Public Governance, Performance and Accountability (Financial Reporting) Rule 2015 (FFR) section 12 – Presentation of financial statements

This section of the FRR requires entities to present all items of income and expense in a single statement of comprehensive income.

Under section 12 of the FRR, entities must present income and expenses in a single statement of comprehensive income – entities are not permitted to prepare a separate income statement and statement of comprehensive income even though Australian Accounting Standards Board (AASB) 101 Presentation of Financial Statements (AASB 101) (for Tier 1 reporting) and AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities (AASB 1060) (for Tier 2 reporting) permits this. Tier 2 entities are not permitted to adopt section 26 of AASB 1060 and must present a separate statement of comprehensive income and statement of changes in equity.

Not-for-profit (NFP) entities should use the ‘net cost of services’ format for the statement of comprehensive income consistent with Primary Reporting and Information Management Aid forms of financial statements (PRIMA forms).

Presentation of expenses in the statement of comprehensive income should be on a positive basis unless the specific expense item is a negative expense (such as a credit balance) – to support transparency.gov.au disclosures.

Extraordinary items and separate disclosures

An entity must not present any items of income and expense as extraordinary items, either on the face of the statement of comprehensive income or in the notes.

When presenting information in the statement of comprehensive income or the notes, an entity must disclose separately the nature and amount of material income and expense items.

Circumstances that would give rise to the separate disclosure of items of income and expense include:

- write-downs of inventories to net realisable value or of property, plant and equipment to recoverable amount, as well as reversals of such write-downs

- restructurings of the activities of an entity and reversals of any provisions for the costs of restructuring

- disposals of items of property, plant and equipment

- disposals of investments

- discontinued operations

- litigation settlements

- other reversals of provisions.

Losses and gains from asset sales

Proceeds from the disposal of assets and the carrying amount of assets sold are to be netted-off as a gain or loss on disposal. A material gain is to be presented as a separate class of income from revenue.

Material gains and losses on the disposal of non-current assets (including investments and operating assets) are to be reported in the notes by deducting the carrying amount of the asset and the related selling expenses from the proceeds on disposal. Entities must separately disclose this information in accordance with disclosure requirements.

Accounting for the Goods and Services Tax

As required in AASB Interpretation 1031 Accounting for the Goods and Services Tax (GST) (AASB Interpretation 1031), revenues and expenses should be recognised net of the GST amount.

Revenue

FRR section 34C – Contracts with customers

This section of the FRR requires entities to separately disclose revenue recognised from contracts with customers and impairment losses recognised on any receivables or contract assets arising from contracts with customers.

Revenue recognition by not-for-profit entities

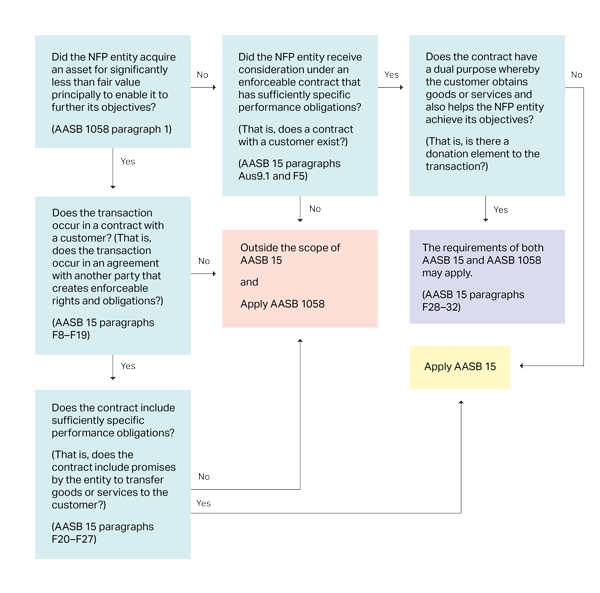

NFP entities must perform a detailed funding agreement/contract review to determine if a transaction is in the scope of AASB 15 Revenue from Contracts with Customers (AASB 15), AASB 1058 Income of Not-for-Profit Entities (AASB 1058). The decision tree below will assist NFP entities in determining which standard applies to a contract.

Decision tree for revenue recognition by NFP entities

Source: AASB Staff FAQs: for Not-for-Profit Entities

Application of revenue standards

Appendix F of AASB 15 provides guidance to assist NFP entities in determining which standard applies to the recognition and measurement of income arising from a particular transaction or event.

A contract component is likely to be for enabling the NFP to further its objectives (not related to the promised goods or services), where:

- there is a non‑refundable component of the transaction price

- the entity has the status of a deductible gift recipient – the donor can claim part of the transaction price as a tax deduction for a donation (see paragraph F31 of AASB 15).

AASB 15 provides guidance for determining when to recognise revenue and how much revenue to recognise. The five-step guidance of a contract with a customer includes:

- identifying a contract with a customer (paragraphs 9–21)

- identifying the performance obligations in the contract (paragraphs 22–30)

- determining the transaction price of the contract (paragraphs 46–72)

- allocating the transaction price to performance obligations (paragraphs 73–90)

- recognising revenue when each performance obligation is satisfied (paragraphs 31–45).

The principles of AASB 1058 apply to:

- transactions where the consideration to acquire an asset is significantly less than fair value – principally to enable an NFP entity to further its objectives, including transfers to enable an entity to acquire or construct a recognisable non-financial asset to be controlled by the entity

- the receipt of volunteer services.

Performance obligations

A customer is a party that is contracted with an entity:

- to obtain goods or services that are an output of the entity's ordinary activities

- promises consideration in exchange for those goods or services.

Under paragraph 6 of AASB 15, a counterparty is not a customer if the counterparty has contracted with the entity to:

- participate in an activity or process

- share in the risks and benefits from the activity or process.

Under AASB 15, revenue is recognised when a performance obligation is satisfied by transferring a promised good or service to a customer. Transfer occurs when the customer obtains control of the good or service.

Control of the good or service is the ability of the customer to:

- direct the use of the asset

- obtain substantially all of the remaining benefits from the asset

- prevent others from directing the use of, and obtaining the benefits from, the asset.

Under paragraph F20 of AASB 15, to identify a performance obligation of an NFP entity, it is necessary that the promise is sufficiently specific to be able to determine when the obligation is satisfied.

As listed in paragraph B2 of AASB 1058, examples of transactions that do not relate to performance obligations (such as donation transactions) are:

- cash and other assets received from grants, bequests or donations

- receipts of appropriations by government departments or other public sector entities

- receipts of taxes, rates or fines

- assets acquired for a nominal or low amount.

Revenue recognition

Under AASB 15, entities are required to measure and recognise the amount of the transaction price as revenue when a performance obligation is satisfied – excluding amounts collected on behalf of third parties (such as GST).

Under paragraphs 9–17 of AASB 1058, income is determined as the difference between the consideration for an asset and the asset’s fair value, after recognising any other related amounts.

Variable consideration

Contracts may include variable consideration due to:

- discounts

- rebates

- refunds

- credits

- price concessions

- incentives

- penalties

- other similar items.

Where this is the case, under paragraph 54 of AASB 15, entities are required to apply one method consistently throughout the contract when estimating the effect of an uncertainty on variable consideration. Of the 2 methods specified in paragraph 53 of AASB 15, entities must select the one that is expected to best predict the amount of consideration the entity will be entitled to.

Non-contractual income from statutory requirements

Income arising from statutory requirements (such as taxes, rates and fines) recognised during the period must be disaggregated into categories that reflect how the nature and amount of income are affected by economic factors (Tier 1 reporting: paragraph 28 of AASB 1058, Tier 2 reporting: paragraph 230 of AASB 1060), noting that:

- taxes, rates and fines are not recognised in accordance with AASB 15, even when they are raised in respect of specific goods or services and they are not contributions by owners acting in their capacity as owners (paragraphs B28–29 of AASB 1058)

- income tax receivable from a taxpayer, the interest income and impairment losses recognised in relation to such receivables during the period are not financial assets as defined in AASB 132 Financial Instruments: Presentation

- other information that may be appropriate for an entity to disclose includes, for each class of taxation income that the entity cannot measure reliably during the period in which the taxable event occurs (paragraphs B28-31 of AASB 1058):

- information about the nature of the tax

- the reason(s) why that income cannot be measured reliably

- when that uncertainty might be resolved (Tier 1 reporting: paragraph 30 of AASB 1058, Tier 2 reporting: paragraph 232 of AASB 1060).

Licences

Appendix G of AASB 15 provides implementation guidance for NFP public sector licensors, including for:

- determining how to account for revenue from licences

- distinguishing a licence (which is subject to AASB 15) from a tax (which subject to AASB 1058)

- non-contractual licences arising from statutory requirements

- recognition exemptions.

Accounting for grants and disclosing assistance by for-profit entities

FRR section 14 – Accounting for Government grants and disclosure of Government assistance

This section of the FRR restricts choice available under AAS for for-profit entities when accounting for government grants.

AASB 120 Accounting for Government Grants and Disclosure of Government Assistance (AASB 120) provides for-profit entities with a number of options for accounting for government grants. Section 14 of the FRR removes the alternative options for for-profit entities, except for transactions under the Paid Parental Leave (PPL) scheme.

Under sections 7 and 8 of AASB 120, a grant is not to be recognised until there is reasonable assurance that the entity will comply with the grant conditions and that the grant will be received. Receipt of a grant, of itself, is not conclusive evidence that the grant conditions have been, or will be, fulfilled. Paragraph 10A of AASB 120 requires the benefit of a government loan at below the market rate of interest to be treated as a government grant. Such loans are to be recognised and measured in accordance with AASB 9.

Paid Parental Leave scheme

PPL payments are not salary for workers compensation purposes and PPL leave is not to be counted as paid leave.

Entities are not obliged to make payments unless they have received funding from the government prior to payroll cut off.

Section 27 of the Public Governance, Performance and Accountability Rule 2014 (PGPA Rule) provides that amounts received under the scheme are ‘relevant non-corporate Commonwealth entity receipts’ and may be retained and used by non-corporate Commonwealth entities (NCEs) in accordance with section 74 of the Public Governance, Performance and Accountability Act 2013 (PGPA Act). Entities are responsible for determining the payroll, accounting, recording and reconciliation processes relating to receipt and payment of parental leave.

Under section 74 of the PGPA Act, NCEs are to disclose PPL receipts in their financial statements as ‘relevant non‑corporate Commonwealth entity receipts’.

For the PPL scheme, accounting treatments include:

- the statement of comprehensive income – amounts received under the scheme are not revenue for the purposes of AASB 1058 therefore payments to employees for parental leave are not expenses.

- accounting treatment for statement of financial position – amounts received at or before the balance date that have not yet been paid to employees are accounted for as cash and a liability (that is, payable).

- statement of cash flows – receipts and payments must be accounted for as operating cash flows and are to be reported on either a gross or net basis.

- Tier 1 reporting: AASB 107 Statement of Cash Flows (AASB 107) paragraphs 13–15 and paragraph 22(b)

- Tier 2 reporting: AASB 1060 paragraph 67 and paragraph 75(b).

Expenses

Reimbursements and repayments

Where an amount that has been expensed is refunded to the entity (that is, cash has been received), it is generally appropriate to treat this amount as a reduction in the expense, except where:

- the amount is received in a subsequent year – in which case it is recorded as income

- the expense is incurred by the Department of Foreign Affairs and Trade (DFAT) on behalf of another entity and DFAT is subsequently reimbursed by that entity. DFAT may record the reimbursement as a reduction in the applicable expense item, regardless of the year in which the reimbursement is received.

Some reimbursements or repayments may not result in a reduction in expense or increase in revenue depending on the legislation governing the original payment. Entities should familiarise themselves with the relevant legislation to understand when a reimbursement or repayment may be receipted/received. For guidance on amounts that are retainable under the provisions of the PGPA Act (section 74) and section 27 of the PGPA Rule – see RMG-307 Retainable receipts.

The treatment for accrual accounting purposes may not be the same as treatment for appropriations. For example, refunded amounts in relation to Departmental activities can be added to an entity’s most recent departmental appropriation item, regardless of the accounting treatment, if the type of receipt is prescribed in the PGPA Rule subsection 27(4) for the purpose of the PGPA Act subsection 74(1).

Employee related expenses

For the following employee related expenses:

- employee benefits expenses – include employee remuneration (both monetary and non‑monetary), but do not include payments or reimbursements of out-of-pocket expenses

- transfer of annual and long service leave (LSL) entitlements – in accordance with paragraph 42 of AASB 1004 Contributions (AASB 1004), the liability in respect of employee benefits accrued up to the transfer date is usually transferred when an employee transfers from an NCE to another Commonwealth entity or to the High Court of Australia. If a payment in consideration for the assumption of annual or LSL liability is made or is to be made:

- the receiving entity shall recognise the assumed liability and an increase in assets (cash or cash receivable); and the losing entity shall recognise the liability extinguished and a decrease in assets (cash) or an increase in liabilities (cash payable)

- where the payment is less than the total amount of the liability for employee entitlements assumed, the receiving entity shall recognise an expense equal to the amount of that shortfall

- cash received in consideration for the assumption of the liability should not be recognised as revenue

- separation and redundancy/termination benefits expenses – payments do not include any benefits that would have been accrued and payable if the redundancy had not occurred (for example, accrued leave entitlements and lump sum superannuation payments). Termination benefits do not include any benefits that are a result of employment being terminated at the request of the employee (that is, without an entity’s offer or resulting from mandatory retirement requirements). Such benefits are post-employment benefits.

See also Part 4 Statement of financial position – Employee Benefits and AASB 119 Employee Benefits (AASB 119) for more information.

Tax payable in relation to employee related expenses should be accounted for in accordance with AASB 112 Income Taxes (AASB 112).

Depreciation

Each part of an item of property, plant and equipment (PPE), with a cost that is significant in relation to the total cost of the item, is to be depreciated separately - see paragraph 43 of AASB 116 Property, Plant and Equipment. If the useful life and depreciation method are the same for each significant part, such parts may be grouped in determining the depreciation charge.

Depreciation of PPE used for development activities may be included in the cost of an intangible asset, recognised in accordance with AASB 138.

Depreciation of an asset ceases at the earlier date of:

- the asset being classified as held for sale, in accordance with AASB 5 Non-current Assets Held for Sale and Discontinued Operations (AASB 5), or

- the date that the asset is derecognised.

Depreciation does not cease when the asset becomes idle or is retired from active use.

Heritage and cultural assets are not depreciated when appropriate restoration activities are undertaken, along with the adoption of appropriate curatorial and preservation policies, to deem the assets have an indefinite useful life. For more information, see Heritage and cultural assets and section 30 of the FRR.

Write-down and impairment of assets

For NFP entities, if the carrying amount of a class of assets is increased as a result of a revaluation, the net revaluation increase shall be:

- recognised in other comprehensive income

- accumulated in equity under the heading of asset revaluation surplus

- recognised in net cost of services, to the extent that it reverses a net revaluation decrease of the same class of assets previously recognised in net cost of services.

Under AASB 136 Impairment of Assets (AASB 136), entities are required to assess at each reporting date if there is indication that an asset may be impaired and, if so, to assess assets for impairment. Intangible assets with an indefinite useful life or intangible assets not yet available for use must be tested for impairment annually, by comparing the carrying amount to the recoverable amount.

Recognition of accrued grant expenses

Accrued grant expenses are only recognised to the extent that they meet the requirements to recognise the liability where grant conditions (such as grant eligibility criteria) were met by the grantee entity, or those entities have provided services or facilities required by the grant agreement.

Borrowing costs

FRR section 15 - Borrowing costs

This section of the FRR requires not-for-profit entities to expense borrowing costs as incurred.

While paragraph Aus8.1 of AASB 123 Borrowing Costs (AASB 123) allows NFP entities to elect to recognise borrowing costs as an expense in the period in which they are incurred, section 15 of the FRR removes such election (that is, NFP entities must expense borrowing costs as they are incurred).

Leases

AASB 16 Leases (AASB 16) sets out the principles for the recognition, measurement, presentation and disclosure of leases to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions.

For further information on entities should refer to RMG-110 Accounting for Leases.

Disclosure of leases

Under subsection 18(2) of the FRR, all reporting entities must apply Tier 1 reporting requirements when applying AASB 16.

Lessees’ treatment of right-of-use assets

Lease ROU assets should be classified by Commonwealth lessees as separate asset classes to corresponding assets owned outright. Entities must disclose ROU assets as a separate class.

Commonwealth lessees are required to apply a cost model under AASB 16 to measure lease ROU assets for initial recognition and subsequent measurement. For more information, see subsection 17(2A) of the FRR and Valuation of non-financial assets.

Lessee lease liabilities

Under subparagraph 47(b) of AASB 16, lessee lease liabilities can be:

- presented separately in the statement of financial position, or

- disclosed in the notes – identifying the line items in the statement of financial position that include those liabilities.

If an entity chooses to aggregate the lessee lease liability with financial liabilities, it must be able to demonstrate that the lessee lease liability and the financial liabilities are of a similar nature or function – otherwise separately present items of a dissimilar nature or function (Tier 1 reporting: paragraphs 29–31 of AASB 101, Tier 2 reporting: paragraphs 21-23 of AASB 1060). For the purpose of the Australian Government consolidated financial statements, entities are required to disclose lease liabilities separately from other financial liabilities.

Lessee lease liabilities should not be disclosed in the financial instrument note. AASB 16 does not require lease liabilities to be disclosed as financial instruments.

Key management personnel remuneration

FRR section 27 - Key management personnel remuneration

This section of the FRR sets out the minimum financial reporting disclosures of entities’ key management personnel remuneration.

Measurement and disclosure

Key management personnel (KMP) remuneration is defined in AASB 124 and AASB 1060 as consideration paid, payable or provided by the entity and is to be measured in accordance with AASB 119, with the exception of superannuation.

Total KMP remuneration disclosed in the annual report in accordance sections 17AD or 17BE of the PGPA Rule should be prepared on an accrual basis, consistent with the KMP remuneration disclosures in the notes to the financial statements (section 27 of the FRR). See section 17CE of the PGPA Rule for more information and RMG-138 Commonwealth entities’ executive remuneration reporting guide for annual reports (RMG-138).

KMP remuneration note

Consistent with AASB 124, AASB 119 and section 27 of the FRR, entities are required to disclose remuneration (compensation in AASB 124) that is paid, payable or provided by the entity using the following 4 major categories:

- short-term employee benefits (includes for example: salary, paid annual leave expense, paid personal/sick leave, performance bonuses, and non-monetary benefits such as medical care, cars and free/subsidised goods or services)

- other long-term employee benefits (includes for example: long-service leave expense, long-term disability benefits, profit-sharing)

- post-employment benefits (includes for example: superannuation, post-employment life insurance and post-employment medical)

- termination benefits, other than accrued leave entitlements.

Other KMP disclosures

Disclosure of KMP compensation is not required by category if the KMP services are provided by a separate management entity (Tier 1 reporting: paragraph 17A of AASB 124, Tier 2 reporting: paragraph 195 of AASB 1060). Where KMP services are from another entity on a fee-for-service contract arrangement, it is not a requirement to include the breakup of amounts in the disclosure of KMP remuneration. However, the amount in total needs to be disclosed.

Other KMP disclosures include:

- ministers’ remuneration – implementation guidance (paragraphs IG7 and IG8) of AASB 124 applies to all KMP including ministers. Entities:

- are not required to disclose ministers’ remuneration in their financial statements

- may include (at the entity’s discretion) a note to disclose the fact that ministers’ remuneration is met by Finance through special appropriations.

- consolidated financial statements – when preparing the consolidated financial statements for an economic entity, the parent entity is required to separately disclose the KMP of the following in accordance with the requirements of this topic:

- the economic entity

- the parent entity (including where the parent entity elects to disclose only parent entity supplementary information as permitted by section 6 of the FRR).

- related party transactions – the objective is to draw attention to the possibility that an entity’s financial position and operating result and performance may have been affected by transactions with related parties. The criteria that are relevant when assessing materiality for disclosing transactions between an entity and its KMP related parties are discussed in:

- AASB 124 Agenda Decision (April 2017)

- AASB Practice Statement 2: Making Materiality Judgements (Dec 2022) including Appendix A Materiality of key management personnel related party transactions of not-for-profit public sector entities

- other references such as the ‘Australian Implementation Guidance to AASB 124’ can also assist entities in making materiality judgements.

For more information on related party disclosures, see Related party disclosures.

- auditor’s remuneration – reporting entities who do not receive audit services free of charge must provide separate disclosure of auditor’s remuneration (Tier 1 reporting: paragraphs 10 and 11 of AASB 1054 Australian Additional Disclosures, Tier 2 reporting: paragraphs 98-99 of AASB 1060).

For more information on reporting executive remuneration information in annual reports, see RMG-138.

For guidance on assessing related party transactions, see 9.4.1 Representations by the accountable authority in the Financial Statements Better Practice Guide. Example related party disclosures are included in the PRIMA Forms.