Finance has developed a corporate plan template and a self-assessment tool. These are intended to support entities in meeting the minimum requirements of the PGPA framework, streamline corporate planning processes across Commonwealth entities and companies, and improve the consistency and quality of reporting.

The Commonwealth entity corporate plan template and the self-assessment tool are available under Tools and templates. The use of these is not mandatory, they are guides only.

For any questions or feedback on the templates and self-assessment tool, please contact PGPA@finance.gov.au.

RMGs are guidance documents. The purpose of an RMG is to support PGPA Act entities and companies in meeting the requirements of the PGPA framework. As guides, RMGs explain the legislation and policy requirements in plain English. RMGs support accountable authorities and officials to apply the intent of the framework. It is an official’s responsibility to ensure that Finance guidance is monitored regularly for updates, including changes in policy/requirements.

Audience

This guide is relevant to officials in Commonwealth entities (non-corporate and corporate Commonwealth entities) who assist the accountable authority to prepare their corporate plan.

Key points

This guide outlines:

- the content requirements for preparing a corporate plan

- the presentation and publication requirements

- how to vary a corporate plan

- better practice examples.

The accountable authority of a Commonwealth entity must prepare a corporate plan for the entity at least once each reporting period.

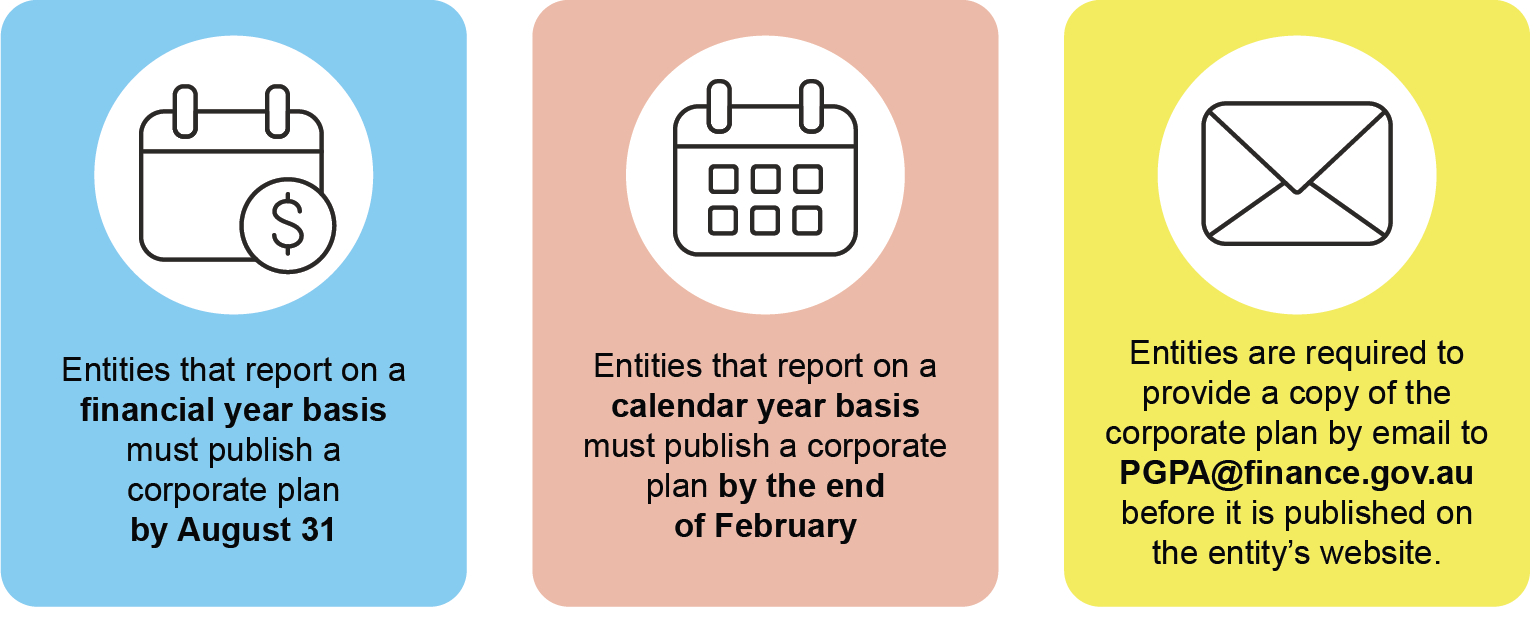

The corporate plan must be published on the entity’s website by the last day of the second month of the reporting period for which the plan is prepared, unless the entity's enabling legislation states a different period.

A copy of the entity's corporate plan must be given to the responsible Minister and the Finance Minister as soon as practicable after it is prepared and before it is published on the entity's website. To meet the requirement to give the corporate plan to the Finance Minister, a copy of the corporate plan should be sent to the Department of Finance at PGPA@finance.gov.au. Entities do not need to send a copy of the corporate plan to the Office of the Finance Minister directly.

Finance is responsible for publishing the entity’s corporate plan on the Transparency Portal after the plan has been sent to PGPA@finance.gov.au and the plan has been published on the entity’s website.

Resources

Related resources including links to related guidance, glossary terms, publications, PGPA Act and Rule, relevant legislation and a corporate plan template are located in the right-hand menu.

Corporate plan requirements for Commonwealth companies is covered by RMG-133 Corporate plan for Commonwealth companies.