Public Governance, Performance and Accountability Rule 2014 section 16E(2) – item 5(b)

The performance measures meet this requirement when they specify targets for each performance measure, for which it is reasonably practicable to set a target, for each reporting period covered by the plan (that is, a minimum of 4-years).

Establishing targets

Targets for each performance measure should be provided in the corporate plan where it is reasonably practicable to set a target.

Performance information is more informative if performance can be compared qualitatively or quantitatively against particular performance levels.

Where possible, targets for performance measures should be specific, measurable, time-bound and reportable. They should also be challenging but achievable.

Entities may use a combination of methods to establish targets for performance measures, such as:

- current performance

- current performance plus/minus a percentage improvement change

- averaged performance

- quality specifications or benchmarks.

Entities should include a description of an entity’s rationale for setting particular targets.

Entities are encouraged to consider how incremental improvements could be demonstrated over time. Where a target has historically been exceeded, or is static for a period of time, entities should regularly review the target or explain why the target has been maintained at a certain level.

Entities should take care to ensure that targets do not promote adverse results. For example, where an entity focuses on improving efficiency to a point where the quality of goods and services is substantially decreased or practices are adjusted to meet a target rather than achieve desired outcomes.

To ensure that targets are not unrealistic or create perverse incentives:

- targets should be set through entity planning processes

- proposed targets should be trialled in parallel to existing targets

- targets should be presented in the context of the service being delivered.

To assist the reader in understanding the entity's performance targets, entities should avoid the use of acronyms or jargon when introducing the target or provide further explanation when acronyms or jargon are used.

Not reasonably practicable to set a target

Circumstances where it may not be reasonably practicable to set a target could be where:

- data that would allow the setting of a target is not available or difficult and resource intensive to establish (for example, for policy development and policy administration functions)

- where a baseline is being developed.

Where targets are not provided, it is a better practice to provide an explanation in the corporate plan of the reasons why targets have not been included.

Better practice principles:

- Targets for each performance measure are required in the corporate plan where it is reasonably practicable to set a target.

- Where possible, targets should be specific, challenging but achievable, measurable, time-bound and reportable.

- Entities should include a target rationale in the corporate plan.

- Entities should regularly review their targets, particularly where a target has historically been exceeded, or is static for a period of time, and outline why the target has been maintained at a certain level.

- Entities should ensure that targets do not promote adverse results or perverse incentives.

- There are circumstances where it may not be reasonably practicable to set a target (for example, establishing a baseline).

- Where targets are not provided, it is a better practice to provide an explanation in the corporate plan of the reasons why targets have not been included.

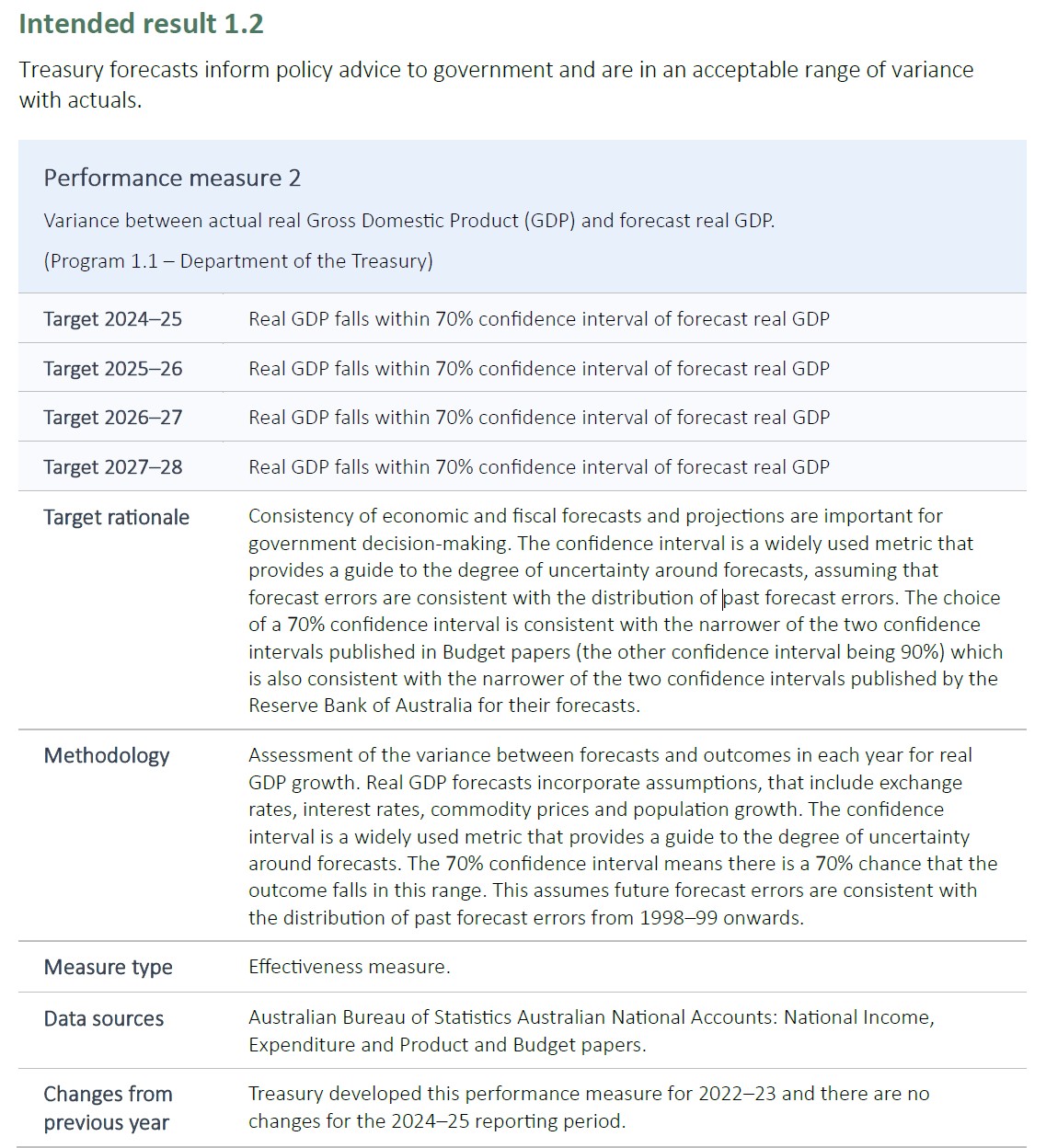

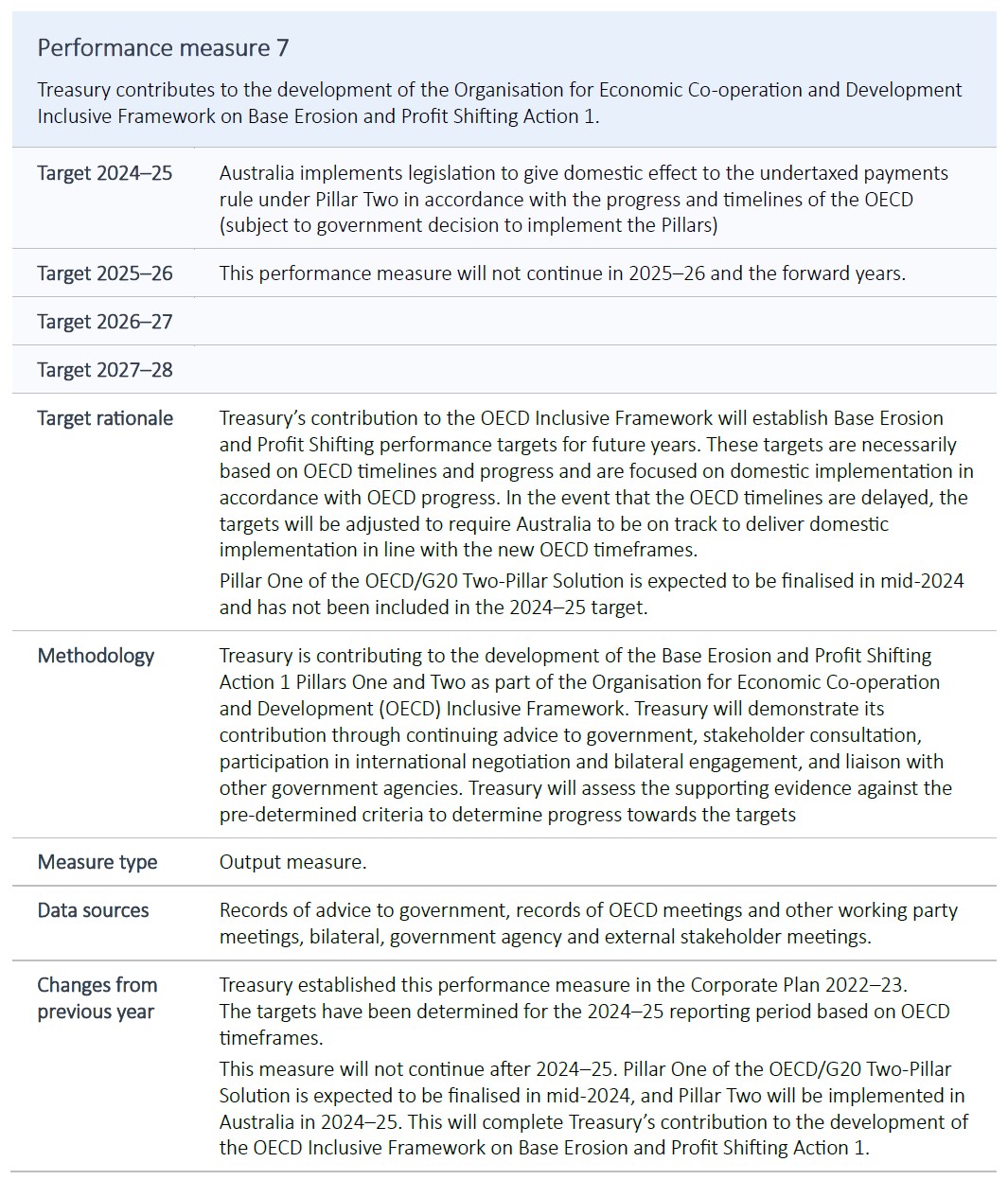

Refer to the Better practice examples in RMG-132 Corporate plans for Commonwealth entities on reporting targets. They include an example of an entity who incorporates a target rationale and another entity that explains the reasons why targets have not been included in its corporate plan (see 10. Reporting targets).

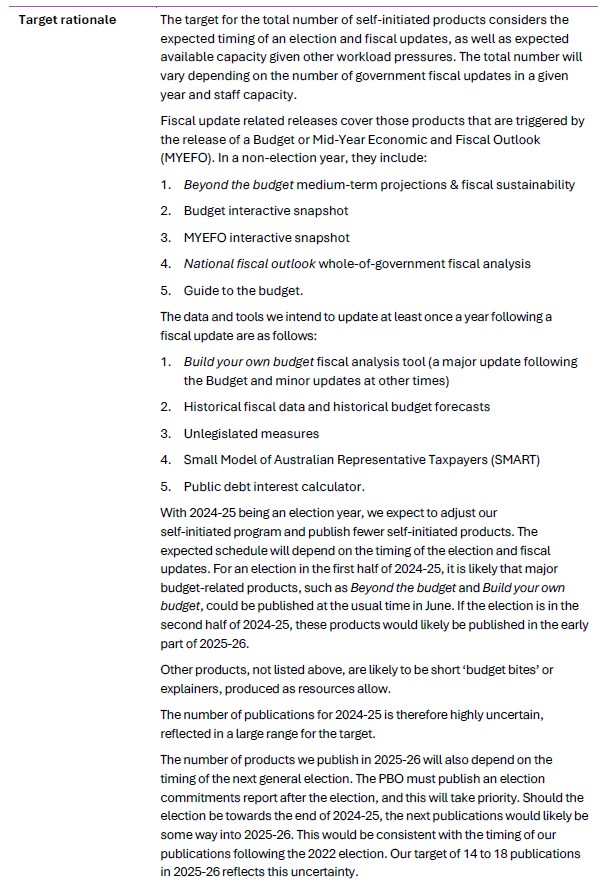

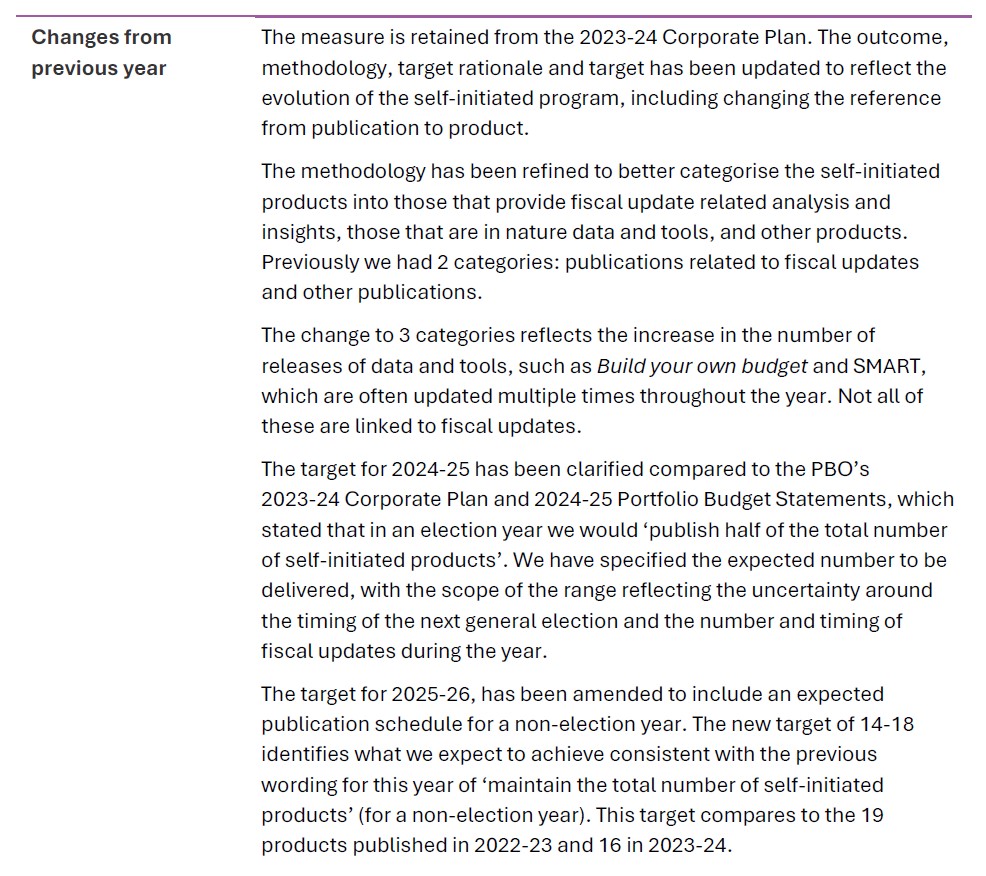

Target rationale examples

See also the examples below of entities who incorporate a target rationale into their performance measures.

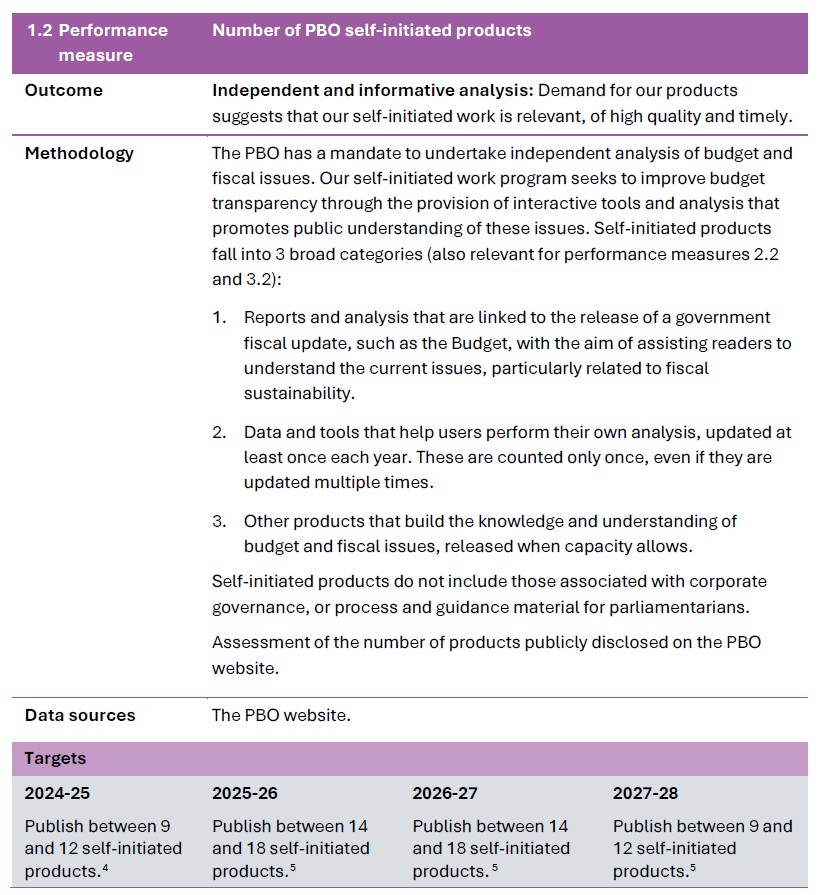

2024–25 Parliamentary Budget Office Corporate Plan (pages 20-22)

Source: Parliamentary Budget Office, Corporate Plan 2024-25