Public Governance, Performance and Accountability Rule 2014 section 16EA(b)

The performance measures meet this requirement when they use sources of information and methodologies that are reliable and verifiable.

Performance measures are required for each reporting period covered by the plan (that is, a minimum of 4-years). Entities often demonstrate this coverage through specified targets, where reasonably practicable to set a target, for each of the reporting periods covered by the plan.

Performance measures must use sources of information (data sources) and methodologies that are reliable and verifiable. These terms are taken to have their common, everyday meaning:

Reliable

Reliable

To have confidence in, or trust in sources of information and methodologies used. They can be relied upon and are trustworthy.

Verifiable

Sources of information and methodologies used can be proven to be true or correct.

Performance measures should be supported by clearly identified data sources and methodologies. Methodologies used need to be designed in a way to produce accurate data, be applied consistently (both by different users at a given point in time and by similar users over different reporting periods) and be able to be substantiated. This allows for the processes followed in generating data for each measure to be validated.

Entities should maintain records that properly document the data sources and methodologies used to measure performance. It is a better practice for entities to report the data source and methodology chosen for each performance measure in entity corporate plans and annual performance statements.

Data sources might include research and evaluation centres (such as the Bureau of Infrastructure, Transport and Regional Economics), internal databases or systems (such as payment or call centre systems), or external sources (such as the Australian Bureau of Statistics or OECD reports).

Methodologies may include participant and stakeholder surveys, benchmarking, evaluation or data mining and analysis.

Entities should avoid using vague language in their performance information, such as:

- ‘qualitative assessment’

- ‘timely’

- ‘ready to implement’.

For example, a measure such as ‘Government measures are legislated and implemented in a timely manner’ does not make clear what the measures are, what ‘timely’ means, nor what implemented means. Does the entity have a timetable for implementation?

The language used should be clear to enable consistent measurement and enable the reader to understand what is being measured and how. Specific and precise parameters should be available to a reader applying performance assessment. Without this information, there is a potential for bias in the reported result, and it may be difficult for the performance measure to be measured consistently or be substantiated.

Better practice principles:

- Data sources and methodologies for each performance measure should be outlined and clearly identifiable in entity corporate plans and annual performance statements

- The language used should be clear, specific and precise to enable consistent measuring and enable the reader to understand what is being measured and how.

For further information about annual performance statements, refer to RMG-134 Annual performance statements for Commonwealth entities.

Examples

The information presented in the examples below allows the reader to clearly understand what is being measured and how.

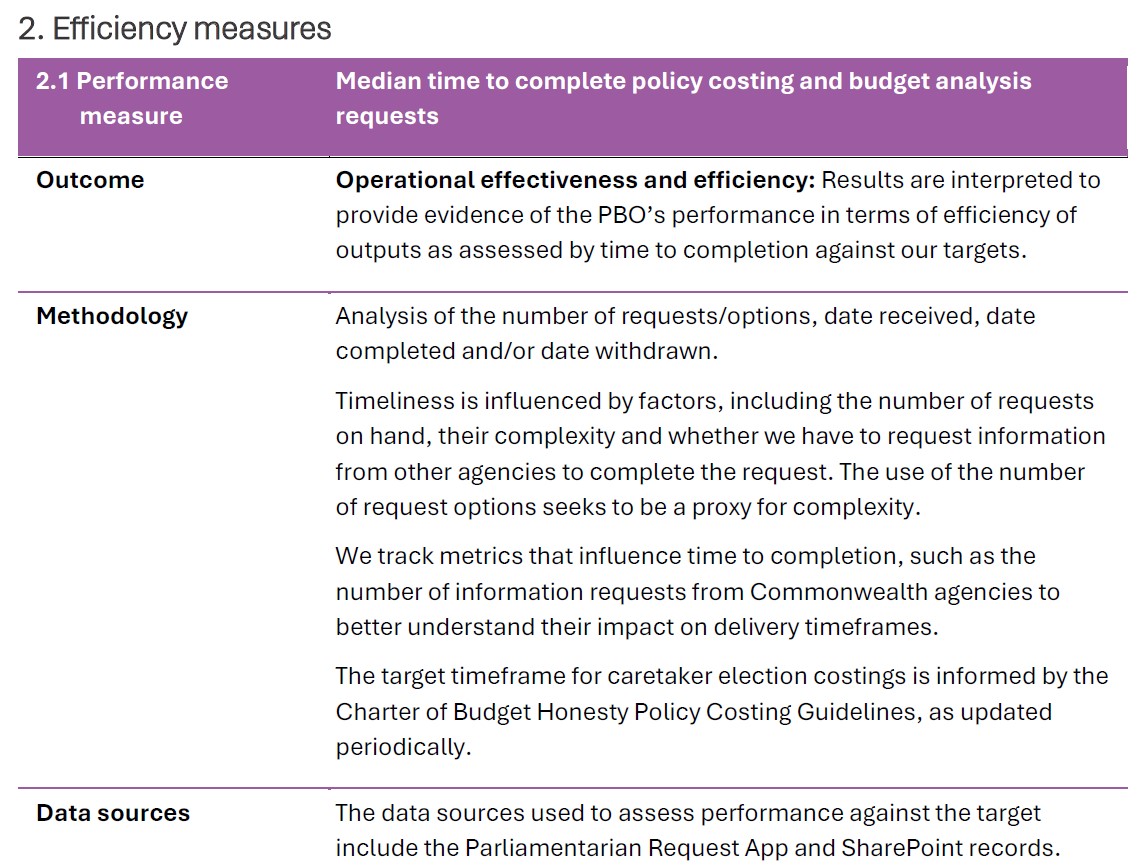

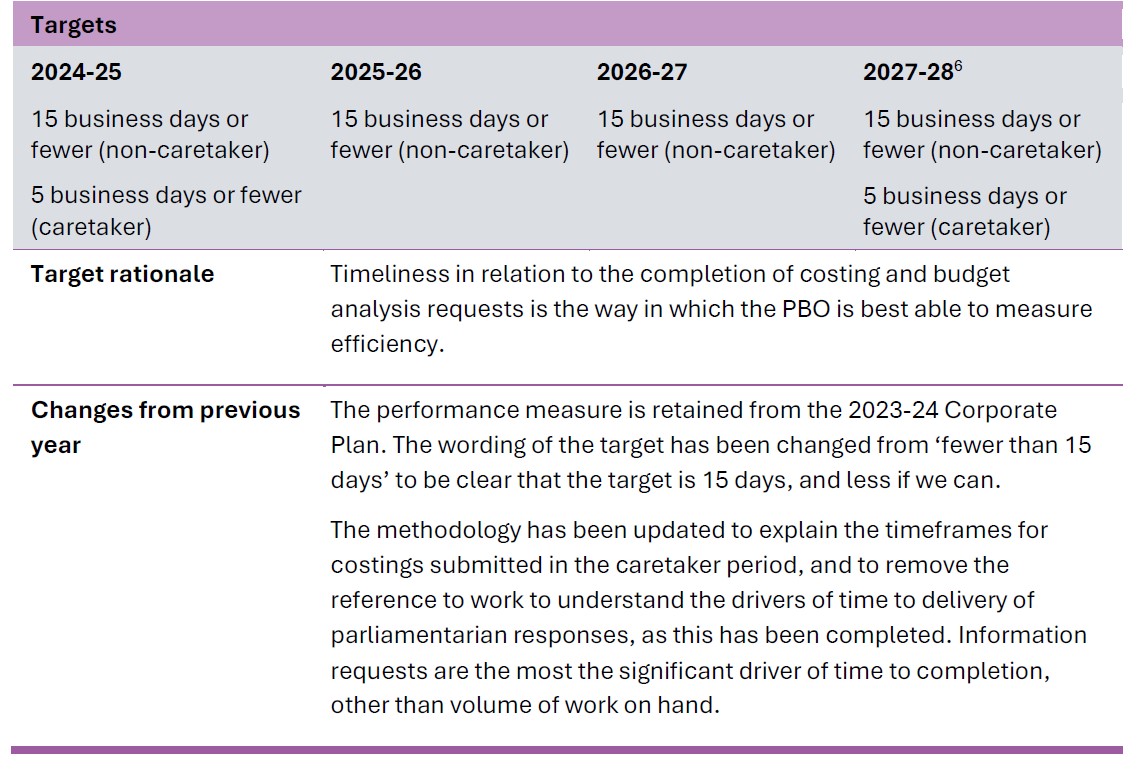

2024–25 Parliamentary Budget Office Corporate Plan (page 24)

Source: Parliamentary Budget Office, Corporate Plan 2024-25

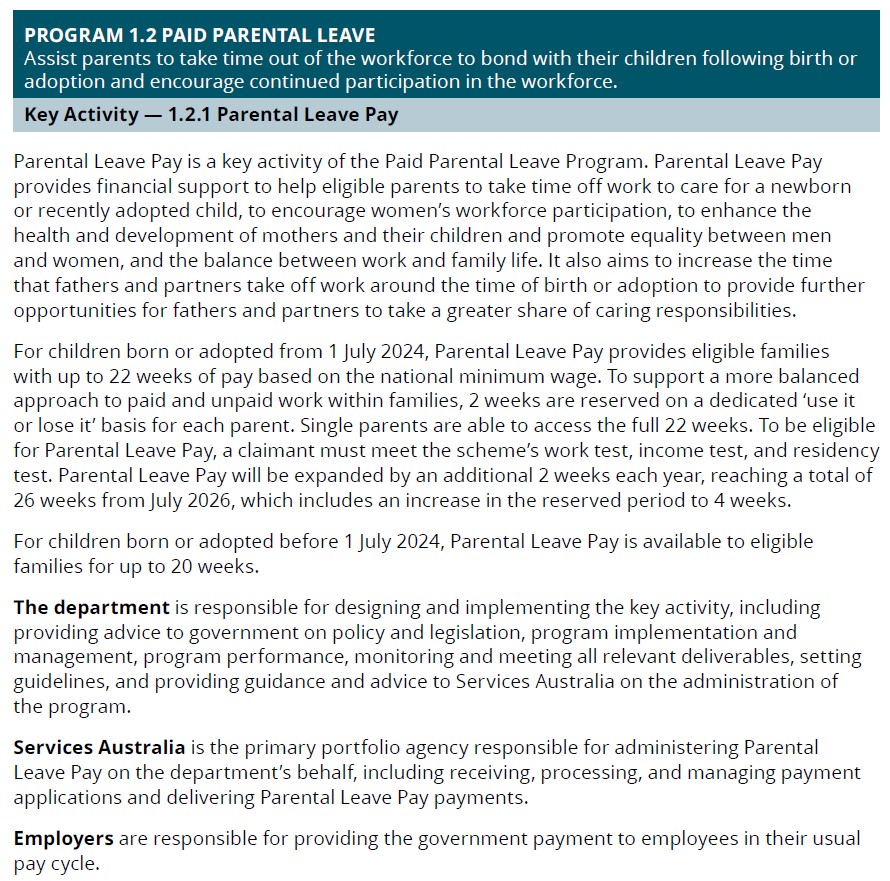

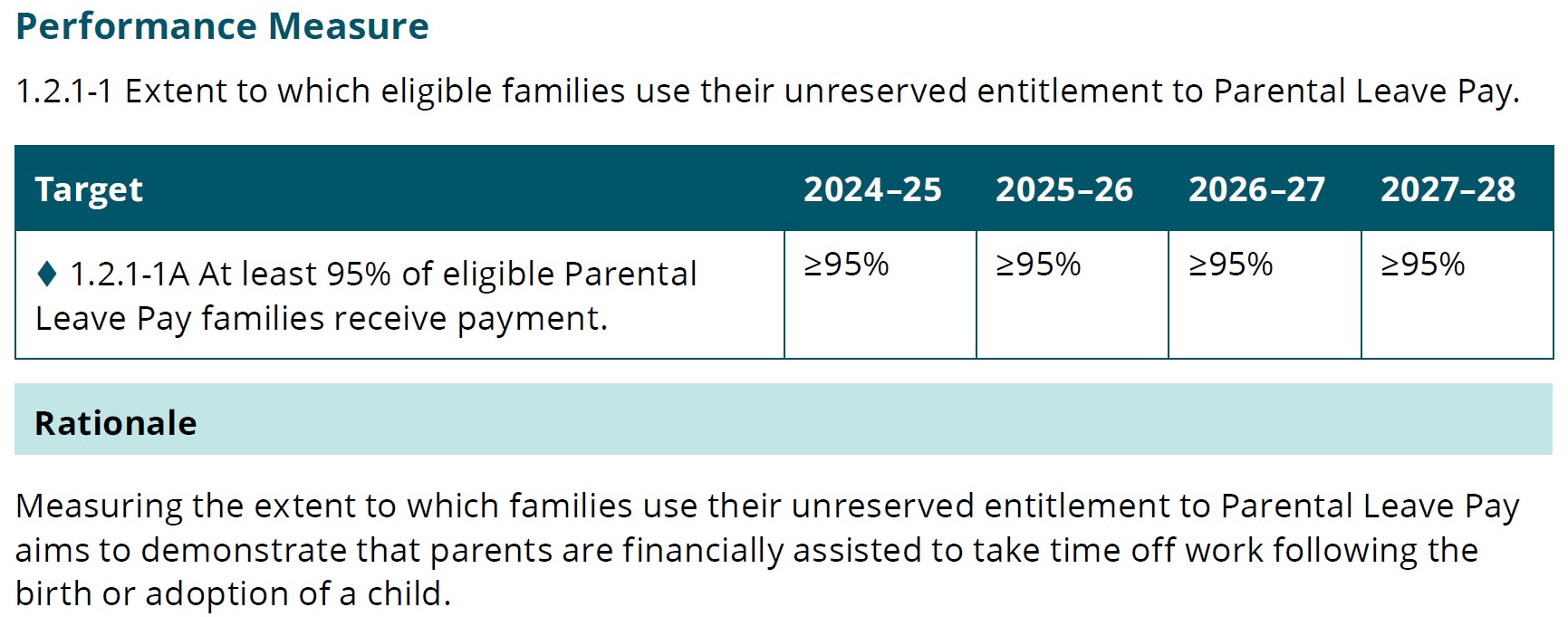

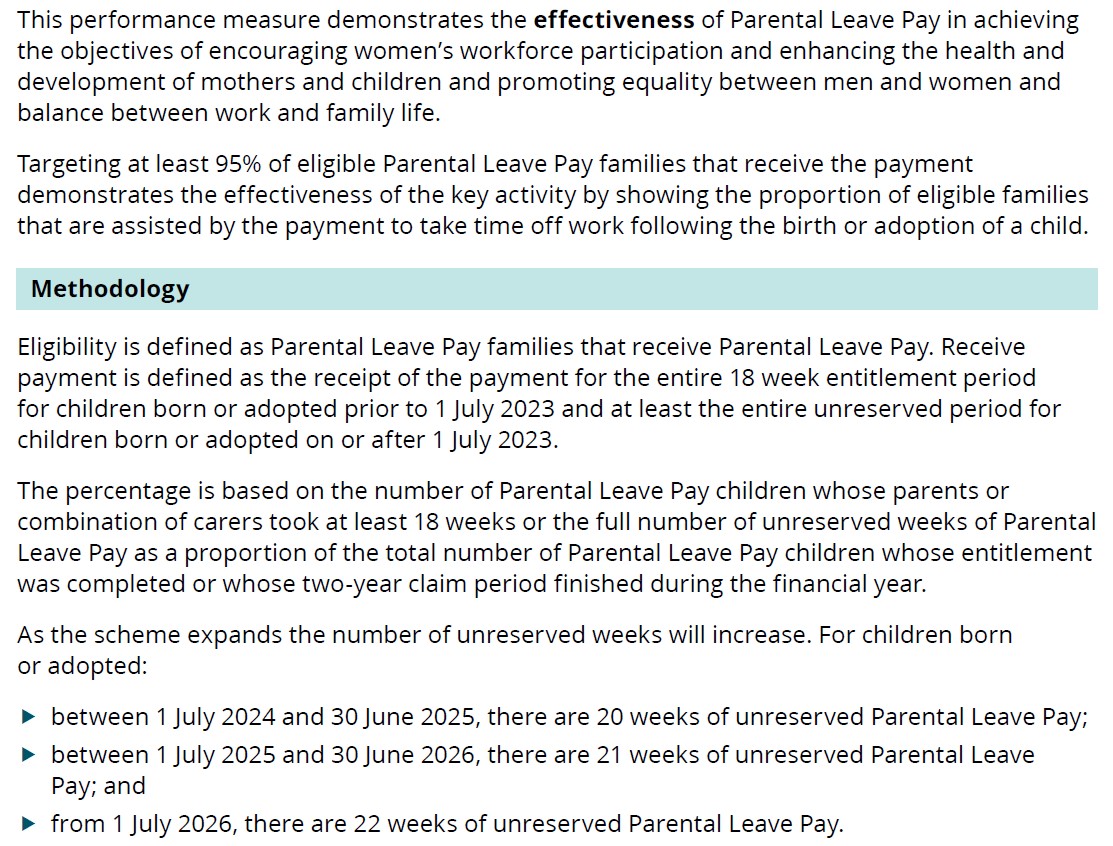

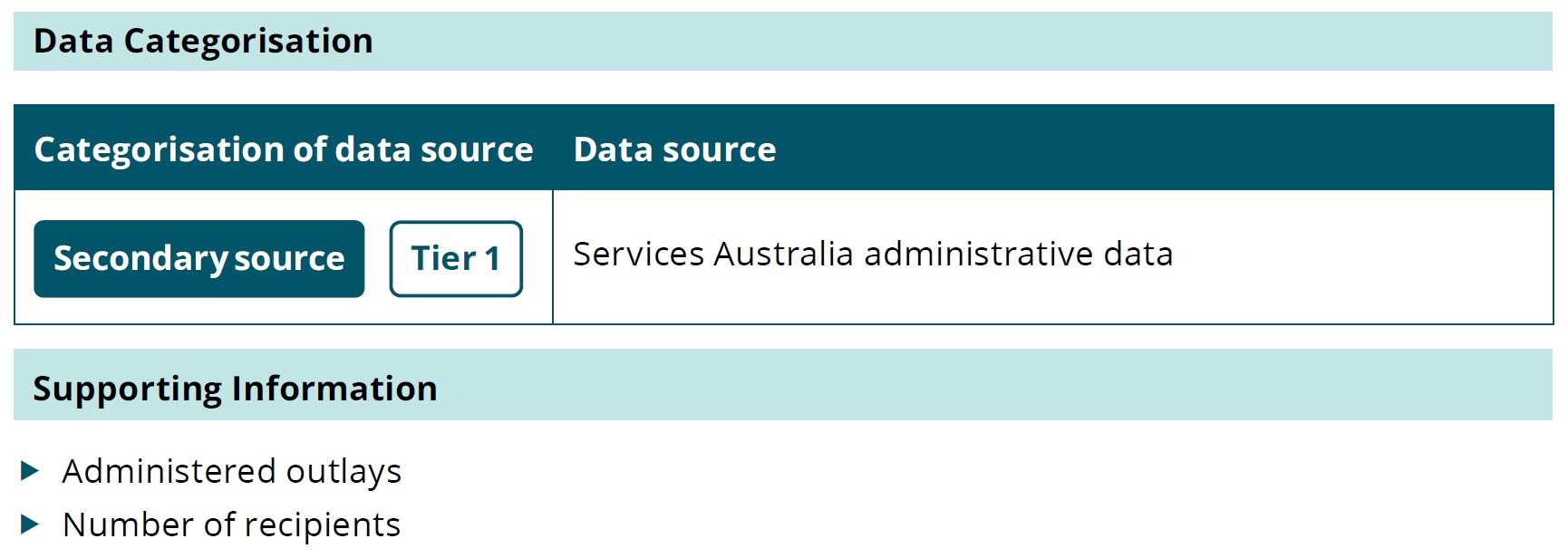

2024–25 Department of Social Services Corporate Plan (pages 27-28)

Source: Commonwealth of Australia (Department of Social Services)