Regulatory activities are generally those activities where the government is seeking to control or influence behaviour, manage risk and/or protect the community. They usually involve a compliance or enforcement and require legislation and Government approval. Other examples include registration, accreditation, monitoring and/or compliance. Regulatory activities set standards therefore are regarded as imposed (not optional) activities. Individuals or groups creating demand for the activity have no discretion of participating.

Charging for a regulatory activity requires a Government decision.

|

|

Fees | Levies | |

|---|---|---|---|

|

Nature of the activity |

Regulatory activities are generally those activities where the government is seeking to control or influence behaviour, manage risk and/or protect the community. The activities usually involve a compliance or enforcement (generally up to point of appeal) element and the individuals or organisations impacted have no discretion. |

||

|

Relationship between activity and the individual or group charged (reciprocity) |

Direct causal relationship between individual or organisation charged and activity delivered is required. |

Reasonable causal relationship between a group of individuals or organisations charged and activity delivered is required. |

|

|

Policy approval and policy authority to charge |

Government (Cabinet or the Prime Minister) |

||

|

Statutory basis to charge |

Legislation required |

Taxation Act required |

|

|

Charging model |

Cost model |

Minimum efficient costs (direct and indirect costs at activity output level) attributed to an individual or organisation |

Minimum efficient costs (direct and indirect costs at activity level) attributed through proxies to a group of individuals or organisations |

|

Pricing model |

Regulatory fees (full or partial cost recovery) |

Regulatory levies (full or partial cost recovery) |

|

|

Relationship between charges (expenses) and costs (revenues) |

Charges must reflect efficient unit cost of a specific good or service |

Charges must reflect efficient reasonable costs of the activity the individual causes. |

|

|

Publicly available documentation |

Regulatory charging activities must be documented in a CRIS prior to charging commencing. |

||

|

Public reporting under the PGPA Act |

Regulatory revenue and expenses must be reported in a regulatory charging summary note to the annual Financial Statements, the Digital Annual Reporting Tool and updated annually in the Cost Recovery Implementation Statement. |

||

|

Governance Finance Statistics (GFS) reporting classification |

Non-taxation revenue |

||

Characteristics and examples of regulatory activities

Charging for regulatory activities requires a discernible, aligned relationship between the costs and the amount charged to the recipient of the activity.

- The default charging position for regulatory activity, for both fees and levies, is that the price will recover the relevant costs of the regulatory effort required for the output to the individual or organisation. In some circumstances, the Government may agree to price a regulatory activity to recover less than the cost (that is, partial cost recovery).

There are 2 categories, the relationship between the costs and the amount charged (the price) to the recipient can fall into:

- Alignment between costs and amount charged to recipient (either the individual or the group). In these instances, the revenue (fee or levy) is classified as non-taxation revenue.

- Amount charged is not aligned and recipients (either the individual or the group) are charged more than the costs. In these instances, the revenue is classified as general taxation.

Principles for regulatory activities

The principles underpin decisions relating to the design, development, implementation and review of charging arrangements.

An entity must apply the principles across all stages, and must apply them consistent with Government priorities and policies, and with respect to entity's purposes and outcomes.

The 6 principles underpinning the Charging Framework apply to all activities. In addition to those, entities are expected to apply the additional 3 principles established specifically for the regulatory charging activities.

Transparency refers to openness and a willingness to make information available about the activity of charging. Transparency allows appropriate scrutiny of government charging decisions and processes by providing access to information.

Transparency involves reporting on performance for the charge and the activity of charging, on an ongoing basis.

When charging for regulatory activity, transparency means documenting key information about the activity of charging and the charges in a way that is accessible for those who pay charges and for other stakeholders. Key information includes policy approval, legal basis for the activity of charging and the charging model. This allows consideration of whether the activity of charging and the charges are being implemented efficiently and effectively, and demonstrates that charging itself is consistent with the policy decision/s.

Accountability refers to clear roles and responsibilities for key stakeholders throughout all stages of the charging process and having in place appropriate governance structures. Accountability involves ensuring that entities, their staff and the responsible Ministers are answerable for their actions and decisions in relation to charging.

The documentation for a specific charging activity should provide sufficient detail to allow the Parliament, those who pay the charges, and other stakeholders to analyse the activity. This includes clearly stating when, by whom, and at what level the charge is set. Entities have some discretion over the level of detail in documentation that is publicly available.

Documenting the policy decision/s and the model for calculating the charge are fundamental to accountability.

Efficiency and effectiveness in government involve making the proper use of available resources (people, money and other supplies) to achieve government policy outcomes. Government activities should meet quantity, quality and other targets, be undertaken at minimum efficient cost, and while achieving the policy objectives and complying with applicable legislative requirements.

For a regulatory activity, efficiency also relates to whether it is efficient to provide the activity on a charging basis (that is, the costs of administering charging should be proportional to the charges for and potential revenue from the activity). This requires a balance between developing a more precise, but more complex and hence more expensive costing model, and developing a simpler and less expensive, but less precise, costing model.

The effectiveness of charging relates to whether the level of the charge (the price) supports the Government’s policy objectives for both the activity and the charging. Effective charging means the appropriate price to enable the desired charging policy outcomes, while also being conscious of the other policy objectives. The effectiveness of cost recovery involves the reliability and accuracy of the cost recovery model and related processes in measuring costs and reflecting those costs in the related charges. Effective cost recovery includes appropriate revenue management.

Stakeholder engagement is particularly important for regulatory activities that are charged for, as the price of the charges have a direct impact on those who pay them.

Stakeholder involvement generally results in better design, planning and implementation of government activities. Successful stakeholder engagement involves well planned and meaningful consultation. Commonwealth entities should have open dialogue with stakeholders, consider their views and, where appropriate, take action.

Entities should engage actively with stakeholders throughout all stages of the charging process, from policy development through to implementation and review. They should develop and implement an ongoing engagement strategy for consultation with stakeholders. Finally, they should consider performance indicators when measuring the effectiveness of stakeholder engagement and revise processes to continuously improve and build trust.

Requirements for regulatory activities

Key requirements must be applied throughout the stages of design, implementation and review of the charging arrangement

Government approval to enable charging for a regulatory activity requires separate decision points. The decisions may be sought separately or concurrently with the policy approval, depending on the circumstance and the nature of the regulatory activity. Decisions are needed to provide:

- approval for the activity to be delivered to the non-government sector to achieve the policy objective

- approval to charge the non-government sector for the activity and at what level (i.e. below full cost - partial recovery, or at full cost recovery)

- approval to develop or change legislation when required.

Entities must contact the Office of Impact Analysis prior to seeking policy approval to check whether a Policy Impact Assessment (PIA) will be required. If a PIA is required, it must accompany the policy proposal.

When assessing the potential to charge, for new or existing government activities or when making changes to the level of a charge, entity staff should conduct appropriate research and analysis, including stakeholders’ consultations. This analysis will inform the Charging Risk Assessment and help determine whether there is a policy rationale to charge or not and what the outcome of charging is likely to be.

Approval of the policy

Policy approval for an activity (for example, provision of goods, services or regulation) is sought by preparing a policy proposal and recommendations for Government consideration in accordance with the Budget Process Operational Rules.

If policy approval is sought from Cabinet, authority to bring the proposal forward for consideration is required, refer to the Budget Process Operational Rules and the Cabinet Handbook.

Records of policy decision

Entities are expected to maintain records of the policy approval to undertake and charge for the activity, including authority for relevant legislation. This assists entities in reporting in their Portfolio Charges Review.

Approval to charge

A policy proposal that involves charging must seek explicit policy approval from the Government to allow charging for the activity. The proposal may relate to introducing charging for new or existing government activities or may involve changing the existing charges for activities.

The policy proposal to charge should contain information on the costs and revenues, likely outcomes from the price level for the public and industries and the risks of each option approach to charging. This allows decision-makers to consider the merits of charging, level of charging (full or partial cost recovery) or changes to charges.

Changes within the policy decision

From time to time, entities may need to make changes to their cost recovered activities as a result of stakeholder feedback, changes in policy or internal monitoring and evaluation. The nature of the changes will determine how they should be approved and implemented. Staff may need to seek advice on the potential policy or legal implications of expected or potential changes to the cost recovered activity.

There are 2 broad types of changes:

- operational changes - relate to the day-to-day management of the activity within the boundaries of the existing policy approval from the Government.

- policy changes - involve variations that are beyond the policy approval for the activity.

Operational changes can be approved by the Relevant minister or Accountable Authority when:

- Relates to day-to-day management within existing policy approval (for example, increase or decrease in charges due to business processes)

- Changes to an existing charging model (for example, due to changes in costs)

- Some material, sensitive or complex operational amendments within existing policy (for example, changes to legislation required to reflect the changed charges structure)

If policy approval needs to be sought from Cabinet, authority to bring the proposal forward for consideration is required, refer to the Budget Process Operational Rules and Cabinet Handbook.

Entities must have a legal basis to charge for a regulatory activity via relevant legislation.

- All charges must have a legal basis through specific legislation (an Act, regulation or legislative instruments).

There must be a legal basis to charge before charging can commence.

Relevant legislation may include the enabling legislation of a Commonwealth entity, legislation for the activity and/or taxation legislation. If charging is being considered, it should be provided for in the enabling legislation for the activity.

- If charging is not supported by existing legislation, new activities that involve charging may require new or amended legislation to give a legal basis to charge.

The detail in the policy approved by Government will inform the relevant legislation, and may include:

- the ability to charge for an activity

- any measures that may need to be included in the legislation

- if known, any criteria or limits to what may be charged for or the level of the charge

- any subsequent decision to charge and the level of the charge (price level).

Where there are changes to the activities covered by legislation, or there are changes to policy objectives of Government, entities should review the activities and legislation to determine whether refreshed policy approval may be required.

The type of legislation required depends on the activity, the costs involved, and whether costs can be attributed to an individual or group.

Entities should consult with the Department of Foreign Affairs and Trade if there is a possibility that international law or other obligations (for example, treaties that govern international trade) could constrain the application of charges.

Entity should consult with the Treasury early in the policy development process when charges may fall into taxation matters.

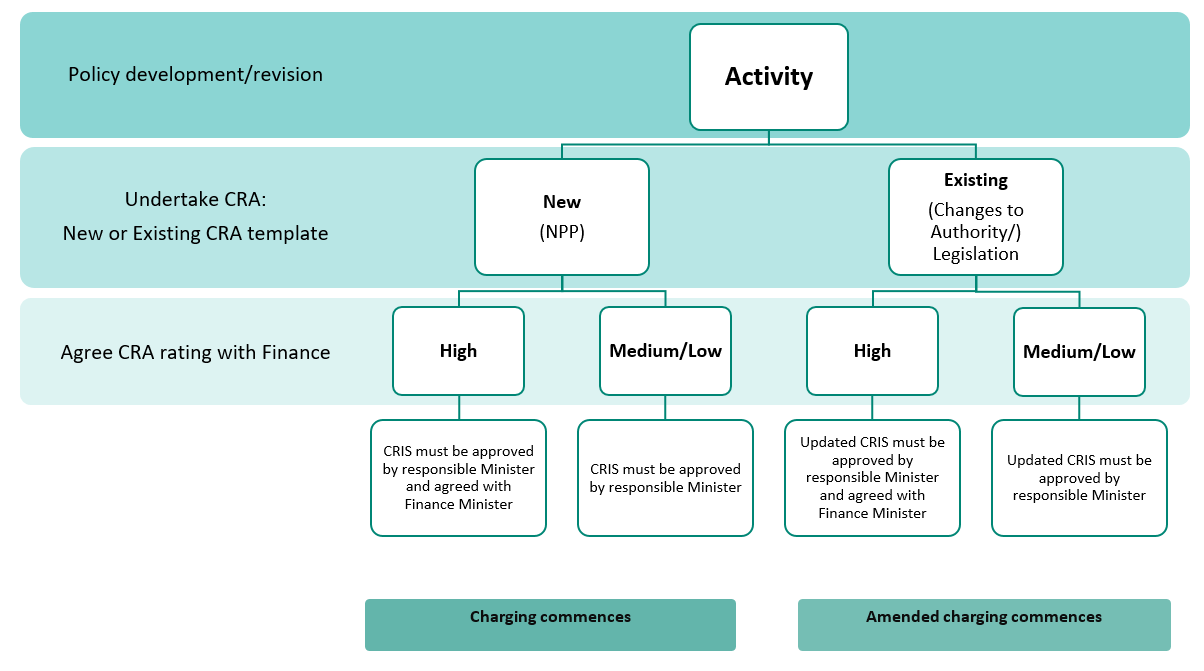

Entities must complete a Charging Risk Assessment for all New Policy Proposals which involve charging for a regulatory activity.

The CRA provides a tool for ongoing review of charging activities' risk and is used as a part of the annual review process when updating the Cost Recovery Implementation Statement.

Risk engagement involves ongoing assessment and management of risk that may adversely impact the policy intend for the charging activity. A key element of planning, designing and managing charging activities is to identify and engage with risk at each stage of the charging process.

During the development of policy, implementation and review of charging arrangements, entities should assess the risks associated with the charging arrangements. This will have an impact on who makes the decision to charge, the risk management strategy to ensure charging achieves its stated intentions, the scale and detail of the charges and the stakeholder engagement strategy.

When analysing risk, entities should consider the entity’s operating environment and factors that influence charging across 3 areas: complexity, materiality and sensitivity.

This analysis could include the following:

| Complexity relates to the structures, processes and implementation of the specific activity. Complexity may be influenced by: |

|

| Materiality relates to the financial value of the activity and may be influenced by: |

|

| Sensitivity relates to the level of interest in the activity or the charge for the activity from government stakeholders, non-government stakeholders, the media and the Parliament. These considerations include: |

|

Charging Risk Assessment

Entities must self-assess the risks associated with materiality, complexity and sensitivity for any new or amended charging activity as part of the policy proposal process and for subsequent changes to charging arrangements. This process is called the Charging Risk Assessment (CRA) and its rating determines the processes required for release of the Cost Recovery Implementation Statement (CRIS).

The risk rating does not determine whether regulatory charging is appropriate, or whether some activities are more suitable for charging than others.

The purpose of the CRA is for responsible entities and Ministers to determine how to engage with the identified risks and to inform the risk engagement strategy adopted by the entity.

- For new regulatory charging, a risk assessment must be undertaken and incorporated in the new policy proposal (NPP). Finance agrees the risk rating for regulatory charging as part of the policy proposal process.

- For existing regulatory charging, a risk assessment informs the approval process for any proposed changes to the policy authority and/or legislation.

Finance has developed a CRA template along with CRA Information Sheet to assist with assessment of the charging risk. These resources are available under Tools and templates in the right hand menu.

- New charging for regulatory activities - CRA New Charging Activity

- Changes to existing charging for regulatory activities - CRA Existing Charting Activity.

If an entity chooses not to use the template, they must assess the risk of the activity using factors similar to those listed in the template.

The entity’s self-assessment rating of risks associated with materiality, complexity and sensitivity for any new or amended charging activity needs to be agreed with Finance.

Based on the responses to the questions contained in CRA template, a risk rating can be:

The agreed CRA rating determines the processes required for release of the CRIS.

A CRA rating of leads to one of two outcomes:

- high means that the responsible Minister needs to seek the Finance Minister’s agreement to the release of the CRIS before charging begins

- low or medium means that the CRIS can be approved by the responsible Minister and does not require the Finance Minister’s agreement for release of the CRIS before charging begins.

Frequency of CRA reviews

Entities must undertake the CRA at the policy approval stage prior to introducing any new charging activities. It is worth noting that CRA rating may change over the policy developing period, for example, at the start there may not have been stakeholder consultation feedback available, but once this feedback is obtained the information is available that potentially can changing the CRA rating.

Once regulatory charging is implemented, entities may need to amend the charging activities along with its risks. Risk assessment is expected to be undertaken as often as required by the activities and/or operating environment changes, and at least annually as part of the annual CRIS review process.

Charging Risk Assessment (CRA) rating for new or existing regulatory charging activities

Entities must align expenses and revenue for the delivery of the activity. This should be done on a yearly basis, or when justified can be aligned over a longer period (for example, the business cycle of the activity).

A charging model is used to support alignment of expenses and revenues. It is made up of 2 separate components, the determination of expected costs (through a cost model) and the determination of pricing for the output to the user and Government (through a price model).

A charging model enables entities for an ongoing management and comparison of actual costs and revenues and expected efficient costs and revenues to:

- ensure prices remain aligned with the policy approval for the level of the price and the requirements of the Charging Framework

- manage any potential over and under-recovery of costs of the activity in line with the Government determined policy authority to charge: at full cost recovery or below costs

- measure and improve efficiency and performance, including by tracking the degree of alignment between expenses and revenue

- demonstrate how prices relate to the costs of the activity:

- this is through appropriate attribution of outputs and subsequent business processes to charges

- should the legal basis or constitutional validity for the charges be challenged.

Regulatory charges should be:

- clear and easy to understand

- closely linked to the specific activity

- set to recover the full efficient costs of the specific activity

- efficient to determine, collect and enforce

- set to avoid volatility, while still being flexible enough to allow for changes based on fluctuations in demand or costs.

There must be alignment between the cost (expenses) of an activity and the price (revenue generated through charges). For activities that are partially cost recovered, the degree of alignment for expenses and revenue is agreed by Government.

Ideally, the expenses and revenue should be aligned on a yearly basis. However, where justified, they can be aligned over a longer period (for example, the business cycle could be longer to reflect peaks and troughs of the activity, or length of accreditation period).

The degree of alignment between expenses and revenue may vary for different activities, as the business cycles and cost drivers for those activities differ. Entities should develop systems to manage any under or over-recovery. These systems and processes need to prevent systemic misalignment of expenses and revenue to ensure the Government decision for full cost recovery or set part recovery is being delivered.

For a regulatory activity the level of charge (price) must not exceed the minimum efficient cost of the entity’s delivery of that particular output. As such, entity staff should consider how to develop an understanding of the costs of an output of ‘activity’.

This means that:

- regulatory (cost recovery) fee, the entity must know and be able to evidence what the cost per good, service or regulation is and how the charge to the individual or organisation for delivering that output have been determined.

- regulatory (cost recovery) levy, the entity must know how much it costs to deliver specific output to group of individuals or organisations within a sector. When designing a levy, staff should select a relevant cost driver as the basis for the distribution of levy payments among individual levy payers. The cost driver should approximate the level of resources used to provide the activity to levy payers. Depending on the activity, this may be done by distributing the levy payments on an equal basis (a flat levy rate). Alternatively, differentiated levy rates could be used to more closely reflect resources used by different groups of levy payers based on their risk, size or other criteria. Complex activities may justify the use of more than one cost driver to determine levy rates. The potential for cross-subsidisation among levy payers may increase if a levy rate does not bear a reasonable relationship to the cost driver of the activity.

Resetting costs and indexation

As a default, regulatory costs are to be reviewed on an annual basis. Costs must be set to confirm the current minimum efficient costs as evidenced by a process assessment and actual costs from the previous year before an updated indexation rate is applied to appropriate cost elements. This process ensures charges reflect the ongoing efficient costs of delivering the activity and the Government decision for full/partial cost recovery.

Activities are only exempted from indexation if policy outcomes are significantly adversely impacted and this determination may require the Government decision.

Entities should be able to explain any variance between actual expenses and revenue in any one year in their CRIS.

Entities must

- publish the Cost Recovery Implementation Statement (CRIS), on their website before charging commences

- ensure the information in the CRIS remains up to date at least annually.

In addition:

- report actual expenses and revenue at an aggregated level in annual financial statements

- where appropriate, outline its non-financial charging performance measures in its Corporate Plan and report on these measures in its Annual Performance Statement.

The entity’s charging documentation should summarise the purpose for charging for an activity and details of the authority to charge (for example, link to legislation or Budget papers). The documentation, irrespective of the type of charge, should also provide information on how charging is implemented, managed and monitored. It should also collect information on how the activity is performing on an ongoing basis, including how the entity has addressed the charging principles and requirements.

This documentation is used in Portfolio Charging Reviews and supports the Accountable Authority in meeting their duties under the Public Governance, Performance and Accountability Act 2013.

Cost Recovery Implementation Statement

Each regulatory activity that is charged for, regardless of financial value, must be documented in a Cost Recovery Implementation Statement (CRIS). The level of information in the CRIS should be proportional to the complexity, materiality and sensitivity of the activity.

The CRIS is an explanatory document that provides key information on the entity’s charging arrangements, it should be finalised, approved and published on the entity’s website before charges commence.

After charging commences, the CRIS also becomes a continuous disclosure tool being updated at least annually. It reports how the activity is performing and provides the basis for ongoing engagement with stakeholders on various aspects of the regulatory activity.

A CRIS can document more than one activity (for example, where the activities are related or have common stakeholders). Where more than one Commonwealth entity is involved in providing a cost recovered activity, the entity that has the overall operational responsibility for the activity should prepare the CRIS with input from other relevant entities. Where cost recovery charges for an activity are collected by one entity, but the activity is provided by one or more other entities, the responsible entities may choose to prepare a combined CRIS.

Entities are encouraged to use the CRIS template developed by Finance. If the entity chooses not to use the template, the entity must still meet the CRIS content requirements listed below.

The CRIS is prepared after the Government makes a decision to charge for the specific regulatory activity. A draft CRIS may support legislative drafting, determination of pricing, and engagement with stakeholders.

CRIS Requirements

- background information on the activity, including its purpose and intended policy outcomes and outputs

- description of the activity and of the stakeholders who pay charges, or may be affected by the charges, for the activity

- details of the Government policy approval to charge for the activity - this may include the date and details of any relevant public announcement

- details of the legislation authorising the charges - including links to primary and subordinate legislation

- an explanation of how the activity is costed - a description of how the activity has been broken down into outputs and processes, and how those have been costed, including cost drivers and assumptions

- an explanation of the design of the charges - which types of charges have been used and why, including their link to the outputs and processes of the activity

- an assessment of risk, including the factors contributing to the risk rating

- the stakeholder engagement strategy, including a summary of the most recent consultation round - was consulted and when, what their views were, and how those views have been considered

- financial estimates for the activity (expenses and revenue) for the current financial year and 3 forward years

- reporting on the financial and non-financial performance of the activity

- key forward dates and events, including the date of the next portfolio charging review.

- certified by the Accountable Authority of the Commonwealth entity

- approved by the responsible Minister

- agreed for release by the Minister for Finance (only if the CRA rating for the activity is ‘high’)

- published on the responsible entity’s website before charging commences for the activity.

Where the Finance Minister’s agreement for release is required, entity staff should factor in enough time to allow for that involvement. Approval of the CRIS should be obtained before amending legislation or legislative instruments.

Entities should also note that the Government or the Minister for Finance may also request that any CRIS be brought forward for agreement as part of other processes.

Regulatory charges financial performance

Annual Reports and Annual Financial Statements

A Commonwealth entity must report on an aggregate level the financial information of cost recovery in the entity’s annual financial statements, in accordance with the Public Governance, Performance and Accountability (Financial Reporting) Rule 2015 (FRR).

Non-financial performance

The accountable authority of a Commonwealth entity must measure and assess the performance of the entity in achieving its purposes. Delivery of the regulatory activities would contribute to achieving these purposes.

Performance measures and other information are key inputs used by government entities in evaluating whether outputs have been produced and outcomes have been achieved. The primary planning document outlining entities non-financial performance is the corporate plan. It provides Parliament, the public and stakeholders with an understanding of the purpose of an entity, its functions, objectives and role.

When it is appropriate to develop measures for charging activities performance, measures can be based on relevant information from a range of sources, such as:

- outcome measures that assess the extent to which the charging activity is contributing to meeting government policy outcomes. They relate to changes effected in the community and may include such things as minimised risks of exotic pests and diseases harming the Australian natural environment, food security and economy, or more timely access to safe and effective therapeutic goods for the Australian community.

- output measures that show the extent to which the charging activity’s operational targets or milestones have been achieved. They may include such things as the numbers of permit applications processed, the numbers of permit applications processed within statutory timeframes, or the numbers of compliance audits that were required over the reporting period.

Benchmarking is one method that may support entities to measure performance of a charging activity. Benchmarking can be against either the whole activity or, where there is no directly comparable activity, against the business processes within the activity.

When evaluating performance, Commonwealth entities should consider common traps, which include:

- assuming that the production of outputs secures the desired outcomes

- assuming that the consumption of inputs results in the desired outputs and outcomes

- framing performance measures that rely on data that cannot be validated.

Over time, a charging activity may no longer be consistent with government policy priorities or may become inefficient. In such circumstances, entity staff should consider whether the activity of charging or the charge should be reviewed.

When reviewing existing charging, entities should consider whether the policy intent of the activity is being appropriately supported by the price level of the charge.

Entities may need to make changes to their charging as a result of changes in cost inputs (increasing or decreasing), stakeholder feedback/changed in operating environment, policy changes or internal monitoring and evaluation. The nature of the changes will determine how they should be approved and implemented. Entities may need to seek advice on the potential policy or legal implications of expected or potential changes to the charging activity.

The treatment of changes to regulatory charges depends on the charging risk assessment (which includes complexity, materiality and sensitivity) of the charge to the user and the total costs and revenues to the government.

Regular review, at least yearly, of the Cost Recovery Implementation Statement (CRIS) provides the information needed to start any change process. This approach provides the assurance on how the level of the actual charge aligns to the Government decision, relevant legislation and the minimum efficient cost of the effort of the Commonwealth entity.