RMGs are guidance documents. The purpose of an RMG is to support PGPA Act entities and companies in meeting the requirements of the PGPA framework. As guides, RMGs explain the legislation and policy requirements in plain English. RMGs support accountable authorities and officials to apply the intent of the framework. It is an official’s responsibility to ensure that Finance guidance is monitored regularly for updates, including changes in policy/requirements.

A Government Business Enterprise (GBE) is a Commonwealth entity or Commonwealth company that is prescribed by the rules (s8 of the PGPA Act). Section 5 of the PGPA Rule prescribes ten GBEs: two corporate Commonwealth entities; and eight Commonwealth companies.

Guidance for Directors on the GBE governance framework is available in the GBE Directors Guide.

Government’s relationship with its GBEs

The Australian Government's relationship to its GBEs is similar to the relationship between a holding company and its subsidiaries, features of which include:

- a strong interest in the performance and financial returns of the GBE

- reporting and accountability arrangements that facilitate active oversight by the shareholder

- action by the shareholder in relation to the strategic direction of its GBEs where it prefers a different direction from the one proposed

- management autonomy balanced with regular reporting of performance to shareholders and

- boards that are accountable to shareholders for GBE performance, and shareholders that are accountable to Parliament and the public.

To enable greater public accountability, GBEs are required to prepare a Statement of Corporate Intent (SCI) (or a publically facing Corporate Plan) in consultation with Shareholder Ministers. An SCI focuses on the purpose and corporate outlook of a GBE, and expresses the expectations of its management in relation to future financial and non-financial performance.

Governance arrangements for GBEs

GBEs are governed by the PGPA Act and its rules and guidance. The following guidelines provide additional guidance on board and corporate governance, financial governance, and planning and reporting:

Finance’s Government Businesses

Finance's Commercial Division provides advice to the Australian Government relating to its GBEs and other commercial entities.

The primary tasks in relation to GBEs are to:

- provide sound strategic and analytical advice to the Government, in particular by engaging with the GBEs, analysing their operations and their environment, and consulting with stakeholders

- action the Minister's decisions including communicating objectives and

- ensure that there is a robust and sound governance framework in place by initiating change and contributing to policy development.

The Division also provides advice on other public non-financial corporations that are not prescribed as GBEs.

Audience

This guide is relevant to Government Business Enterprises (GBEs) that are Commonwealth entities (entity GBEs) or wholly owned Commonwealth companies (company GBEs)[1]. These GBEs are subject to the Public Governance, Performance and Accountability Act 2013 (PGPA Act) and prescribed in the Public Governance, Performance and Accountability Rule 2014 (PGPA Rule). Company GBEs are also subject to the Corporations Act 2001 (the Corporations Act), while entity GBEs are also subject to their enabling legislation.

[1] That is, where the Commonwealth has a 100 per cent ownership interest in the company.

Key points

Laws/rules/policy: This guide outlines the oversight arrangements for entity GBEs and company GBEs that are prescribed in the PGPA Rule.

Purpose: To provide guidance regarding board and corporate governance, planning and reporting, financial governance and other governance matters.

Previous guidance: This guide replaces the Commonwealth Government Business Enterprise Governance and Oversight Guidelines, August 2015.

Part 1 – Overview

Definition

1.1 A GBE is a Commonwealth entity or Commonwealth company as defined in section 8 of the PGPA Act and prescribed in section 5 of the PGPA Rule.

Application

1.2 This guide applies to GBEs that are entity GBEs and company GBEs.

- When forming subsidiaries or entering into joint ventures, GBE Directors are expected to consider the compliance of their company constitution or any shareholders’ agreement of the subsidiary with the GBE Guidelines.

1.3 For GBEs that are Commonwealth companies and that are not wholly owned companies, the extent to which this guide applies will be identified in legislation applying specifically to the GBE, the company constitution, or the shareholders’ agreement (see paragraphs 5.3 to 5.12 of this guide for more detail).

1.4 This guide is to be read in conjunction with the PGPA Act, the PGPA Rule and relevant Resource Management Guides that may be issued from time to time under the PGPA Act.

Principles

1.5 The main features of the Commonwealth’s relationship with its GBEs are:

- a strong interest in the performance and financial returns of the GBE

- reporting and accountability arrangements that facilitate best practice governance and active oversight by the Commonwealth

- action by the Commonwealth in relation to the strategic direction of its GBEs where it prefers a different direction from the one proposed.

1.6 The Commonwealth’s ownership interest is generally represented by two `Shareholder Ministers´. The Shareholder Ministers are the Responsible Minister (that is, the Minister responsible for the GBE) and the Finance Minister. The Finance Minister is generally the sole Shareholder Minister for those GBEs within the Finance portfolio.

1.7 The key principles underpinning the GBE Guidelines are:

- Shareholder Ministers exercise strategic control consistent with their accountability to the Parliament and the public

- Shareholder Ministers set clear objectives for GBEs

- The directors of a GBE are responsible for overseeing the development of the business strategies and the development of the day-to-day management policies.

- The directors of a GBE ensure that:

- the GBE´s activities are conducted so as to minimise any divergence of interests between the GBE and its Shareholder Ministers

- GBEs are managed in the best interests of the entity or company as a whole

- GBEs and their officers maintain the highest standards of integrity, accountability and responsibility.

- Required standards of disclosure to Shareholder Ministers are satisfied, consistent with requirements under the PGPA Act and other relevant reporting frameworks. This includes consultation with Shareholder Ministers on matters of significance and regular and timely disclosure of information:

- which may affect the value of the GBE

- which may influence government decisions in relation to the GBE

- in which the government has a legitimate interest.

- Information is produced for Shareholder Ministers and the community according to the highest standards.

- Where possible, information should be provided in a consistent format to enable ready comparison with information provided previously by the GBE. For example, the reporting of key metrics in Annual Reports and Corporate Plans. Generally accepted best practice reporting principles should be adopted where appropriate.

Mandate and Objectives

1.8 A principal objective for each GBE is that it adds to its shareholder value. To achieve this, it is expected to:

- operate efficiently, that is, at minimum cost for a given scale and quality of outputs

- price efficiently:

- A GBE is expected to set prices taking into account economic forces, including the level of demand for, and the enterprise’s capacity for and cost of supplying, individual goods and services.

- The government may impose price conditions on GBEs providing goods and services in a monopolistic market or Community Service Obligations (CSOs). Such price conditions and CSOs, where appropriate, would be in addition to those arising from regulation by the Australian Competition and Consumer Commission or as specified in legislation or through contractual arrangements.

- earn at least a commercial rate of return, after notional adjustments for any CSOs considered necessary by government, given the obligations in (a) and (b) above, to price and operate efficiently. This means:

- recovering the full cost of the resources employed, including the cost of capital

- working towards a principal financial target and a dividend policy, agreed in advance with Shareholder Ministers, with the principal financial target to be set on the basis that each GBE is expected to earn commercial returns at least sufficient to justify the long-term retention of assets in the business, and to pay commercial dividends from those returns.

1.9 In addition to setting a principal financial target, Shareholder Ministers may set other financial targets and non-financial targets, for particular GBEs, on a case-by-case basis in consultation with the GBE (refer to paragraphs 4.7 to 4.13).

1.10 A GBE is expected to operate in the industry sector, and provide the goods and services (including CSOs), that the government has mandated.

- The government may impose service quality standards on GBEs providing goods and services in a monopolistic market or on CSO goods and services

- In providing each GBE with a clear mandate and set of objectives, Shareholder Ministers will ensure that the objectives include any requirements to meet the government’s explicitly stated social and economic policy objectives.

1.11 The mandate of a GBE will be considered by Shareholder Ministers as part of the annual corporate planning process. Shareholder Ministers will, in consultation with the GBE’s board, provide further guidance on the purpose, role and limits on the activities of the GBE. This will be documented in the form of a Statement of Expectations or Commercial Freedoms Framework appropriate to the commercial activities, environment and risk profile of the GBE, having regard to the GBE’s mandate as agreed by the government while ensuring adequate Shareholder Minister oversight. In addition, a Funding or Financing Agreement may be negotiated with a GBE to prescribe the terms and conditions associated with any funding or financing the government may provide to the GBE. The Shareholder Ministers will, where appropriate, periodically undertake a stand-alone review of the mandate.

1.12 Under sections 22 and 93 of the PGPA Act, the Finance Minister may make a Government Policy Order (GPO) that specifies a policy of the Australian Government that is to apply to one or more GBEs. The GPO will take effect once registered on the Federal Register of Legislative Instruments, which will include details of the policy and its application. Ministerial orders to GBEs, including those prescribed in enabling legislation, and company constitutions, will be provided in writing.

Part 2 – Board and Corporate Governance

Board Responsibility and Conduct

2.1 The general conduct of directors (for GBE companies) and of boards (for GBE entities) is subject to the provisions of the PGPA Act and its Rules, the Corporations Act (for GBE companies), enabling legislation (where it exists), common law and equity.

2.2 Boards have ultimate responsibility for the performance of the GBE, and are fully accountable to Shareholder Ministers. Boards are expected to implement effective governance frameworks to support their role and responsibilities, and report on their implementation in the Annual Report.

2.3 Board members have their fiduciary and other duties drawn to their attention by Shareholder Ministers in correspondence offering appointment, and are to fully accept the individual responsibility this places on them.

- Appointment letters for all directors are expected to include:

- information about director powers and duties

- information about the term of appointment and remuneration arrangements, with particular reference to Remuneration Tribunal determinations

- a link to provide information about the online GBE Directors Guide

- a request that the director formally respond to the letter of appointment within 14 days of receipt, providing the undertaking referred to at paragraph 2.4

- a statement that, in accepting the position, the director agrees to their name and remuneration being publicly disclosed

- insurance and indemnity arrangements (if applicable to the GBE), expectations around confidentiality of information and board decisions, and procedures to manage conflicts of interest.

- The online GBE Directors Guide includes information and resource materials regarding the general operation and practices of GBEs, which includes:

- a GBE’s structure, role, purpose and accountability

- director roles and duties, including legislative and public sector accountability obligations and responsibilities

- financial management issues specific to GBEs

- planning and reporting requirements

- governance and regulation requirements such as Parliamentary scrutiny and audit processes.

2.4 Directors are expected to formally respond to the letter of appointment within 14 days of receipt and provide an undertaking:

- to advise Shareholder Ministers if there is any change in circumstances that might impact on their ability to be a director

- that they have reviewed the online GBE Directors Guide.

2.5 Boards are expected to regularly monitor the ongoing independence of each director and the board generally, to ensure that they continue to exercise unfettered and independent judgement.

- The board is expected to ensure that a director does not have any interests that derogate from carrying out the role intended with diligence and care.

- It is expected that the board will establish and maintain a formal register of directors’ interests to ensure potential conflicts can be identified and managed.

2.6 In particular, the government expects GBE boards to establish and maintain a code of conduct for directors (including any subsidiaries), employees and contractors and that GBEs, in undertaking their business, avoid activities that could give rise to questions about their political impartiality. For example, GBEs are not to make direct or indirect political donations or participate in activities that would bring the government into disrepute. GBEs may wish to consult with the Shareholder Ministers on any sensitive issues affecting its business activities.

2.7 The code of conduct may cover the following matters: being professional; customer service; work practices and performance; conflict of interest; relationship with suppliers; gifts and benefits; outside employment; appropriate use of assets and resources; and confidentiality of information, including privacy considerations in written and electronic form.

Board Appointments and Performance

2.8 GBE boards and any subsidiaries are to comprise directors with an appropriate mix of skills, who are to be appointed on the basis of their individual capacity to contribute to the board, having an appropriate balance of relevant skills (such as commerce, finance, accounting, law, marketing, workplace relations, management and other skills relevant to the GBE’s operations) to enable them to contribute to the achievement of the GBE´s objectives.

- Boards are expected to draw on outside expertise where necessary to augment their own skills

- The Chair is not expected to be an executive of the GBE, unless otherwise agreed by Shareholder Ministers. This clause does not apply to any subsidiaries

- The appointment of Commonwealth departmental officers (referred to as officials under the PGPA Act) to GBE boards may only be considered in exceptional circumstances, having regard to their possession of the skills referred to above, any potential conflicts of interest that might arise, and the particular circumstances of the GBE (such as GBEs in winding-down mode). In such cases, the appointed Commonwealth departmental officers are to act in the best interests of the GBE and at all times in accordance with the PGPA Act, the Corporations Act (for company GBEs), the Public Service Act 1999, and particularly the APS Values and APS Code of Conduct. All appointed board members are to act in accordance with the Shareholder Ministers’ objectives for the GBE.

2.9 The Chair is expected to head a board committee which provides Shareholder Ministers, through the board, with recommendations on board composition and membership.

- The Chair is to, following consultation with Shareholder Ministers, develop an Annual Board Plan which includes:

- the medium-term aims in relation to board composition, taking into account the strategic objectives of the GBE

- a forecast of likely board vacancies

- an assessment of the skill and diversity requirements of the board in the context of the strategic requirements of the GBE and government policy objectives regarding diversity in board composition. This is to have consideration of any assessment undertaken on the board’s performance (paragraph 2.21 refers).

- The Chair is expected to write to Shareholder Ministers at least three months prior to a vacancy arising on the board or in the role of CEO.

- Following consultation with Shareholder Ministers, the board may provide, through the Chair, a shortlist of candidates for board vacancies.

- Additional processes for identifying board candidates such as public advertising or the use of executive search processes may be undertaken by agreement with Shareholder Ministers, to help ensure appointments are drawn from the best possible field of candidates.

- Chairs may recommend the reappointment of an existing director where this is sought by the director and where appropriate (i.e. based on evidence of good performance, where the tenure falls within the requirements set out in legislation applying to the GBE, and where the term has not been excessive).

- All recommendations for appointment should have regard to any government skill and diversity requirements and policies.

- Through the Chair, the board is expected to advise Shareholder Ministers about its preferred candidate for the position of CEO. The CEO is directly accountable to the board and it is expected that potential candidates would be identified through public advertising or executive search processes.

2.10 Shareholder Ministers may elect to appoint a candidate not proposed by the Chair.

2.11 Any decision to appoint the CEO as a director is at the discretion of Shareholder Ministers and the CEO recruitment and succession arrangements undertaken by the board are expected to reflect this except where legislation states otherwise.

2.12 Boards are expected to implement and maintain a succession plan for CEO positions and provide an annual assurance to Shareholder Ministers that this is the case.

2.13 Where a Board appointment is proposed, Shareholder Ministers will consult the Prime Minister seeking his/her, or at his/her discretion the Cabinet’s, approval of the appointment before each appointment is finalised.

2.14 Board appointment and reappointment terms to GBEs and any subsidiaries are to be consistent with government policy. The process and consideration of Board appointments and reappointments are outlined in the Cabinet Handbook available on the Department of the Prime Minister and Cabinet’s website.

2.15 The Remuneration Tribunal determines a remuneration reference rate for directors that is commensurate with their roles and responsibilities. In setting remuneration, the Remuneration Tribunal may take into consideration a range of information including but not limited to the workload and work value of the office, fees in the private sector, wage indices and other economic indices and rates set for other bodies. The Remuneration Tribunal may also consider factors such as the non-cash benefits provided, and the public interest and personal status involved in holding the office.

2.16 GBEs are expected to have clear policies regarding the remuneration of directors on subsidiary boards and to consult with Shareholder Ministers in developing or revising these policies. Remuneration of subsidiary board members is expected to be set at a level proportionate to the Remuneration Tribunal’s decision for the parent GBE board taking into consideration, but not limited to, factors such as the decision making, workload and time commitments of directors on the subsidiary board.

2.17 Clear remuneration policies are also expected to exist for circumstances where directors hold positions on both the GBE parent and subsidiary board, or the GBE executive and subsidiary board, such that the policies reflect the additional responsibility and time commitment of the directors.

2.18 Boards are expected to review annually the composition of all subsidiary boards giving regard to any changes in the parent company’s strategies, independence and expertise of the directors.

2.19 Shareholder Ministers may, at their discretion, remove directors at any time prior to the completion of their term of appointment.

- In the event that a GBE is not performing satisfactorily, Shareholder Ministers will initiate prompt remedial action. Dismissal of the directors may be considered, particularly in any case where the GBE has failed to keep Shareholder Ministers adequately informed, and in situations of ongoing under-performance in respect of financial or other aspects of the operations of the business.

- A director may be placed in a situation where continuing to be a GBE director could embarrass the GBE or Shareholder Ministers. In such situations, they should raise the issue with their Chair immediately. The Chair, in turn, will decide whether it is necessary to raise the issue with Shareholder Ministers. In a worst case situation, the director may be asked to resign, or failing that, be removed.

2.20 While induction of board members is the responsibility of the GBE, boards are expected to work with Shareholder Departments, as representatives of Shareholder Ministers, to implement and maintain appropriate induction and development programs for directors. The online GBE Directors Guide is available on the Department of Finance’s website. Induction programs are expected to incorporate information on general public sector, legal, performance and accountability obligations.

2.21 On an annual basis the boards of the GBE and its subsidiaries are expected to assess its performance and performance of the Chair. The performance assessment of the GBE Board is to feed in to the GBE’s Annual Board Plan (paragraph 2.9 refers). Unless otherwise directed by Shareholder Ministers, on a biennial basis (every two years) a performance assessment of the GBE board is to be undertaken by an independent external party and the Chair is expected to provide the report to Shareholder Ministers.

- Part of any board performance assessment is expected to include a review of the level of director attendance at board meetings. Directors are expected to attend all scheduled board meetings, and attendance is to be reported in the Annual Report. Chairs are to raise on-going non-attendance issues with Shareholder Ministers for consideration and possible further action.

2.22 On an annual basis, the GBE board is expected to assess the performance of the CEO against predetermined criteria and a written record of its content is to be retained by the GBE board. Chairs are expected to provide annual written confirmation to Shareholder Ministers that this process has been completed.

2.23 Boards are expected to ensure that board committees and/or subsidiaries do not duplicate work performed by the CEO and management. The composition and charter of each board committee is expected to be reviewed by 1 December each year to ensure that they remain appropriate in the context of the governance needs of the GBE.

Part 3 – Planning and Reporting

Requirements

3.1 The planning and reporting requirements for GBEs are contained in the PGPA Act and PGPA Rule, with additional requirements for Commonwealth companies contained in the Corporations Act. The planning and reporting requirements are summarised in Table 1.

Table 1: Summary of Legislative Requirements

| Requirement | Commonwealth Entities | Commonwealth Companies |

|---|---|---|

| Corporate Plan content | Sections 35 of the PGPA Act and 16(E) of the PGPA Rule. | Sections 95 of the PGPA Act and 27(A) of the PGPA Rule. |

| Annual Reports | Sections 39 (inclusion of an Annual Performance Statement) and 46 of the PGPA Act and 16(F) of the PGPA Rule. | The Corporations Act, Section 97 of the PGPA Act and any relevant Rules. |

| Financial Statements | Section 42 of the PGPA Act. | The Corporations Act. |

| Additional Notification Requirements (Significant Events) | Section 19(1)(a) of the PGPA Act and any relevant Rules. | Section 91(1)(a) of the PGPA Act and any relevant Rules. |

Additional Notification Requirements (Changes in financial conditions and CSOs)

| Disclosure requirements for GBEs (Section 17BF of PGPA Rule). | Disclosure requirements for GBEs (Section 28F of PGPA Rule). |

| Supplementary Interim Reports | Section 19(1)(b) of the PGPA Act. | Section 91(1)(b) of the PGPA Act. |

| Performance Audit | Section 17 of the Auditor‑General Act 1997. | Section 17 of the Auditor‑General Act 1997. |

| Audit Committees | Section 45 of the PGPA Act and section 17 of the PGPA Rule. | Section 92 of the PGPA Act and section 28 of the PGPA Rule. |

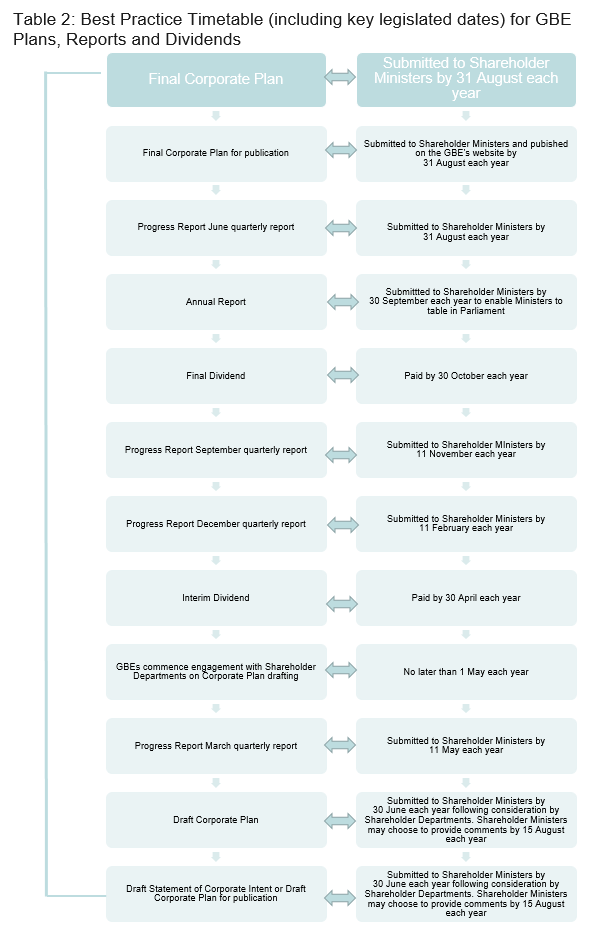

3.2 GBEs must provide Shareholder Ministers with a series of annual corporate planning and reporting documents for comment and review by the key dates shown in Table 2 (including dates legislated in the PGPA Act and PGPA Rule).

- GBEs are expected to engage with Shareholder Ministers and Shareholder Departments early in the reporting and planning processes to allow sufficient time for each GBE to build government priorities into the processes.

- In reviewing the documents, Shareholder Ministers and Shareholder Departments may seek clarification of the information provided, or request certain amendments.

Table 2: Best Practice Timetable (including key legislated dates) for GBE Plans, Reports and Dividends

Corporate Plans

3.3 Corporate Plans are to be prepared in accordance with the appropriate section of the PGPA Act, PGPA Rule and Corporations Act (refer summary at paragraph 3.1). See also Resource Management Guide No. 132 (Corporate plans for Commonwealth entities) and Resource Management Guide No. 133 (Corporate plans for Commonwealth companies).

- Corporate Plans must cover a period of at least four reporting periods (4 years) for the entity starting on the first day of the reporting period for which the Corporate Plan is prepared. Corporate Plans are also expected to include the financial results for the year immediately prior as a comparison. Details of matters to be included in Corporate Plans, as far as they are applicable, are outlined in

Table 3.

Table 3: Minimum Requirements and matters to be included in Corporate Plans

| PGPA Rule Minimum Requirements | Matters to be included in Corporate Plans for GBEs |

|---|---|

| Introduction |

|

| Purposes |

|

| Environment |

|

| Performance |

|

| Capability |

|

| Risk oversight and management |

|

Table 3a: Supplementary information requested by the Finance Minister under Sections 19(1)(b) and 91(1)(b) of the PGPA Act, to be included in Corporate Plans

| The supplementary information required unless otherwise agreed in writing: | Matters to be included in Corporate Plans for GBEs |

| Purpose |

|

| Performance |

|

| Capability |

|

| Financials |

|

| Risk oversight and management |

|

| Subsidiaries |

|

| Key Performance Indicator Targets |

|

Table 4: Minimum Key Performance Indicators for Corporate Plans

| Measure | Key Performance Indicator | Definition |

|---|---|---|

| Financial Performance | Total shareholder return | (Commercial value at end, less commercial value at start plus dividends paid less equity injected)/commercial value at start |

| Dividend yield | Dividends paid/average commercial value | |

| Dividend payout ratio | Dividends/net profit after tax (NPAT) | |

| EBIT | Earnings before net interest and tax | |

| EBITDA | Earnings before net interest, tax, depreciation, amortisation and fair value adjustments for financial instruments | |

| Return on equity (RoE) | Net profit after tax/average equity | |

| Net profit after tax (NPAT) | The bottom line of the Income Statement | |

| Underlying net profit after tax | The bottom line of the Income Statement adjusted for one-off items and Australian Accounting Standards Board (AASB) fair value movements | |

| Business Efficiency | Operating margin | EBITDA/operating revenue |

| Return on capital employed | EBIT adjusted for AASB fair value movements (net of tax)/average capital employed. Capital employed is defined as total assets less current liabilities | |

| Debtors age (days) | (Debtors/revenue) x 365 | |

| Leverage/Solvency | Gearing Ratio | Net interest bearing debt/net interest bearing debt plus equity |

| Interest Cover | EBITDA/interest paid | |

| Current ratio | Current assets/current liabilities | |

| Liquidity Ratio | Cash and equivalents/current liabilities | |

| Customers and Stakeholders | Customer Satisfaction | Percentage of customers rating the GBE very good or excellent as determined by survey |

| Meeting CSOs | Adherence to specific government directives, which cause GBEs to depart from otherwise commercial decisions, regarding the conditions of supply of goods or services | |

| Staff | Staff Retention and turnover rates | Number of staff replaced/average number of staff for the period |

| Staff Satisfaction | Percentage of staff very/extremely satisfied as determined by survey | |

| Lost time injury frequency rates and OHS incident rate | Lost time injuries per million hours worked | |

| Wages expense ratio | Cost of wages and salaries/operating revenue |

3.4 Shareholder Ministers may elect to meet with the directors of a GBE prior to responding to the draft Corporate Plan.

3.5 The response by Shareholder Ministers will:

- usually be within 45 days of receipt of the draft Corporate Plan

- Draft Corporate Plans are expected to be provided to Shareholder Departments for discussion with the GBE prior to being endorsed by the board to ensure a timely response.

- include (if necessary) any proposed changes to the draft Corporate Plan to better reflect the government’s policies and objectives for the GBE.

3.6 Shareholder Ministers may request the board to reconsider certain elements of the GBE’s draft Corporate Plan prior to finalisation.

3.7 Shareholder Ministers are not required to approve or agree a GBE’s final Corporate Plan, but draft Corporate Plans should be provided to Shareholder Ministers with sufficient time for Shareholder Ministers to provide comments if they wish to do so.

3.8 Generally, all GBE Corporate Plans and subsequent updates, reports or supplementary information are confidential to Shareholder Ministers, their advisers and Shareholder Departments.

Corporate Plans for publication

3.9 The directors of a company GBE or the board of an entity GBE must annually agree to a version of the Corporate Plan which must be a public document, in accordance with section 16E(3) and (4) of the PGPA Rule.

3.10 This document can take the form of a complete Corporate Plan, a redacted Corporate Plan, or a Statement of Corporate Intent. However, it must address the minimum requirements of the Corporate Plan as prescribed by the PGPA Rule (outlined in Table 3) and in doing so include sufficient non-confidential or commercially sensitive information to inform how the GBE plans to deliver on its purpose.

3.11 GBEs are to arrange for this document to be provided to Shareholder Ministers consistent with timings outlined in Table 2, and publish it on the GBE’s website by 31 August each year (the end of the second month of the reporting period for which it is prepared).

Progress Reports

3.12 Confidential quarterly progress reports are to be provided by the Chair to Shareholder Ministers by the dates specified in Table 2. The minimum requirement for progress reports is that they should include:

- analysis of the GBE’s quarterly and year-to-date performance against Corporate Plan forecasts for the corresponding period, including detailed analysis of revenue and expense (including capital expenditure) performance for the period and explanations for deviations from Corporate Plan forecasts

- financial statements in a format approved by the Finance Minister

- analysis of the GBE’s performance against its broader Corporate Plan objectives (such as its KPIs and operational performance targets/forecasts where relevant), including any major achievements during the period along with explanations for any changes to strategies

- an update on any emerging issues since the Corporate Plan and their potential consequence on performance, any material changes to identified risks and detailed strategies for managing these risks. These risks should be presented with the same level of details as required for risk reporting in Corporate Plans (refer Table 3a). This is in addition to the requirements set out in paragraph 4.15

- a clear statement of the GBE’s outlook for the rest of the financial year in terms of meeting its full year forecast, those risks that may result in financial results not being indicative of future performance of the GBE and opportunities arising and management plans

- commentary on progress in meeting CSOs (where relevant).

3.13 Shareholder Ministers may elect to respond to the Chair with specific comments on the progress reports.

3.14 All progress reports are confidential to the Shareholder Ministers, their advisers and the Shareholder Departments.

3.15 As per section 19(1)(b) and 91(1)(b) of the PGPA Act, Shareholder Ministers may request reports, documents and information on the activities of the GBE or any of its subsidiaries at any time.

Annual Reports

3.16 The directors of a GBE must provide an Annual Report to Shareholder Ministers in accordance with the requirements of the PGPA Act.

- Where a GBE is a Commonwealth entity, the Annual Report must be prepared in accordance with the PGPA Act, the PGPA Rule, the entity’s enabling legislation and any other applicable legislation and guidance issued by the Finance Minister. The Annual Report must also include an Annual Performance Statement.

- Where a GBE is a company, the Annual Report must be prepared in accordance with the PGPA Act, the PGPA Rule, the Corporations Act and any other applicable legislation and guidance issued by the Finance Minister.

- GBEs are expected to include comments on performance against the financial and non‑financial expectations outlined in the Corporate Plan for publication relating to that financial year, including on any subsidiary.

- GBEs are expected to include the financial results of all subsidiaries in their Annual Reports.

3.17 GBEs are expected to detail in their Annual Report key governance practices. This information can be modelled against the ASX Corporate Governance Principles and Recommendations and may include, but is not limited to:

- board committees of the company and their main responsibilities

- education and performance review processes for directors

- ethics and risk management processes.

3.18 Financial statements of GBEs and their subsidiaries presented in Annual Reports are audited, or reported on, by the Auditor-General under the circumstances outlined in the Auditor-General Act 1997.

3.19 GBEs are to note that the Auditor-General is able to conduct a performance audit of an entity GBE or a company GBE, or any of its subsidiaries, in the circumstances outlined in the Auditor-General Act 1997.

3.20 GBEs are also expected to include in their Annual Reports the minimum standards outlined in the Voluntary Tax Transparency Code, which has been developed by the Board of Taxation to promote more transparency in tax reporting by medium and large businesses.

3.21 GBEs are expected to report all relevant information relating to the remuneration packages of all individuals who constitute the executive management of the GBE on a disaggregated basis. As a minimum, this is to include the CEO and their direct reports.

3.22 The GBE should be conscious of its obligations under the Privacy Act 1988 when disclosing an individual’s remuneration. It is the responsibility of the GBE to ensure consent has been granted by executives captured under this guidance.

3.23 GBEs are expected to use the Remuneration Disclosure template below when preparing this information.

Table 5: GBE executive remuneration disclosure template

| GBE executive remuneration disclosure template | |||||||||

| Short term benefits | Post-employment | Other long term benefits | Termination benefits | Total remuneration | |||||

| Base salary and fees | STI/ Bonuses | Non-cash benefits | Superannuation contributions | STI deferral | Long service leave | ||||

| Senior Executives | |||||||||

| Name | Previous Year | ||||||||

| Current Year | |||||||||

| Name | Previous Year | ||||||||

| Current Year | |||||||||

| Name | Previous Year | ||||||||

| Current Year | |||||||||

| Total | Previous Year | ||||||||

| Current Year | |||||||||

| Total executive management | Previous Year | ||||||||

| Current Year | |||||||||

Keeping Shareholder Ministers Informed

3.24 Notification requirements are contained in the PGPA Act for both entity (section 19) and company (section 91) GBEs.

3.25 In accordance with the PGPA Act, the board of an entity GBE or the directors of a company GBE must keep Shareholder Ministers informed of the activities of the GBE and its subsidiaries, and follow a disclosure principle which is similar to the continuous disclosure requirements of the ASX Listing Rules.

- If a GBE becomes aware of any information that may have a material effect on its value and/or performance, that information must be provided immediately to Shareholder Ministers. This may include significant changes to the business environment and risks which may impact on the achievement of planned activities and financial projections such as revenue and dividends.

- Directors must provide such other information in relation to the GBE’s activities as Shareholder Ministers require, within the time limits set by the Shareholder Ministers.

- Where there are two Shareholder Ministers, all correspondence and reports from GBEs must be sent to both Shareholder Ministers simultaneously. Whilst Shareholder Ministers will consult in relation to all correspondence, they may decide that, in relation to some matters, one of the Shareholder Ministers will correspond on behalf of both Shareholder Ministers.

- Shareholder Ministers may consult with the Prime Minister and/or other Ministers about any material matter affecting the value of the GBE and in doing so may provide copies of Corporate Plans, progress reports and correspondence on other major matters to the Prime Minister and/or other Ministers for possible comment.

3.26 Proposals for significant business initiatives are expected to be developed for inclusion in the normal corporate planning cycle. The threshold value at which an initiative is considered significant will be agreed and defined within the Commercial Freedoms Framework or Statement of Expectations.

- If an urgent initiative arises which is unable to wait for inclusion in the planning cycle, it is to be treated as a notifiable significant issue, pursuant to section 19 (entity GBEs) and section 91 (company GBEs) of the PGPA Act. GBEs must notify Shareholder Ministers prior to entering into any identified business opportunities. This is expected to include, but not be limited to, new business ventures, major contracts and capital raising proposals.

3.27 Unless otherwise agreed, GBE boards are expected to submit business cases outlining new proposals above agreed thresholds to Shareholder Ministers for consideration either as part of the Corporate Plan or separately for urgent initiatives as outlined in paragraph 3.26. GBEs are expected to distinguish between business cases that relate to core business and those that relate to non-core business. The threshold dollar value for consultation for proposed non-core business opportunities will be lower than that for core business opportunities and are to be agreed in consultation between the board and Shareholder Ministers as part of the annual corporate planning process, unless the threshold has been separately agreed with Shareholder Ministers (for example, as part of a Commercial Freedoms Framework). As a minimum, business cases are expected to address the following:

- the rationale for the initiative and an explanation of how it fits into the GBE’s corporate strategy

- cost, anticipated return (net present value), effect on shareholder value and some measure of the initiative’s risk

- key assumptions around revenue and costs (including base case, scenarios and sensitivity analysis), plus identification and quantification of key risks and mitigation strategies

- proposed funding or financing strategy

- the impact on the GBE’s capital structure and credit rating (if applicable)

- expected outcome, and impact on future dividends.

3.28 GBEs are expected to allow a reasonable amount of time (not less than 10 working days) for Shareholder Ministers and Shareholder Departments to respond to any business case, and factor that into the decision making timeframe.

3.29 All business case proposals, subsequent updates and supplementary information are to be treated as commercial in confidence by Shareholder Ministers, their advisers and the Shareholder Departments.

3.30 GBEs are expected to conduct Annual Strategic Meetings, to which Shareholder Ministers or their delegate(s) are invited to attend. The focus of the meetings will be to discuss both the board’s and the GBE’s performance over the past year, and to engage on the development of strategy going forward.

Audit Committees

3.31 Under section 45 of the PGPA Act and section 17 of the PGPA Rule (for Corporate Commonwealth entities) and section 92 of the PGPA Act and sections 17 and 28 of the PGPA Rule (for Commonwealth companies), GBEs are required to have an Audit Committee to provide independent advice and assurance to the entity’s accountable authority (i.e. the board). The relevant sections of the PGPA Rule also to require the accountable authority to determine the functions the audit committee is to perform for the entity.

3.32 The Audit Committee’s written charter determines the functions of the audit committee for the entity. The functions must include reviewing the appropriateness of the GBE’s:

- financial reporting

- performance reporting

- system of risk oversight and management, and

- system of internal control.

Part 4 – Financial Governance

Capital Structure and Dividend Policy

4.1 Each GBE and its subsidiaries are expected to target an optimal capital structure (the combination of financial liabilities and equity used to fund the assets of the GBE) that is agreed annually between the board and Shareholder Ministers in the Corporate Plan consultation process.

- An optimal capital structure is one that, in light of economic, industry and GBE specific factors, would provide for an investment grade credit rating, whilst at the same time imposing a discipline on the GBE to optimise efficiency. The standalone target credit rating is BBB.

- As part of developing a target optimal capital structure, consideration is expected to be given to the forecast level of capital expenditure in the GBE’s Corporate Plan, and appropriate options for funding capital expenditure (including via retained earnings or debt). Consideration is also to be given to longer term objectives outlined in a GBE’s Corporate Plan.

- In providing for a GBE to expand its capital base through retained earnings, any proposed future capital expenditure is expected to add shareholder value. That is, as a minimum, capital expenditure plans should meet a hurdle rate of return that is consistent with the GBE’s principal financial target (Refer paragraphs 1.8 and 4.7 – 4.13 ‘Financial Targets for GBEs’).

4.2 The level of estimated dividends (and forecast payout ratio) for a GBE and its subsidiary should be agreed annually between the GBE and the Shareholder Ministers through the Corporate Plan consultation process, and is expected to have regard to the maintenance of, or progress toward, its optimal capital structure.

- The level of estimated dividends shall be driven by the desired capital structure, the profitability of the enterprise, and the level of agreed future capital expenditure.

- The proposed dividend payout ratio and estimated dividend payment should be included in the Corporate Plan for each year covered by the Corporate Plan.

- The agreed dividend payout ratio should take account of the government’s preference for dividends over capital gains.

- Profits generated by subsidiaries are to be taken into account in agreeing the level of estimated dividends and forecast payout ratio.

4.3 Dividends are expected to be paid in two installments: an interim dividend and a final dividend.

- Interim dividends are payable by 30 April and final dividends by 30 October.

- Shareholder Ministers may agree on variations to those dates, after consultation with the board of the GBE.

4.4 Interim and final dividends to be paid must be agreed between the board and Shareholder Ministers, as soon as possible after the quarterly progress reports for the periods ending December and June have been received by Shareholder Ministers.

4.5 The capital structure of a GBE is expected to be reviewed where the application of dividend policy has not led to, or is unlikely to lead to, an optimal capital structure within a reasonable period of time.

4.6 Dividend policy for partly owned GBEs is expected to have regard to the above principles, the extent of Commonwealth ownership, and the views of other shareholders.

Financial Targets for GBEs

4.7 All GBEs are expected to add to shareholder value in their operations with a view to at least meeting financial targets set out in their Corporate Plan.

- Increases in shareholder value are achieved when the GBE’s Weighted Average Cost of Capital (WACC) is exceeded, regardless of whether or not the target return is reached. However, where a GBE achieves a return which is less than its financial target, it has not achieved the minimum return acceptable to Shareholder Ministers who expect the adoption of strategies aimed at achieving the target.

4.8 Setting appropriate financial targets aims to:

- ensure that GBEs operate and price their goods and services efficiently

- provide an environment for GBEs which is competitively neutral with the private sector.

4.9 GBEs (other than those covered under paragraph 4.10) are expected to target a specific WACC. This principal financial target requires the GBE to earn returns sufficient to cover the cost of debt and the required return on equity. WACC is used to estimate the required rate of return on total assets, taking into account the different required rates of return attached to the different components of the GBE’s capital structure.

- The cost of debt is the expected rate at which the GBE is able to borrow.

- The required return on equity is the risk free rate plus a risk premium appropriate to the GBE.

4.10 For GBEs that are service-based and therefore carry little debt as part of their optimal capital structure, the cost of the equity element of the WACC can be targeted (rather than the WACC itself) as the principal financial target. This target is the risk free rate (government bond rate) plus a risk premium appropriate to the GBE.

4.11 Any other financial targets which might be set for particular GBEs are expected to be consistent with the objective of increasing shareholder value. In some cases, such as for newly established GBEs, it may be appropriate to target the achievement of relevant principal and other financial targets over the medium-term. Nevertheless, establishing appropriate financial targets is required to drive the decisions of the GBE.

4.12 Shareholder Ministers will agree with each GBE the methodology they will use to measure performance against their principal financial target and other financial targets. These measures will be based on shareholder value added, and the change in shareholder value added year-on-year.

4.13 Financial targets are not to be adjusted for any unfunded components of CSOs. Rather, any adjustments considered necessary are expected to be made notionally to the GBE’s actual revenues.

Managing Risks

4.14 GBE boards are responsible for managing risks. Boards are therefore expected to establish processes and practices within the GBE to manage all risks associated with the GBE´s operations.

4.15 All GBEs are encouraged to consider applying the Commonwealth Risk Management Policy and Guide to Implementing the Commonwealth Risk Management Policy published by Finance in relation to risk management frameworks and systems.

4.16 As indicated in paragraph 3.32, the GBEs Audit Committee’s functions must include reviewing the appropriateness of the GBE’s system of risk oversight and management; and system of internal control.

4.17 GBE boards must keep Shareholder Ministers informed of risk management strategies by outlining them in Corporate Plans and progress reports, and other reports when necessary. In addition, Corporate Plans and progress reports are expected to contain a statement from the board that the GBE has appropriate risk management policies and practices in place and that adequate systems and expertise are being applied to achieve compliance with those policies and procedures.

4.18 The Commonwealth, as a shareholder, is sensitive to commercial risk. In some circumstances, it may therefore choose to set limits on the activities of particular GBEs; for example, on liabilities, financial exposures, use of derivative instruments, etc.

- In normal circumstances, a GBE should only use derivative financial instruments for the purpose of hedging exposures.

4.19 As a general rule the Commonwealth will not provide formal guarantees of GBE liabilities. Accordingly, GBE boards are expected to take this policy into account when making decisions which affect a GBE’s operations and performance.

- Guarantees provided in the past continue to apply to existing borrowings until they mature, in order to protect the interests of investors.

4.20 GBE boards are expected to engage in normal tax planning activities that are within the spirit of the law. It is not appropriate for GBEs to lead the market in aggressive tax planning strategies.

GBE Borrowings

4.21 Ongoing oversight of GBE borrowings is an integral part of the Corporate Plan and progress report processes, as outlined in Part 3 of this guide.

4.22 The government will consider sanctioning borrowing proposals beyond the first forward year for GBEs that have a proven track record of good performance and accountability, and which provide appropriate justification (including expected rates of return) in Corporate Plans to support proposed capital expenditure programs.

4.23 GBEs will usually borrow from financial markets. Under section 57 of the PGPA Act, borrowing by corporate Commonwealth entities (either through the Commonwealth budget or privately) requires express authorisation by or under an Act, or by the Finance Minister in writing, or by the PGPA Rules. GBEs that are Commonwealth corporations are expected, as best practice, to consult with Shareholder Ministers on any major borrowing proposals.

- GBE boards are expected to be aware that some lenders will want to include in their loan documentation the right to call up their loan(s) if the control of the GBE changes. Shareholder Ministers prefer that GBE boards do not agree to such clauses being included in loan documentation or to any other clauses that would be triggered, at the lender's discretion, by an ownership change.

4.24 Company GBEs are expected to avoid issuing debt securities that would bring them within the definition of a "disclosing entity" under the Corporations Act.

- This will minimise the potential for conflict between the information provision requirements of the PGPA Act, this guide, and the Corporations Act.

Part 5 – Other Governance Matters

Workplace Relations

5.1 Subject to this guide, GBEs are free to manage relations with their employees consistent with the Fair Work Act 2009 and in accordance with the following:

- The CEOs of GBEs are, with limited exceptions, covered by the Remuneration Tribunal’s Principal Executive Office (PEO) Classification Structure and Terms and Conditions. As such, the board, where it is the employing body, determines the remuneration and allowances for the office consistent with the PEO framework.

- If the Employing Body considers a revision to the CEO’s remuneration is appropriate it should consult with Shareholder Departments prior to approaching the Remuneration Tribunal.

- GBEs are encouraged to apply the Government’s workplace relations policy.

- Any matters specified from time-to-time by the Minister responsible for workplace relations policy, after consultation with the Prime Minister and the Finance Minister.

- In making appointments of executive, management and senior staff, GBEs are to have regard to government policy on fostering a culture that embraces diversity and that supports a high performing Australian Government public sector.

5.2 Superannuation arrangements for GBEs are covered by the Superannuation Benefits (Supervisory Mechanisms) Act 1990 (the Superannuation Benefits Act). GBEs (except with respect to any staff employed under the Public Service Act 1999) are able to establish and operate superannuation arrangements of their choice, provided that any relevant prescribed requirements made under the Superannuation Benefits Act are complied with.

Partly Owned GBEs

5.3 Where the government decides to move to, or adopt, partial ownership of a GBE this guide applies to the maximum extent possible, consistent with minimising the risk of an oppression action by minority shareholders under Part 2F.1 of the Corporations Act.

5.4 Government approval is required for any proposal to set up a partly owned GBE, or to change Commonwealth ownership of an existing GBE from whole to partial ownership (including by the introduction of employee share ownership schemes). The approval may anticipate a continuous process of a reduced share or level of Commonwealth ownership leading to transfer of the controlling interest to other parties and to eventual sale of all of the Commonwealth’s interest.

5.5 Where the government decides to move to partial ownership of a GBE in which it is likely to retain a controlling interest for a period of time, Shareholder Ministers, in consultation with the Attorney-General, will, before any shares in the GBE are sold or issued:

- review any enabling or other relevant legislation and the company constitution or memorandum and articles of association (M&As) of the GBE (as applicable), to assess the extent to which they are consistent with this guide.

- provide, through a Shareholder Ministers´ agreement with potential owners and/or changes to the enabling legislation and the M&As or company constitution (where applicable), for this guide to apply to the maximum extent consistent with the policy objectives the government is pursuing through its movement to partial ownership of the GBE.

5.6 In negotiations with potential other owners of a GBE that the Commonwealth will not control, Shareholder Minister will aim to have this guide applied to the maximum extent possible, having regard to the policy objectives of the government in the circumstances.

Partly Owned Subsidiaries of GBEs and Joint Ventures involving GBEs

5.7 GBEs are generally free to establish partly owned subsidiaries, purchase control of other companies or enter into joint venture arrangements; however under paragraph 3.26 of this guide they must notify Shareholder Ministers of significant proposals to form subsidiaries, joint ventures, etc[1].

- When becoming involved in joint ventures, GBEs are expected to generally adopt the incorporated form or enter into the joint venture through a subsidiary.

5.8 Where a GBE establishes a wholly owned subsidiary, or purchases a 100 per cent interest in a company (thereby creating a subsidiary), the board of the GBE is expected to ensure, prior to any move to partial ownership of the subsidiary, that no obstacles are present in the company constitution, and there is no capacity for any shareholders of the subsidiary, to prevent the GBE from complying with this guide for as long as the Commonwealth has a controlling interest in the subsidiary through the GBE.

- Where the GBE has any subsidiary it will ensure that control of the affairs of that subsidiary will be exercised by a majority of the directors of that subsidiary, who are directors or employees of the GBE or have been approved by Shareholder Ministers for appointment as directors of that subsidiary.

5.9 Where a GBE establishes a subsidiary with less than 100 per cent ownership, or purchases a controlling interest in a company with less than a 100 per cent ownership, the directors of the GBE are expected to ensure, primarily through the company constitution and any shareholders´ agreement of the subsidiary, that the subsidiary operates so as to enable the GBE to comply with this guide to the maximum extent possible.

5.10 The above requirements relating to GBEs establishing subsidiaries do not apply to cases in which a GBE is undertaking equity investment and promotion of companies as part of its day-to-day business operations (for example, a GBE which provides financial services as its core function) provided Shareholder Minister have notified the GBE of the types of investments which are exempt.

5.11 Where a GBE, or one of its subsidiaries, becomes involved in a joint venture the GBE is expected to ensure that the reporting and control arrangements relating to the joint venture enable the GBE to satisfactorily meet its obligations under this guide.

5.12 Shareholder Ministers will ensure that there are no provisions in enabling legislation, company constitutions, guidelines to directors or shareholders´ agreements, of a GBE which would prevent the GBE from complying with the requirements outlined above relating to subsidiaries and joint ventures.

Arrangements for GBEs Being Established, Sold, Restructured or Wound Up

5.13 This guide applies in full to GBEs during an establishment, sale or restructuring, or winding-up process, until Shareholder Ministers decide on variations to facilitate the establishment, sale/restructuring or winding-up process and to streamline reporting. The board will be advised of variations.

5.14 Where a scoping study, or other review, is undertaken by government, Shareholder Ministers will advise of any particular requirements or expectations of the GBE in this context.

5.15 Where a decision has been taken to sell all or part of the Commonwealth’s interest in a GBE, or where the possibilities of sale are being explored, the board and management of the GBE must provide full co-operation and requested information to the government during the period leading up to the sale.

[1] Also refer to PGPA Act, section 19 for authorities and section 91 for companies.

Resources

Other relevant publications include:

- The online GBE Directors Guide

- Resource Management Guide 131 Developing Performance Measures

- Resource Management Guide 132 Corporate Plan for Commonwealth entities

- Resource Management Guide 133 Corporate Plan for Commonwealth companies

- Resource Management Guide 134 Annual performance statements for Commonwealth entities

- Resource Management Guide 136 Annual Reports for corporate Commonwealth entities

- Resource Management Guide 137 Annual Reports for Commonwealth companies

- Resource Management Guide 202 Audit Committees

- Resource Management Guide 203 General duties of officials

- Resource Management Guide 211 Implementing the Commonwealth Risk Management Policy

- ASX Listing Rules

- ASX Corporate Governance Principles and Recommendations (See the heading: Corporate Governance Disclosures).