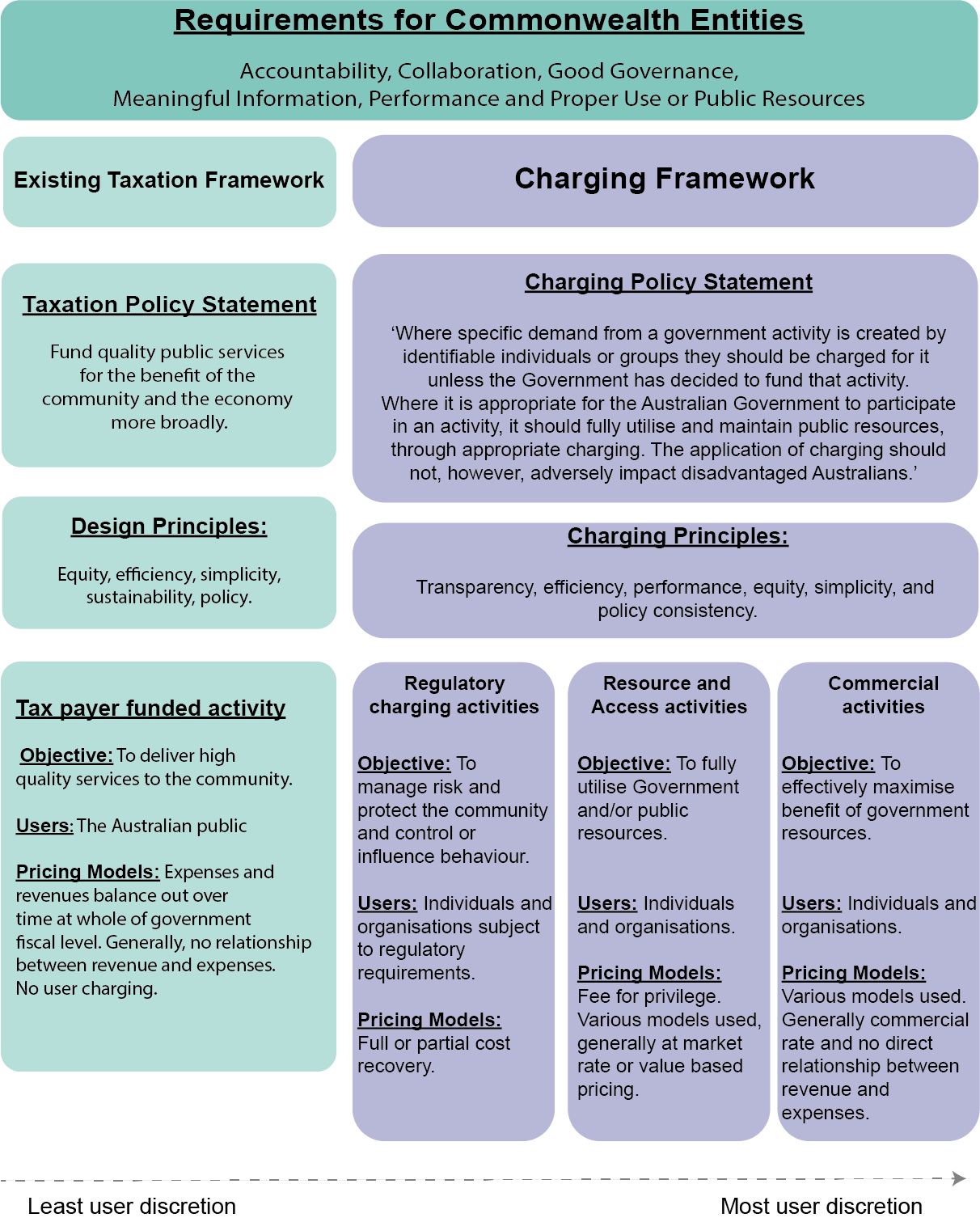

- The Australian Government has a whole-of-government charging framework to apply across the general government sector. The Australian Government Charging Framework (Charging Framework) provides that where an individual or organisation creates the demand for a government activity, they should generally be charged for it, unless the Government has decided to fund the activity.

- The Charging Framework ensures a consistent approach to guide policy development and helps determine when it is appropriate to charge for a government activity, leading to more consistent government charging activities. It is a part of the Government’s toolkit for good public policy design and complements other government priorities, such as contestability and deregulation.

- The Charging Framework applies to all corporate and non-corporate Commonwealth entities in the Government General Sector (GGS) and consists of the following 3 elements:

- Charging policy statement - this states the rationale for identifying, developing and implementing Australian Government charging activities,

- Charging considerations - these guide the decision on the extent to which charging would be appropriate, and

- Charging principles - these guides the design, implementation and review of charging activities.

- The Charging Framework:

- improves the transparency, accountability and management of charging arrangements, including what individuals and businesses are being charged for and why;

- promotes charging across government, in appropriate circumstances;

- provides a decision making rationale, guidance and tools for ministers and government entities;

- brings coherence and reduce inconsistencies in charging across government;

- provides greater certainty for individuals and businesses being charged;

- encourages GGS entities to implement more responsive, citizen-centric government activities;

- manages demand for government services by sending price signals to users; and

- provides citizens with greater input into government activities, thus driving efficiency and improving responsiveness.

Australian Government Charging Framework

The Charging Policy Statement

- The policy statement for government charging is:

- The Charging Framework utilises a user pays approach. This means that where the provision of a government activity confers a degree of private benefit to the individual or group they should be charged for the activity. Based on the type of government activity being provided and relevant public interest considerations, the Government may determine the pricing mechanism and any level of subsidy.

- Charging sends important ‘price signals’ to individuals and groups about the cost or value of a government activity. Individuals or groups that create the need for a government activity should bear, at least, the costs of administering the activity, unless the Government has decided to fund that activity. In this way, prices paid incorporate all of the efficient costs of providing those activities.

Charging considerations

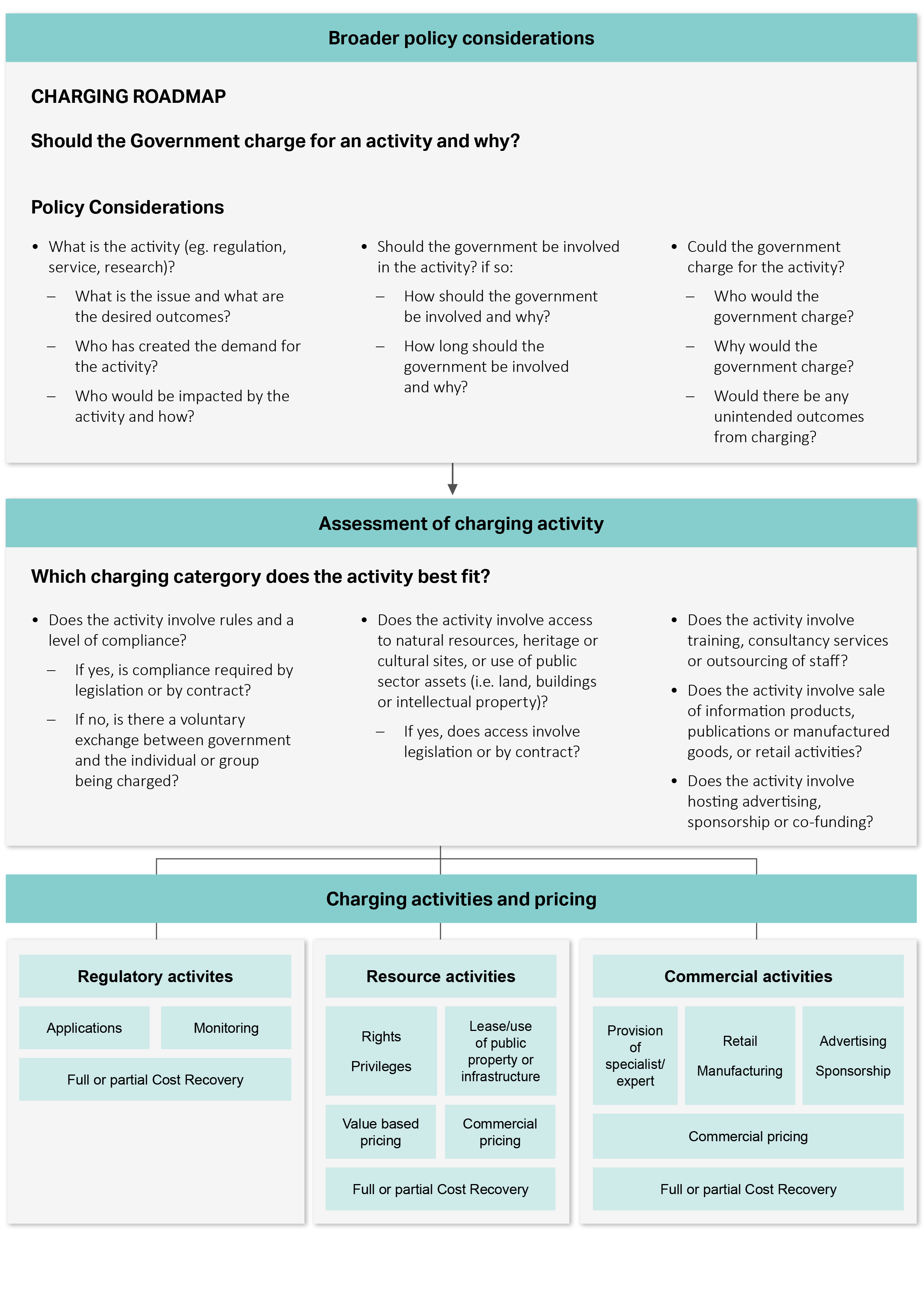

- Charging decisions are made by the Government. The Charging Framework includes considerations to help government entities to develop advice to the Government about whether it is appropriate to charge for a government activity. In considering whether to charge for a government activity, the Government may take into account:

- policy considerations, including the policy problem and proposed solution, whether the government should be involved in the activity, and whether it is appropriate to charge for the activity (e.g. it might not be appropriate to charge for defence or national security activities); and

- specific charging considerations, including the nature and type of activity being proposed, whether charging is efficient or another form of funding is more appropriate (e.g. if charging impacts on disadvantaged Australians, then the activity might be mostly funded through general taxation).

- In making its decision, the Government may also consider broader factors, in addition to these charging considerations, such as the deregulation agenda. The Charging Roadmap (refer to the Australian Government Pricing Models table below), provides a summary of charging considerations and the charging decision making process. A specific consideration, which relates to legal authority for the activity, is constitutional risk. All policy proposals are currently required to address whether there is a constitutional basis for undertaking a specific activity and whether legislation is required. The Framework is consistent with this approach, as ministers must also consider the constitutional basis of a charging activity and whether legislation is required to, impose any charge. If an activity is an ordinary and well recognised function of government, such as photocopying or leasing of property, then legislation may not be required.

Charging principles

- The principles will assist in the design, implementation and review of government charges and build on the principles for regulatory activities in the Cost Recovery Policy. The principles are:

- transparency – is about openness and allowing scrutiny of government activities, decisions and processes. Public transparency means making available key information about the activity, such as the authority to charge, charging rates, and, where relevant, the calculation basis (where publication of this information would not distort market performance) for those who pay charges and other stakeholders;

- efficiency – relates to delivering activities at least cost, while achieving the policy objectives and legislative functions of the Australian Government and considering the economic impact of charging for the activity;

- performance – relates to effectiveness, risk mitigation, sustainability and responsiveness. Government entities must regularly review and evaluate charges to assess their impact and whether they are contributing to government outcomes. Engagement with stakeholders is a key element of managing performance;

- equity – where specific demand for a government activity is created by identifiable individuals or groups they should be charged for it, unless the Government has decided to fund that activity. Equity is also achieved through the Government’s social safety net, to ensure that vulnerable citizens are not further disadvantaged through the imposition of a charge;

- simplicity – whereby charges should be straightforward, practical, easy to understand, and collect; and

- policy consistency – charges must be consistent with Australian Government policy priorities and policies, including the specific entity outcomes and policy objectives for the charging activity. Cabinet-level authority may be required for changes to charging models, for specific areas of activity.

Charging Activities

- The Charging Framework establishes consistent definitions and categorises government charging to assist decision making. These will not override other definitions, such as definitions for legal or accounting purposes, or those in related policies, such as the Australian Government Guide to Regulation.

- Government charging activities can be divided into 3 groups:

- regulatory activities are generally those activities where the government wishes to control or influence behaviour, manage risk and protect the community. They include an enforcement or compliance element and usually do not involve user discretion. Legislation is always required for these charging activities consistent with the cost recovery framework, the charging premise for regulatory activities is that, where an identifiable group creates extra or specific demand for a specific regulatory activity, they should be charged for the activity, where appropriate. Most regulatory activities involve charging for part or all of the costs of an activity on a cost recovered basis and the Cost Recovery Policy will apply;

- resource management and access activities involve the provision of specific rights, privileges, and access to public resources. Some of these activities may be regulatory or require legislation. These activities normally utilise a ‘fee for privilege’ charging model, where the beneficiary is charged based on the potential value of the activity to the recipient. Pricing relates to the specific benefit to the individual or group, based on the value of the resource or access to the resource; and

- commercial activities include those activities where the Government is involved in the market, where there could be actual or potential competitors. Although, the Government might be the sole supplier of an activity, there is usually a degree of user discretion (i.e. it is voluntary) about whether the good or service is consumed. They are the most consensual form of charging activities. Other commercial activities could include provision of specialist or expert services; retail and manufacturing; tailored data provision and advertising and sponsorship. Legislative requirements may vary, depending on the nature of the charging activity. Charging models are usually market driven, but other pricing models may also be used.

Charging activity categories and examples

| Charging categories | Examples |

| Regulatory activities | Applications and registrations, such as applications to register patents or wildlife trade permits. Monitoring and enforcement, such as quarantine compliance audits or insurance sector investigations. |

| Resource management and access activities | Rights and privileges, such as licenses for access to spectrum, commercial fishing licenses, or CSIRO licensing use of its Wi-Fi technology to others. Lease and use of public property or infrastructure, such as sub-leasing of government land and/or buildings or hiring out of vehicles, machinery, laboratories or specialist facilities |

| Commercial activities | Provision of specialist or expert services, such as access to laboratory technicians or statisticians. Commercial and manufacturing, such as sales from gift shops or other government shops, sale of publications, entry fees to sporting facilities, sale of tailored data, manufacturing of medical isotopes. Advertising and sponsorship, such as sale of advertising space on websites, or sponsorship of conferences. |

Charging Roadmap: Summary of decision making processes

Note: these activities are currently covered by the Cost Recovery Policy.

- Once the decision to charge is made, the type of activity will influence the pricing model that should be used. This will also need to take account other government policy considerations (e.g. community service obligations may result in a subsidised price). The Australian Government Pricing Models table provides an overview of these pricing models. The Summary of Australian Government Charges and Taxes table provides an overview of the types of activities the Cost Recovery Policy applies to and shows the scope of the new Framework.

Australian Government Pricing Models

| Pricing models | |

|---|---|

| Cost recovery pricing | |

Cost recovery Full cost recovery Partial cost recovery | There are two types of cost recovery charges: Cost recovery fees are a charge for a good, service or regulation (in certain circumstances) to a specific individual or organisation. Cost recovery levies are a charge imposed when a good, service or regulation is provided to a group of individuals or organisations rather than to a specific individual or organisation. A cost recovery levy is a tax and is imposed via a separate taxation Act. It differs from general taxation as it is ‘earmarked’ to fund activities provided to the group that pays the levy. Charging the non-government sector all of the efficient costs of a specific government activity. Partial cost recovery charges the non-government sector some of the efficient costs of a specific government activity. |

| Value-based pricing | |

| Fee for privilege | A charge imposed in relation to access to a public resource that confers a clear right or privilege (including access to a limited resource). This could include a royalty payment calculated in respect of the quantity or value of things taken, produced or copied, or linked to the occasions upon which the right is exercised. |

| Access fee | A charge for access to or use of a specific public resource (e.g. entering an exhibition or leases of a building or equipment). |

| Commercial pricing | |

| Market-based pricing | This is sometimes referred to as competitive-based pricing and is based on the prices of similar products in the market or a proxy, where there are no actual competitors. Depending on whether the Australian Government activity has more or less features than the competition, the government can set the price higher or lower than the competitor pricing, taking into account competitive neutrality principles. |

| Consumption, subscription and freemium models |

|

| Dynamic-based pricing | This pricing is based on demand for that activity (e.g. auctions). Pricing is adjusted in response to market demands. That is, when demand is low and elastic, prices are adjusted lower to increase the attractiveness of the government activity. |

Summary of Australian Government Charges and Taxes

Charging categories | Regulatory charges | Resource charges | Commercial charges | Fines and penalties | General taxation | |

| Pricing Models | Cost recovery fees

| Cost recovery levies

| Value-based pricing, commercial or cost recovery | Value-based pricing, commercial or cost recovery | Fines, including statutory fines and enforcement penalties | Specific taxes, non-cost recovery levies, excises and customs duties |

| Relationship between charges and costs | Charges must reflect efficient unit cost of a specific good or service

| Charges must reflect efficient overall costs of the activity

| Charges generally based on the potential value of the activity to the recipient | Charges generally based on market rates | Amounts of fines and penalties relate to specific criminal sanctions | Taxes generally do not relate to a specific activity or its costs (i.e. raise general revenue)

|

| Statutory authority to charge | Legislation required

| Taxation Act required | Legislation may be required

| Legislation may be required

| Legislation may be required

| Excise, customs or taxation Act required

|

| GFSb reporting classification | Non-taxation revenue | Non-taxation revenue | Non-taxation revenue | Non-taxation revenue | Taxation revenue | |

| Examples of activities | Registrations Applications Licences | Monitoring compliance Investigations Enforcement | Rights and privileges, including licences to access IP or natural resources Also includes lease and use of public property or infrastructure | Sale of publications or data Provision of specialist expertise Advertising and sponsorship | Timeframe sanctions Remediation penalties | Government services for the benefit of the community and the economy more broadly - for example road infrastructure and Medicare service |

Charges not subject to the Australian Government Charging Framework.

a R = revenue generated from the activity; E = expenses incurred in providing the activity.

b Government Finance Statistic