Overview

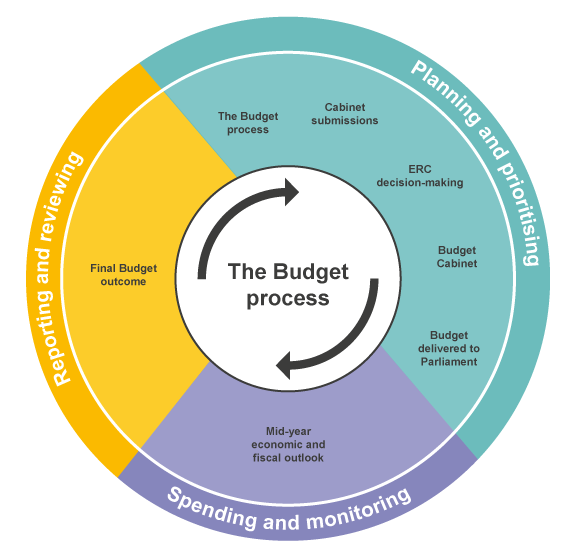

The Budget process is the decision-making process for allocating public resources to the Government’s policy priorities. It is through the Budget process that the government gains the Parliament’s authority to spend relevant money through the passage of the annual appropriation acts and other legislation that establishes special appropriations.

The Charter of Budget Honesty Act 1998 (the Charter) sets out principles and requirements that guide the government’s management of fiscal policy.

The Budget Process Operational Rules (BPORs) are standing rules endorsed by the Cabinet that outline the major administrative and operational arrangements for managing the Australian Government Budget (the Budget) and its related processes. This version of the BPORs came into effect on 18 December 2023 and is in effect until revised – officials should contact their agency or portfolio external budget teams to ensure they have access to the most up to date BPORs.

Portfolio Ministers can bring forward policy proposals for consideration by the Government during the annual Budget process.

Finance supports the Government in its Budget preparation, delivery and ongoing management through the Budget Process. Finance provides policy and financial advice to the Minister for Finance and the Expenditure Review Committee (ERC) of Cabinet on Government expenditure and non‑taxation revenue in order to produce the Budget and other major economic updates throughout the year.

Finance has an obligation to ensure that the Budget estimates related to expenditure or capital that are presented to the government are reliable, and meet the requirements of the Charter.

Finance is also responsible for ensuring Budget estimates, processes and documentation are prepared and delivered in an accurate and timely manner. This requirement is one of Finance’s deliverables (set out in Finance’s Portfolio Budget Statement).

Economic Updates

Budget

Annual forecasts are published at the General Government Sector (GGS) level (Budget Papers) and the portfolio and entity level (Portfolio Budget Statements). The Budget Papers are prepared by the Treasury and Finance and set out the details of the Budget for the parliament and for the Australian public.

What is the role of Commonwealth entities in the Budget context?

All Commonwealth entities are required to keep their estimates and actuals reporting up-to-date in both their internal records system and Central Budget Management System (CBMS), to ensure that all public reporting is accurate and consistent. Estimates often need to be amended in line with new Budget decisions, changes in whole-of-government parameters (such as the Consumer Price Index or currency exchange rates variations), or changes to the Machinery of Government (MoG).

Mid-Year Economic and Fiscal Outlook

The Government produces a Mid-Year Economic and Fiscal Outlook (MYEFO) report by the end of January each year, or within six months after the last Budget has been presented to the Parliament, whichever is later. Typically, MYEFO is released in December.

MYEFO provides updated information on the Government’s fiscal position and compares estimated expenditure to actual expenditure. MYEFO estimates include any Government decisions made since the previous Budget that affect expenses, revenues and capital estimates. MYEFO also updates the budgetary position, including Budget aggregates, by incorporating any changes to economic parameters.

Portfolio Ministers can propose new or amended proposals, using the same process as for Budget proposals, however, the expectation is that these should only be proposed if the need is urgent, unavoidable, and cannot be considered by the Government as part of the next Budget.

Final Budget Outcome

The Final Budget Outcome provides the final fiscal outcomes for the preceding financial year and is based on external reporting standards. The Charter of Budget Honesty Act 1998 requires that a Final Budget Outcome be released no later than three months after the end of the relevant financial year. The financial statements in the Final Budget Outcome are similar to those in the budget but provide actual outcomes rather than estimates.