Audience

This guide applies to all officials, particularly chief financial officers and finance teams, in Commonwealth entities that enter into contracts that transfer insurance risk to another party.

Key points

This guide:

- provides guidance for determining whether insurance arrangements established by Commonwealth entities are classified as general insurance contracts, in the context of Australian Accounting Standards Board (AASB) 1023 General Insurance Contracts (AASB 1023)

- only applies to general insurance contracts under AASB 1023, even where an entity does not conduct an insurance business

Introduction

Commonwealth entities are required to prepare their annual financial statements in accordance with the AAS and the Public Governance, Performance and Accountability (Financial Reporting) Rule 2015 (FRR).

AASB 1023 details the accounting requirements for general insurance contracts. While there are various types of insurance contracts, for AASB 1023 purposes, a general insurance contract is an insurance contract that is not a life insurance contract.

This guide assists entities in identifying whether a general insurance contract exists for AASB 1023 accounting purposes.

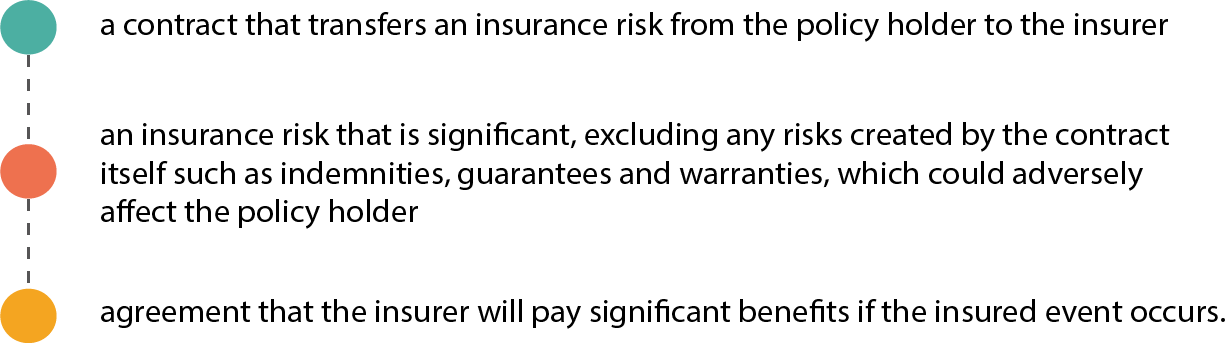

An insurance contract is a contract under which one party (the insurer) accepts significant insurance risk from another party (the policyholder) by agreeing to compensate the policyholder if a specified uncertain future insured event, adversely affects the policyholder.

For an insurance contract to exist, there must be:

Under the definitions provided at paragraph 19.1 of AASB 1023, a general insurance contract is an insurance contract that is not a life insurance contract. Any contract that transfers insurance risk from one party to another and is not a life insurance contract could be a general insurance contract. Under AASB 1023, any entity that issues an insurance contract is an ‘insurer’, whether or not that entity is regarded as an insurer for legal, regulatory or supervisory purposes.

Example 1: Contracts that are general insurance contracts

Contracts that are general insurance contracts, where the transfer of insurance risk is significant, include:

- insurance against theft or damage to property

- insurance against product or professional liability or legal expenses

- medical cover

- surety bonds, fidelity bonds, performance bonds and bid bonds

- travel assistance (i.e. compensation for losses suffered while travelling).

Figure 1 shows the elements that must all be present for an agreement to be a general insurance contract. References to Appendix A of AASB 1023 are included, however, these do not replicate the appendix. Other paragraphs of AASB 1023 may also be relevant to users of this guide in determining whether a general insurance contract exists.

Figure 1: An insurance contract only exists if all the following elements are present

Entities must advise Comcover as soon as practicable if any risk that is covered by Comcover is also covered under a separate insurance policy.

Assessing the significance of risks and benefits

In determining whether a Genera insurance contract exists, entities will need to apply professional judgement in assessing whether the:

- insurance risk being transferred from the policyholder to the insurer is significant

- policyholder will derive significant additional benefits from the insurer if the insured event occurs.

The significance of the insurance risk needs be assessed on a case-by-case basis, in accordance with the entity’s risk management policy.

Example 2: Significance of an insurance riskA Commonwealth company (that is not classified to the GGS) enters into an insurance contract to cover the risk associated with flood or earthquake damage. While the likelihood of the insured event occurring may be low, the consequences of a flood or earthquake could be high. |

Example 3: Significance of additional benefitIf the benefit payable is similar to the interest the policyholder would receive if they invested the insurance premium, then the additional benefit would not be significant. |

Below are examples of contracts that are not general insurance contracts. Also see the examples at Appendix A, paragraph 18 of AASB 1023.

Example 4: Contracts that are not general insurance contractsExamples of contracts that are not general insurance contracts include:

|

Appendix A, paragraph 18(b) of AASB 1023 notes that self-insurance is not a general insurance contract.

Self-insurance occurs where a risk that could be covered by an insurance contract is retained. Under self-insurance arrangements, there is no insurance contract as there is no agreement to the transfer of an insurance risk to another party.

Other contracts that do not meet the General Insurance Contract definition

Where a contract does not satisfy the definition of a general insurance contract, the entity should consider whether the following AAS apply:

- AASB 4 Insurance Contracts – applies to fixed-fee service contracts that meet the definition of an insurance contract such as maintenance contracts or roadside assistance contracts

- AASB 15 Revenue from Contracts with Customers – where a contract does not create financial assets or financial liabilities

- AASB 137 Provisions, Contingent Liabilities and Contingent Assets – in respect to legal and constructive obligations and contingent liabilities, such as product warranties and refund policies issued directly by a manufacturer or retailer

- AASB 9 Financial Instruments – where a contract creates financial instruments such as financial guarantees, loans and receivables, and derivatives

- AASB 1038 Life Insurance Contracts – in relation to life insurance contracts.

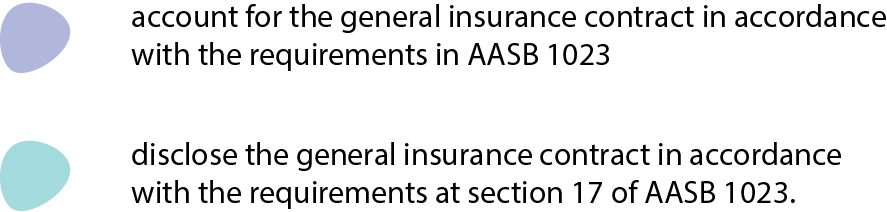

Where a general insurance contract exists, entities are to: