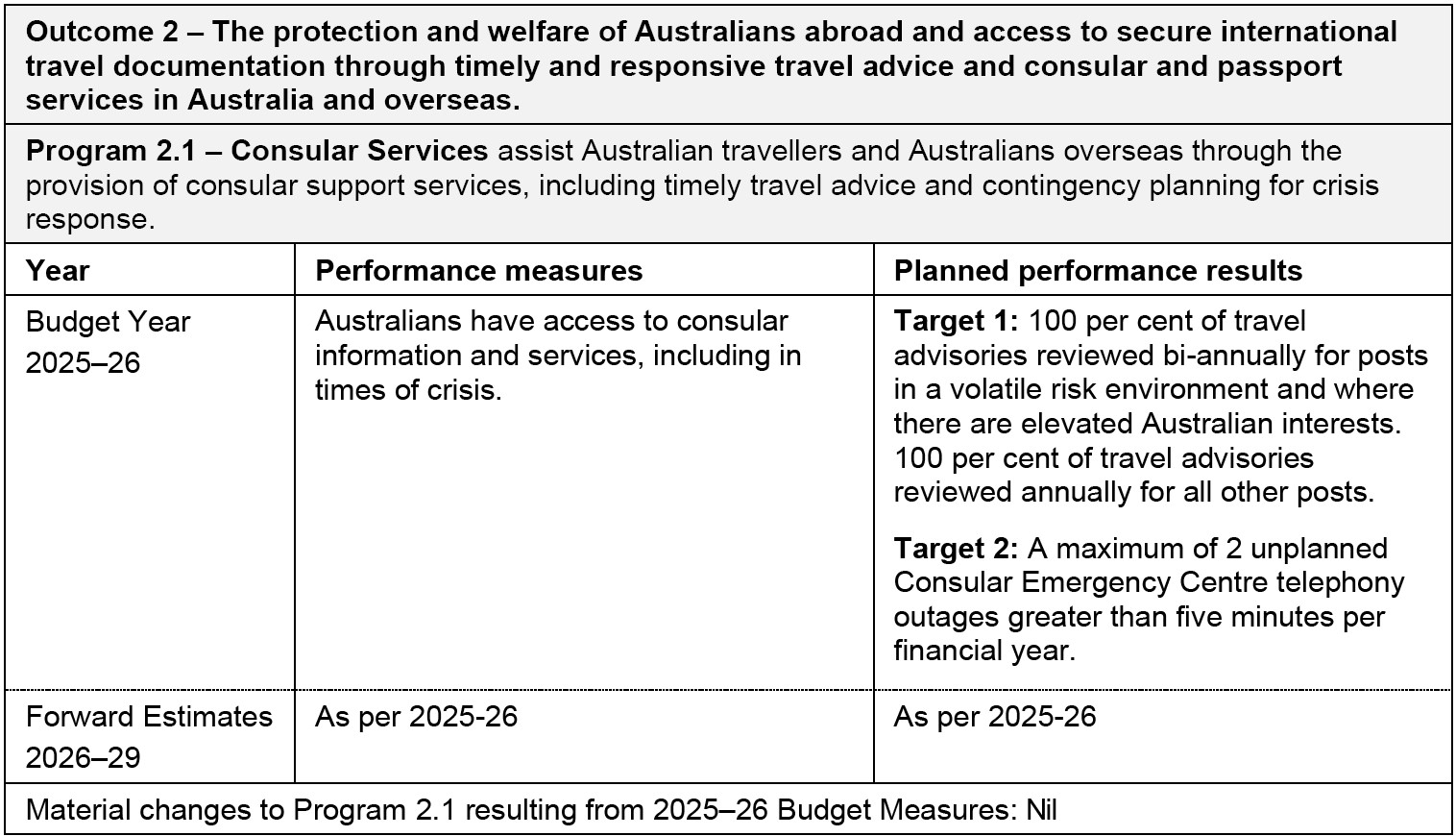

The Department of Foreign Affairs and Trade in the 2025–26 Foreign Affairs and Trade Portfolio Budget Statements (pages 48 and 49) reported one performance measure under its Outcome 2, Program 2.1 and the relevant Key activity. In the example, the performance information:

- is reported in line with the template and guidance

- refers to the key activity from the current corporate plan, by title only

- is presented clearly in separate boxes, using bold text for the numbered-targets, indicators and overall result

- the Expected performance results report the numbered-targets, an indication that the targets are on track to be met, the target results as at 31 December 2024, and an indicator that the performance measure is on track to be met

- the Planned performance results for the Budget year are reported correctly, outlining the performance measure and associated targets for 2025–26

- the Planned performance results for the Forward estimates are reported ‘As per 2025–26’ to indicate the performance measure and associated targets are the same (unchanged) from the Budget year

- clearly reports ‘Nil’ to indicate there have been no material changes to the program resulting from 2025–26 Budget Measures.

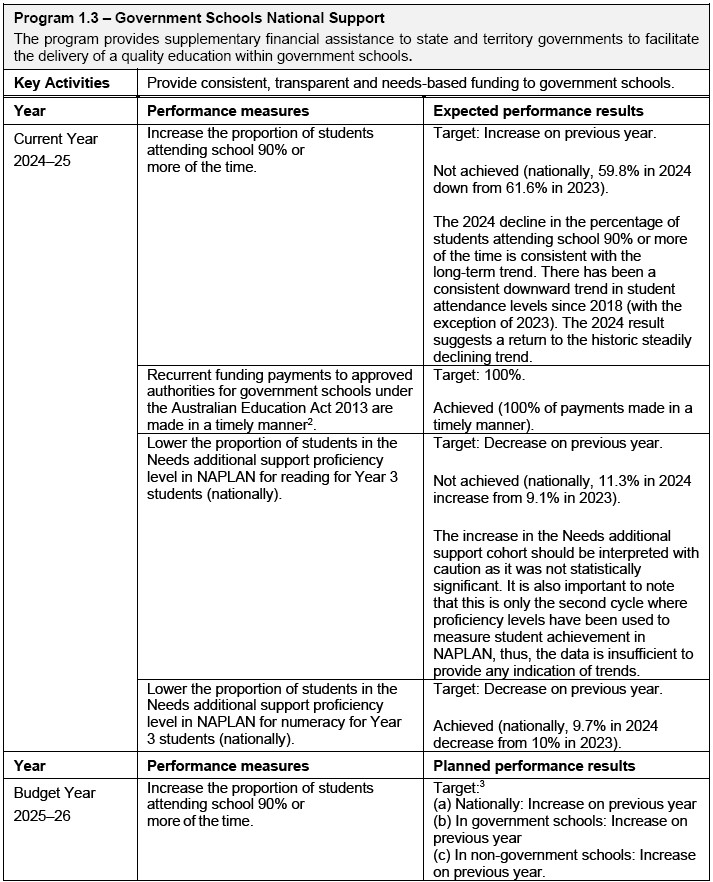

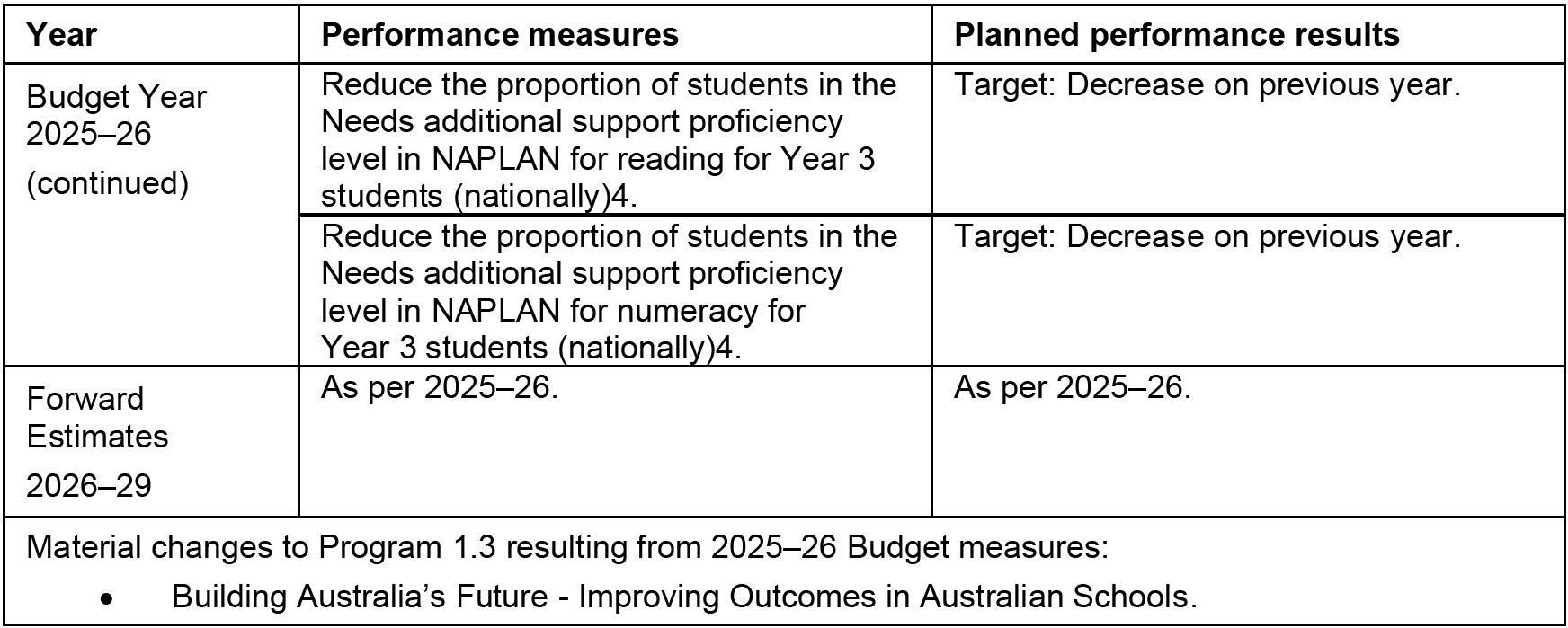

Reporting multiple performance measures

The Department of Education in the 2025–26 Education Portfolio Budget Statements (pages 31 and 32) reported its performance information under Outcome 1, Program 1.3 and the related key activity. In the example below, the performance information:

- is reported in line with the template and guidance

- refers to the key activity from the current corporate plan, by title only

- presents each performance measure and target in separate boxes, clearly reporting the targets, the actual results and data, and a short explanation as to why any measures are not expected to be achieved

- the Planned performance results for the Budget year are reported correctly, with the measure and revised target for 2026–27 and a footnote inserted which explain the reason for the change

- the Planned performance results for the Forward estimates are reported ‘As per 2025–26’ to indicate the performance measures and associated targets are the same (unchanged) from the Budget year

- reports the specific 2025–26 Budget measure which has resulted in a material change to the program

- includes appropriate footnotes to report changes, details and rationales which also provides a clear line of sight between the PBS and corporate plan.

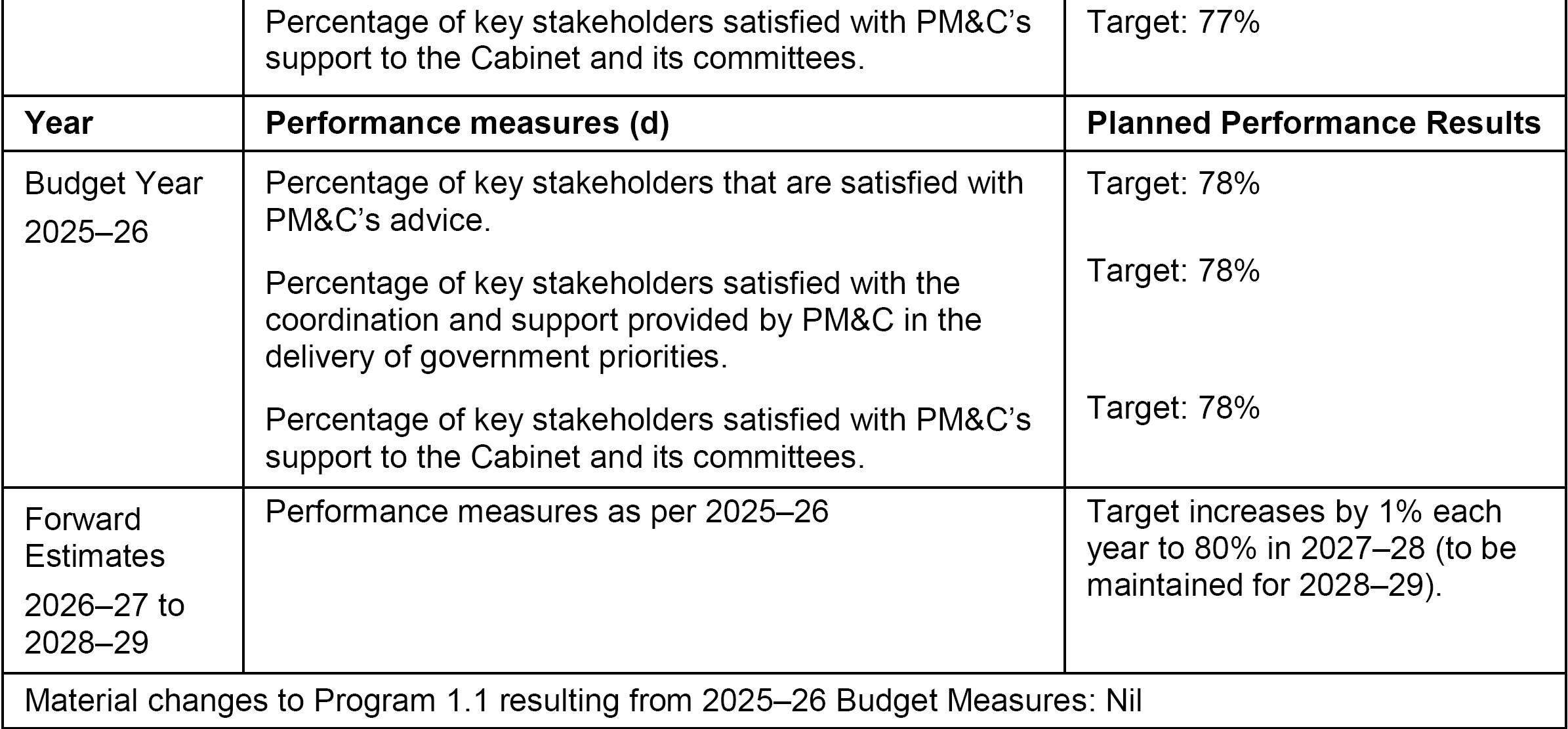

Reporting your entity is reviewing its performance measures

In the example below, the Department of the Prime Minister and Cabinet (PM&C) in the 2025–26 Prime Minister and Cabinet Portfolio Budget Statements (page 27) reported it was reviewing its performance measures for the Budget year under its Outcome 1, Program 1.1 and related key activity. It did so by inserting a footnote against the performance measures for the Budget Year and Forward Estimates. Footnote (d) clearly states: ‘The department is reviewing its performance measures for 2025–26. The department’s performance measures and targets will be published in the PM&C Corporate Plan 2025–26’.

Footnote (d) provides a clear signal that the performance information for the Budget Year and beyond is likely to change as a result of the review.

It is better practice to report the details and rationale of each change in the next corporate plan and corresponding annual performance statements.