Commonwealth Climate Disclosure requirements depend on the Tranche your entity is in. Each Tranche has reporting obligations that gradually increase each year until all requirements are fully phased in. If you're unsure which Tranche applies refer to When Do I Start Disclosing.

Climate Disclosure Requirements for Tranche 1 and 2

Year 1 CCD Requirements are to be applied by:

- Tranche 1: FY2024–2025 climate disclosures

- Tranche 2: FY2025–2026 climate disclosures

Year 2 Requirements are to be applied by:

- Tranche 1: FY2025–2026 climate disclosures

- Tranche 2: FY2026–2027 climate disclosures

Year 3 Requirements are to be applied by:

- Tranche 1: FY2026–2027 climate disclosures, and onwards

- Tranche 2: FY2027–2028 climate disclosures, and onwards

Tranche 1 and 2 entities follow a phased approach over 3 years for the CCD Requirements, which includes:

- Year 1 introduces fundamentals across the 4 pillars

- Year 2 builds on requirements and introduces more detailed criteria, including public policy effects and climate-related scenario analysis

- Year 3 and onwards introduces more complex criteria to reach the full set of Requirements.

Climate Disclosure Requirements for Tranche 3

Year 1 Simplified Requirements are to be applied by:

- Tranche 3: FY2026-2027 climate disclosures

Year 2 Simplified Requirements are to be applied by:

- Tranche 3: FY2027-2028 and onwards

Tranche 3 entities follow a phased approach over 2 years for the CCD Simplified Requirements:

- Year 1 introduces a limited set of criteria across the 4 pillars

- Year 2 builds on requirements and introduces more complex criteria, including public policy effects to reach the full set of simplified requirements.

For full requirements and reporting information on all tranches, see Commonwealth Climate Disclosure Requirements.

Disclosures are structured across 4 main areas

Detailed CCD requirements for each Tranche and reporting year are available on the CCD Requirements page. For further help also see the CCD e-learning module.

Entities must disclose information to address the 4 pillars:

- Governance

- Strategy

- Risk management

- Metrics and targets

The Commonwealth Climate Disclosure Requirements

An entity begins with Year 1 disclosure requirements with additional requirements added in Year 2 and Year 3. By Year 3 for the full Requirements and Year 2 for the Simplified Requirements, the Requirements include:

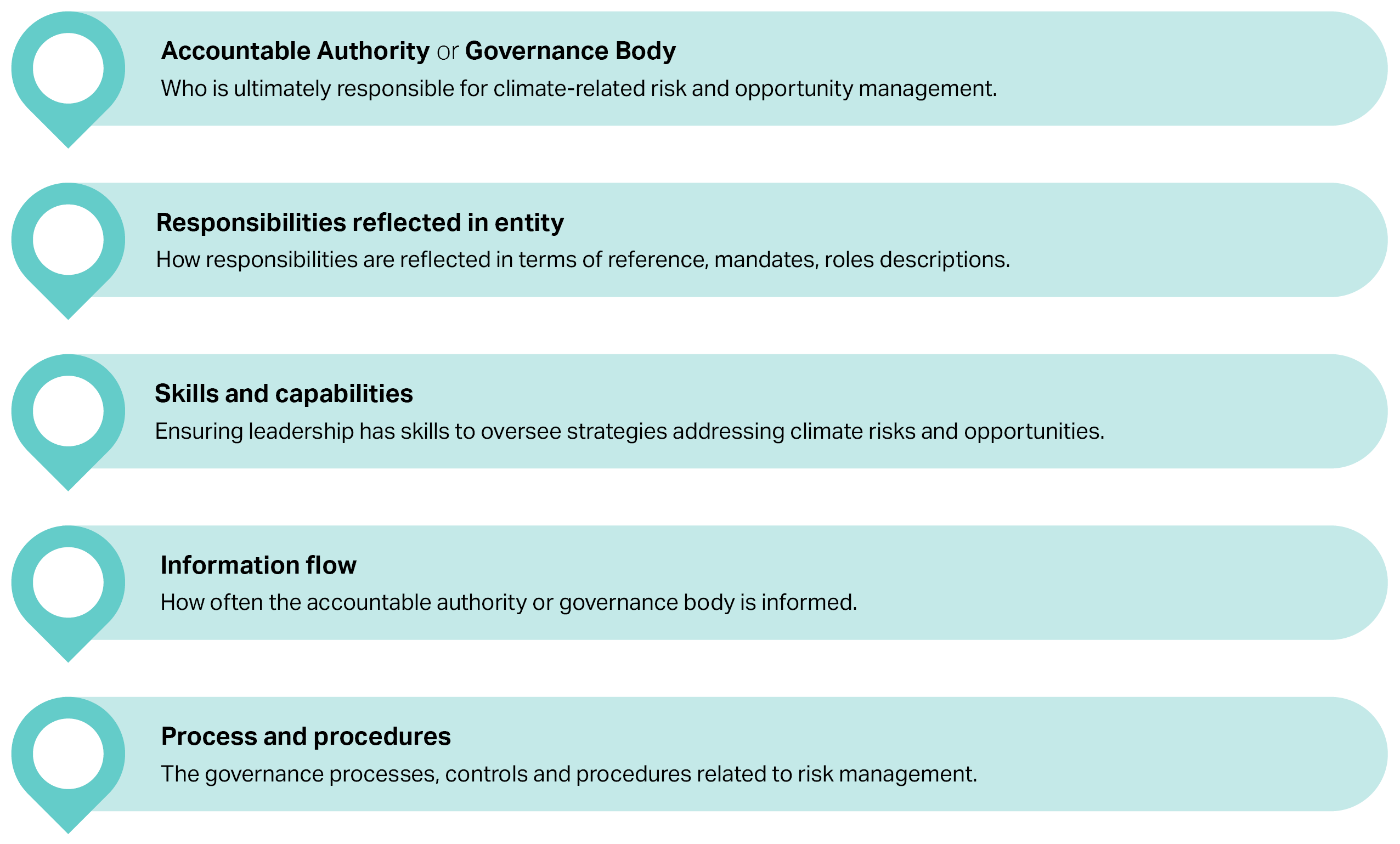

Governance identifies the accountable authority, oversight mechanisms, skills, information flow and target-setting responsibilities. Governance criteria include the following key areas: accountable authority or governance body, responsibilities reflected in entity, skills and capabilities, information flow, and process and procedures.

Strategy explains material risks and opportunities, operational model effects and in later years, public policy effects, financial effects and outlines scenario analysis. Strategy criteria include the following key areas. Strategy criteria include the following key areas: climate-related risks and opportunities, operational model effects, public policy effects, strategy and decision-making effects, financial position and performance and cashflow effects, and climate-related scenario analysis.

Financial effects do not apply to Tranche 3

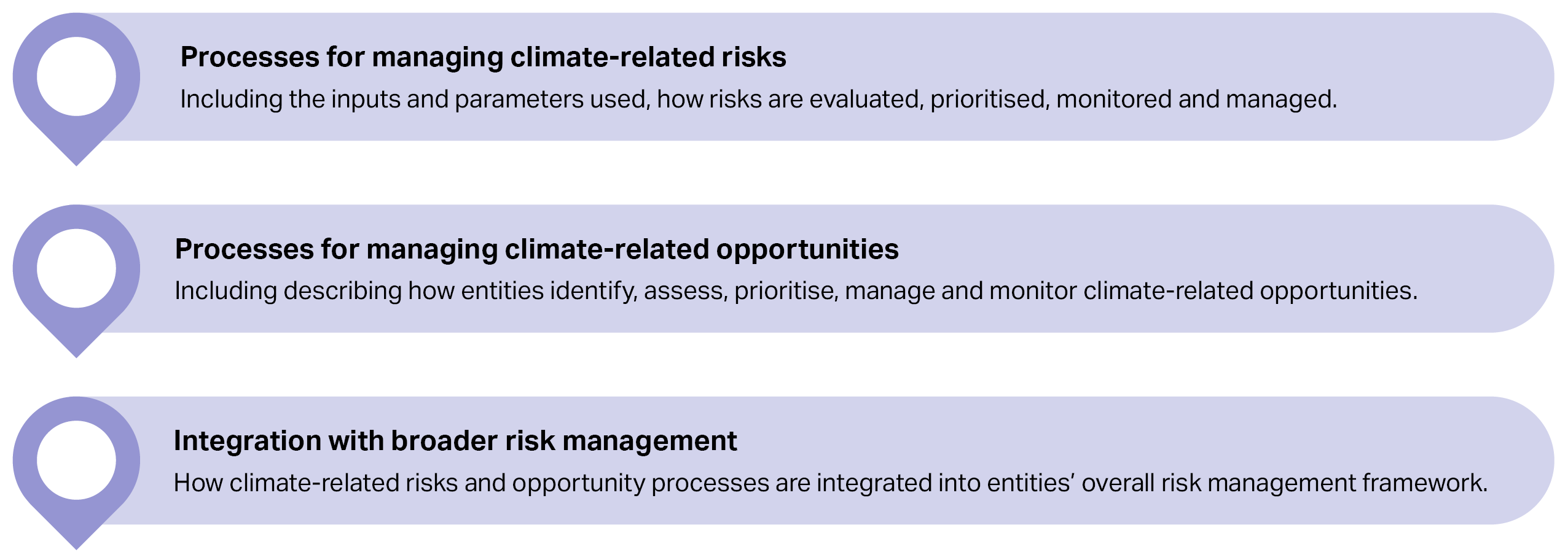

Risk management details processes to identify, assess, prioritise, manage and monitor risks and opportunities and shows integration with overall risk management. Risk management. Risk management criteria include the following key areas: processes for managing climate-related risks and opportunities, and integration with broader risk management.

Metrics and targets reports on Scope 1 and Scope 2 (and select Scope 3) emissions per the Emissions Reporting Framework, discloses targets, methodologies and progress. Metrics and targets criteria include the following key areas: climate related metric, entity performance, targets and goals for emissions and supporting information on targets and goals.

Further information on these pillars is available on Foundations of Climate Change Disclosure.