RMGs are guidance documents. The purpose of an RMG is to support PGPA Act entities and companies in meeting the requirements of the PGPA framework. As guides, RMGs explain the legislation and policy requirements in plain English. RMGs support accountable authorities and officials to apply the intent of the framework. It is an official’s responsibility to ensure that Finance guidance is monitored regularly for updates, including changes in policy/requirements.

RMG 419 has been updated to reflect that the COAG Legislation Amendment Act 2024 received Royal Assent on 5 July 2024 to amend the COAG Reform Fund Act 2008 (now the Federation Reform Fund Act 2008) and other Acts to update references to COAG reflecting the cessation of the Council of Australian Governments and changes to intergovernmental architecture.

If you have any feedback on our RMGs or have any queries in relation to this guidance, please contact us at PGPA@finance.gov.au.

Audience

This guide applies to all relevant officials, particularly chief financial officers and finance teams, in Commonwealth entities that have responsibility for classifying Australian Government payments to other levels of government.

For ease of reference and presentation, the RMG uses:

- ‘entities’ to mean Commonwealth entities, as defined by the Public Governance, Performance and Accountability Act 2013 (PGPA Act)

- ‘states’ to mean Australian states and territories

- ‘other levels of government’ to include both state and local governments.

Key points

This guide:

- provides advice on the types of payments that are within scope of the federal financial relations (FFR) framework, and the payment classification process undertaken by the Department of Finance (Finance)

- provides guidance on the classification of payments to other levels of government for specific purposes as distinct from Commonwealth own-purpose expenses (COPEs) that may involve payments to other levels of government

- replaces Classifying payments to other levels of government for specific purposes and Commonwealth own-purpose expenses (RMG 419), dated December 2020.

Introduction

- Australia has three levels of government that work together to provide us with the services we need. Each level of government has its own responsibilities, although in some cases these responsibilities are shared.

- Correctly classifying Australian Government payments is important as it assists to determine:

- how each payment is reported in Budget papers

- whether payments are subject to the federal financial relations (FFR) framework or the Commonwealth Grant Rules and Principles (CGRPs).

Part 1 - Legislative Framework

- Financial relations between the Australian Government and the states are governed by the provisions of the:

- Intergovernmental Agreement on Federal Financial Relations (IGA FFR) which recognises that the states have primary responsibility for many areas of service delivery, with coordinated action to address Australia’s economic and social challenges. The IGA FFR is a living document, with detailed arrangements set out in schedules which can be updated as necessary, with the agreement of the National Cabinet

- Federal Financial Relations Act 2009 (FFR Act) which provides a standing appropriation for the Australian Government to provide financial support for the delivery of services by the states through national specific purpose payments and for the Treasurer to determine Goods and Services Tax (GST) payments to the states

- Federation Reform Fund Act 2008 which establishes the Federation Reform Fund for the purpose of making grants of financial assistance to the states, and specifies that the terms and conditions on which financial assistance is granted are to be set out in written agreements between the Australian Government and the states.

Part 2 - The federal financial relations framework

- The Federal Financial Relations (FFR) framework centralises Australian Government payments to and through the states for general and specific purposes for:

- general revenue assistance – primarily through GST distribution, which has no conditions on how states use the funding

- a range of specific-purpose payments – to be spent on particular sectors or projects.

- The FFR framework provides ongoing financial support for the delivery of services by the states through general revenue assistance, including GST payments and other general revenue assistance, to be used by the states according to their own budget priorities and payments for specific purposes.

- The FFR framework includes payments to or through state governments but excludes Commonwealth own-purpose expenses (COPEs) and payments direct to local governments – which are generally subject to the CGRPs.

Roles and responsibilities under the FFR

- Under the FFR framework the Treasurer is accountable for payments to the states, including through the Federation Reform Fund. Department of the Treasury (Treasury), in consultation with portfolio entities, is responsible for the administration of estimates and payments under the FFR framework, which are reported in Budget Paper No. 3, Federal Financial Relations (Budget Paper No. 3).

- The relevant minister and entity remain responsible for ensuring that all necessary policy and budget authority exists, and the day-to-day administration of agreements, including requirements for all relevant legislative approvals to be in place.

- Under the FFR framework, Finance is responsible for the classification in Budget papers of Australian Government expense payments to other governments, which include:

- payments made ‘to’ states, including:

- national specific purpose payments (NSPP) which are a funding mechanism through which the Australian Government supports state efforts in delivering services in key sectors (e.g. health, schools, skills and training, disability services and affordable housing)

- national partnership payments (NP payments) which support the delivery of specified outputs or projects, to facilitate reforms or to reward the states for nationally signification reforms

- payments that are made ‘through’ the states where they have less influence on how the funds are spent and to bodies that fall within the state government responsibilities (e.g. non-government schools). Payments ‘through’ the states are also often national partnership payments (as defined in FFR Act)

- payments made direct to local government.

- For more information on the FFR framework and associated arrangements for agreements and payments, see:

Part 3 - Commonwealth own-purpose expenses

- Payments to states and direct to local government entities that are classified as a COPE are excluded from the FFR framework. A COPE is an expense made by the Australian Government in the conduct of its own general government sector activities, and includes expenses for the purchase of goods and services and transfer payments. These include:

- arrangements where the Australian Government is purchasing specific services from state government bodies

- competitive grants programs that can be applied for on the same terms and conditions as government and non-government sectors (even where all applications except one are from state or local government entities, the funding will still be classified as a COPE).

- COPEs may be paid to other levels of government in which case the payments are:

- made and reported by the responsible entity

- not reported in Budget Paper No. 3

- may be subject to the CGRPs.

Part 4 - Classification criteria and process

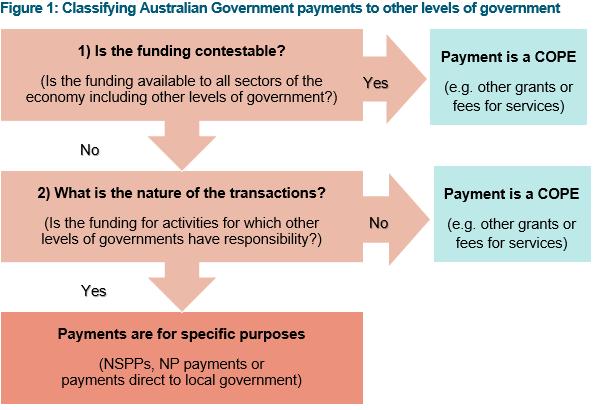

- Two criteria determine whether an Australian Government payment to other levels of government is a payment for specific purposes or a COPE. If the payment is contestable the payment is classified as a COPE and the second criterion is not applied.

- Contestability of the payment(s) – whether the funding is available to all sectors of the economy. Where the:

- allocation of Australian Government funding is open to all sectors of the economy that can provide the required goods and services, including all levels of government, this expenditure is a COPE (including fee-for-service type arrangements)

- funding is not open and is restricted to other levels of government or particular bodies in areas of state government responsibility (e.g. public hospitals, schools and local councils), it may be classified as payments to, or through, the states or direct local government

- The nature of the transaction(s) – the level of government with responsibility for the activity influences classification as a COPE. A payment to other governments, or sectors regulated by other governments through legislation, for an activity under their responsibility will not typically be considered a COPE.A ‘payment through the states’ classification would be used where:

- the payment is for a specific purpose but the states pass on the funding to non‑government entities (i.e. states act as agents) such as payments for non‑government schools

- indirect Local Governments Assistance payments where the states have little impact on how the resources are used

- programs are jointly administered by the Australian Government and states.

- Contestability of the payment(s) – whether the funding is available to all sectors of the economy. Where the:

- For enquiries regarding Commonwealth-state expenditure policy, email the relevant Agency Advice Units (AAUs).

Classification process

- Figure 1 shows the process for classifying Australian (including state government entities, authorities, state‑owned corporations, local councils, etc).

Illustrative examples

- The following are hypothetical examples that illustrate the application of the classification and process to classify Australian Government payments to the states.

Scenario: To support older people, the Australian Government decided to fund the costs of a robot for each Australian aged over 70 years and living at home. The trial program made grants through a competitive tender process using selection criteria, which resulted in state governments being selected as service providers.

Process: To determine the classification of the payments, consideration is given to:

- contestability – the Australia Government funding is available to all sectors of the economy, including other levels of government

- this scenario, the second criterion is not required.

Classification: Payments are a COPE and subject to the CGRPs.

Scenario: A state government announced that it will fund the redevelopment of a public children’s hospital. The Australian Government will contribute $200 million.

Process: To determine the classification of the payments, consideration is given to:

- contestability – the Australian Government’s contribution of $200 million is provided directly to the state government so it is non-contestable

- the nature of the transaction – the hospital is a part of the state health system and the state is responsible for the delivery of public hospital services. The state government funds the project and is responsible for the delivery of the project.

Classification: The contribution is a ‘payment to the states’ under the FFR framework and is published in Budget Paper No. 3.

Scenario: The Australian Government will provide $100 million for a local council to build a community centre, which will increase the number of tourists to the town centre.

Process: To determine the classification of the payments, consideration is given to:

- contestability – funding is provided directly to the council (non-contestable)

- the nature of the transaction – this is the council’s project. The council has responsibility for project delivery and will realise the benefits from the project.

Classification: The payments are ‘payments direct to local government’, which are generally subject to the CGRPs.

Scenario: The Australian Government makes payments to the states for non government schools.

Process: To determine the classification of the payments, consideration is given to:

- contestability – the funding is provided directly to the states so it is non-contestable

- the nature of the transaction – non-government schools are established under state education systems (i.e. the states are responsible for regulating schools and have primary responsibility for the sector). The states will pass the payments on to non-government entities.

Classification: The payments are ‘payments through the states’ – even though the Australian Government provides the majority of government funding to these schools, such payments are not classified as COPE as the states have responsibility for the education system.

Part 5 – The different responsibilities between Department of Finance and Department of the Treasury in managing Payments to other levels of Australian Government

- Various areas within Finance are responsible for managing payments to other levels of Australian Government:

- Government Financial Statistics (GFS) and Estimates team provides advice on the types of payments that are within scope of the FFR framework

- GFS and Estimates team provides payment classification based on this guide

- CBMS Support team establishes specific purpose payments (SPP) codes within the Central Budget Management System (CBMS) via approval from 3 teams within Finance - the AAUs, Expenditure Trends team and GFS and Estimates team

- In consultation with the relevant portfolio entities, AAUs validate SPP estimates within CBMS

- GFS and Estimates team provides consolidated SPP data to Treasury for Whole of Government Reporting for Budgets, Final Budget Outcomes and Mid-Year Economic Fiscal Outlook updates.

- Treasury is responsible for the following:

- Under the FFR framework the Treasurer is accountable for payments to the states, including through the Federation Reform Fund. Treasury, in consultation with portfolio entities, is responsible for the administration of estimates and payments under the FFR framework, which are reported in Budget Paper No. 3, Federal Financial Relations.

- Treasury Federal Financial Relations team works with portfolio entities on the development of Commonwealth-State funding agreements, ensuring the agreements align with the FFR framework.

- Treasury provides the commentary and tables published in Budget Paper No 3, Federal Financial Relations which presents information on the Australian Government’s financial relations with state, territory and local governments.

Part 6 – Payment Classification Process

- For any payment classifications, the agency needs to address two criteria:

- Contestability: Is the funding only available to the state government or local government? Is the funding directly provided to the state government or local government?

- The nature of transactions: Who is ultimately responsible for delivery of the project? If the payment is not available to all sectors of the economy, the nature of transaction helps to determine whether a payment to the other governments is a COPE.

- All payment classification requests are required to be sent via email to the COPE Inbox (cope@finance.gov.au). Most agencies structure their responses similar to the examples provided in RMG 419, Part 4 (please refer to page 8 – 10).

- Once a payment classification has been determined, the payment classification determination will be sent via email to the entity, as well as the relevant AAU, and the State Payments team within Treasury. It is important to have the payment classification determination in written form as Finance and Treasury needs a record of it in order for the SPP codes to be created in CBMS.

Part 7 – Process to establish an SPP in Central Budget Management System and publication

- Entities responsible for the policy sends payment classification request via email to the COPE Inbox (cope@finance.gov.au).

- The GFS and Estimates team sends a response to the entity with the payment classification and notifies the relevant AAU and the State Payments team within Treasury.

- Payment classifications can be the following:

- SPP to the states

- SPP through the states

- Payments to local governments

- Loans to state governments

- Commonwealth Own Purpose Expense (COPE)

- SPP codes are required to be established in CBMS for all payment classifications listed above except for COPE payments.

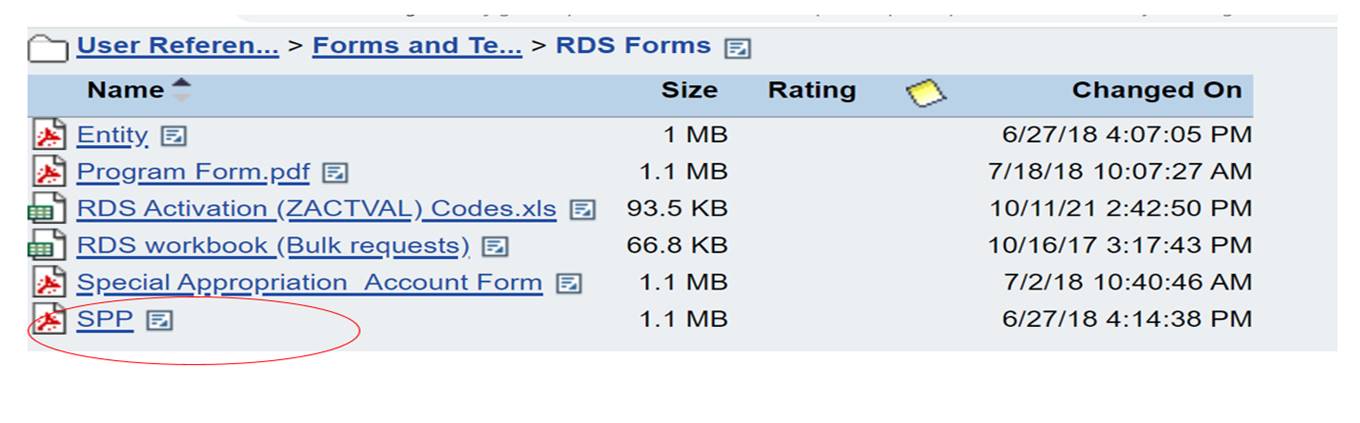

- SPP codes are created in CBMS by the CBMS Support team once Treasury or the relevant entity have sent through the CBMS code creation request form which can be found in CBMS using the path below: User Reference Material > Forms and Templates > RDS Form > SPP

- Appendix A of the SPP form provides detailed instructions on how to complete the form.

- Whilst it is the entity responsible for the policy that sends through the payment classification request, most often the SPP code creation request would be sent from Treasury in consultation with portfolio entities. This is because the Treasurer is accountable for payments to the states and is responsible for the administration of estimates and payments under the FFR framework.

- The majority of SPPs are paid from the Federation Reform Fund special appropriation and are administered and reported by Treasury (against Treasury’s programs). There are rare circumstances where it is the policy holding entity that reports and administers estimates and payments for SPP, but this arrangement would need to be agreed between Treasury and the portfolio entity.

- The SPP code creation request form is sent from Treasury or other entity (responsible for the policy) once there is policy authority. The completed form needs to be submitted to the CBMS Support team (CBMS@finance.gov.au), who then creates the SPP code in CBMS upon the approval of the three responsible teams in Finance:

- Expenditure Trends team

- AAU

- GFS and Estimates team

- CBMS Support team will advise all relevant stakeholders once the SPP code have been created in CBMS. The agency can then enter in the estimates against the established SPP code, and the relevant AAU validates it.

- The CBMS accounts codes that can be linked to an SPP code are listed below:

| CBMS code | Account Name |

|---|---|

| 1231002 | Interest from housing agreements |

| 1231300 | Interest from State and Territory debt |

| 2331100 | Current Grants to Local Government |

| 2333000 | Current Grants to State and Territory Governments |

| 2334000 | Current Grants through State and Territory Governments |

| 2335007 | Capital Grants to Local Government |

| 2335008 | Capital Grants to State and Territory Governments |

| 2335009 | Capital Grants through State and Territory Governments |

| 5234201 | Loans to state and Territory governments - Advances and Io |

| 5234301 | Loans to state and Territory governments - Repayments |

Part 8 – Managing and reporting of estimates in the system (relevant to payments to other levels of Government)

- Under the FFR framework the Treasurer is accountable for payments to the states, including through the Federation Reform Fund.

- Treasury, in consultation with portfolio entities, is responsible for the administration of estimates and payments under the FFR framework.

- Treasury works with the portfolio entity in managing and reporting of estimates in CBMS.

- For payments which are not appropriated to Treasury, the portfolio entity manages estimates in CBMS directly.

- The AAU that manages the entity responsible for the policy will validate the estimates in CBMS.

Part 9 – Appropriations linked to other level of Government Payments

- Subject to the New Policy Proposal, payments generally classified as an SPP to or through the states or loans to the states as well as payments to direct local governments are reported against administered appropriations.

- Payments classified as a COPE may be reported against administered or departmental appropriations.

- Please consult the Annual Appropriations team and/or Special Appropriations team within Finance for any queries relevant to appropriations.

Resources

This guide is available on the Finance website at www.finance.gov.au.

Other relevant publications include:

For more information, see the websites for: